The Rise of China and the Development of Financial Centres in Hong Kong, Beijing, Shanghai, and Shenzhen

Journal: Journal of Globalization Studies. Volume 4, Number 1 / May 2013

As China's economy becomes more integrated with the world, several financial centres are expected to grow within the Chinese financial system. Hong Kong and Shanghai are unarguably the prime financial centres in China's economy, but Beijing and Shenzhen perform unique and irreplaceable functions in China's financial framework. This paper examines the strengths and competitiveness of Hong Kong, Beijing, Shanghai and Shenzhen through a wide range of market assessments in stock, bond, funds markets, futures and derivatives as well as the foreign exchange market and the presence of corporate headquarters to reveal how the development of financial centres in China relates to the rise of China's economy. The findings suggest that Hong Kong performs the role of an international financial centre in the Greater China region in terms of possessing highly internationalized financial industries and a sound legal environment, while Shanghai, Beijing and Shenzhen have strong points in domestic financial services and functions; together they not only represent the symbolic rise of China but also contribute to the fast growth of China and Asian economies.

Keywords: International Financial Centre, Hong Kong, Beijing, Shanghai, Shenzhen, the rise of China, Chinese financial framework, financial services and functions.

Introduction

China's persistent economic growth in the past thirty years heralds its emergence as a great power in the world economy. China became the world's second largest economy in 2011, has the largest foreign exchange reserves in terms of trade surplus, a banking industry that has remained relatively intact after the 2007–2008 subprime crisis, and a capital market that is predicted to become the world's third largest by 2016 (XINHUA 2007). China's extraordinary economic growth has made financial services increasingly important. Financial services provide organizations with support in raising funds for product and service expansion, risk management and so forth. At the private level, financial services support individual investment and wealth management. Thus, the development of the financial sector is necessary and significant for China to further expand its economy.

As a matter of fact, the study of Chinese financial centres is a hot topic in today's academic world. Plenty of scholars have showed interests in this research area over the past two decades. Some have made great contributions to comparative studies of Hong Kong and Shanghai (Yeung 2001; Jao 2003; Sung 2009); while others have devoted their studies to the determining factors for financial centres' formation (Gehrig 1998; Zhao 2003, 2013), and theories of financial centre development (David 1988, 1994; Porteous 1995; Zhao 2003, 2013; Zhao et al. 2004) and so forth. However, little attention has been paid to other Chinese financial centres such as Beijing and Shenzhen. In addition, few studies have focused on the cooperation between financial centres in China even though existing literature has already discussed the competition or relationship between Hong Kong and Shanghai (Yeung 2001; Jao 2003; Karreman and Knaap 2007) or Hong Kong, Shanghai and Beijing (Yeung 2010). The recent accelerating trend of China's financial centre development warrants close monitoring and further research.

China's central and local governments are zealous in promoting the development of financial centres. Beijing Financial Street, located inside Beijing's 2nd Ring Road, was positioned as the core of Beijing's financial centre according to Beijing International Financial Centre Development strategic plan announced in May 2008 by the Beijing municipal government. However, Shanghai's future seems more promising. In 2009, the State Council of China released a resolution to build Shanghai into an International Financial Centre that will match the country's economic strength and the international status of its currency, the RMB, by 2020 (Zhao 2010). Shenzhen has also been catching up. In 2009, China's State Council approved a pilot plan for the Qianhai Shenzhen-Hong Kong Modern Service Industry Cooperation Zone to implement experimental polices, which promote Qianhai as a pilot zone for the establishment of innovative financial institutions and the development of innovative trading platforms to support experimental activities in financial reform under Shenzhen-Hong Kong cooperation. Mr Li Keqiang, Vice-Premier of the State Council, during his visit to Hong Kong in August 2011, announced numerous measures of the Central Government to support Hong Kong's financial development under the 12th Five-Year Plan. Among them, three are of particular concern to the finance and insurance sector, namely allowing investments in the mainland of China (Mainland) equity market by means of the Renminbi Qualified Foreign Institutional Investor (RQFII) scheme; facilitating fund management companies to launch exchange-traded funds constituted by Hong Kong-listed stocks on the Mainland's stock exchanges; and supporting Hong Kong's insurance companies to enter the Mainland market by means of setting up offices or taking up stakes. Under these circumstances, Beijing, Shanghai, Shenzhen and Hong Kong are at the doorsteps of New York and London for the top spot in the global financial centre arena. This paper aims at studying the subjects that are related to the development of financial centres and revealing the importance of information hinterland, geography of finance, as well as law and finance theory in the Chinese financial market, and the regulatory regime and legal quality in Chinese financial system.

The Theoretical Framework of Development of the World Financial Centres

A financial centre comprises a surplus of capital, a roughly offsetting deficit of capital and an intermediary agent or intermediation process. It can be considered as a grouping of a certain number of financial services together in a given urban space or in a functional description, a place where intermediaries coordinate financial transactions and arrange for payments to be settled (Cassis 2011). The emergence and locational movements of financial centres are not a new phenomenon in the modern era, in fact, it can be traced back to ancient times (Jarvis 2009). One of the oldest cities in the world, Samarkand (the second-largest city in Uzbekistan, located on the silk road between China and the Mediterranean countries), and other ancient cities like Babylon, Timbuktu (with its position as the southern terminus of trans-Saharan caravan routes) and Constantinople had functioned as major financial centres for intercontinental trade in their times. During the eighteenth and nineteenth centuries, larger financial centres such as London and New York emerged to serve regional and international markets as their volume of economic exchanges and the complexity increased (Ibid.).

The emergence of financial centres depends on numerous endogenous and exogenous factors. The size of domestic economy is one of the most important long-term development drivers of financial centres (Cassis 2011). For that reason, power transition and power diffusion of financial centres can be traced throughout history. For most of the nineteenth century, London was the leading worldwide financial centre. In the twentieth century, New York dominated the global financial scene until the 2008 subprime crisis. In the second half of the twentieth century, the emergence of several national, international and global financial centres have relied on their size of domestic economy or have taken the function as an intermediary for larger emerging economies, such as Tokyo, Hong Kong, Singapore and more recently Shanghai. Kindleberger (1974) was the first to use scale economies as a factor explaining the formation of a financial centre. He regarded scale economies in the organization of financial markets together with localized information, different time zones and discriminatory practices in business relations as major centrifugal forces. Two decades later, Krugman (1991) suggested four notable centrifugal forces: labour market externalities, demand for intermediate services, technological and information spillovers; which, as he stated, were the most important factors for the agglomeration of financial activities in financial centres. Although Krugman's opinion differs from Kindleberger's, one underlying idea is the same: scale economies or spillovers are significant factors for the formation of a financial centre. Gehrig (1998) analyzed both the centripetal and centrifugal forces in financial markets and suggested that economies of scale in the payment mechanism, information spillovers, liquidity and thick market externalities were major centripetal forces; while market access costs and coordination, rent-seeking and political intervention as well as localized information were centrifugal forces. He demonstrated that financial centres tend to be the host/gathering place of information sensitive financial activities in a region, while information insensitive sectors tend to relocate to low-cost suburban areas or to use low-cost communication media, such as computerized networks. These previous studies find that financial centres, like other agglomerations, are the outcome of both centripetal and centrifugal forces.

Path dependence, information hinterland and time zone are other important theories to interpret the development and change of financial centres in the globalization era. Path dependence refers to the historical accidents which would have long run cumulative consequences (David 1988, 1994). An initial locational pattern may simply be a historical accident, but once established, that pattern can become path dependent and ‘locked in’ through mechanisms of cumulative causation (Porteous 1999). In other words, once a city achieves a certain level of financial activity, it can sustain this advantage over other cities for a certain time. This theory explains why London remains the leading financial centre long after the decline of the British Empire (Porteous 1995). Besides path dependence, several scholars also paid attention to the importance of ‘information’ in the world financial market; to fill the knowledge gap, they drew attention to information hinterland in pursuance of explaining the rise and decline of financial centres over time (Porteous 1995; Wang et al. 2007; Zhao et al. 2004). The concept of ‘information hinterland’ defines a region for which a particular core city (financial centre) provides the best access point for the profitable exploitation of valuable information flows. In a dynamic sense, a financial centre is expected to grow from its information hinterland, and it will move and change as its information hinterland moves and changes (Zhao 2003, 2013). Time zone theory also catches the attention of scholars. Physiological and geographical studies revealed that human beings cannot change their life cycles. Time zones determine the daily work rhythm and behavioural patterns in different continents (Laulajainen 2003; Waterhouse et al. 2007; Zhao 2010, 2013). Hence, time zone is а significant factor influencing the development of financial centres. Since our world can be divided into three major time zones based on an eight-hour working day, the spatial distribution of global financial centres occurs in these time zones with each one having a dominating financial centre. London dominates in the European and African time zones, while New York reigns supreme in North and South America. At the moment, Asian time zones do not have a dominating financial centre; however, a table of financial centres is set to assume the status (Zhao 2010). Thus, the competition of international financial centres in the Asian time zone is very intense in terms of implication of time zone theory. As to the rise of China’s economy in the world, the emergence of an international financial centre in Asia must compete within China-related financial centres. Therefore, our article incorporates the size of the domestic economy, the information hinterland, path dependence, and time-zone theories together into a theoretical framework to explain the development of financial centres in China over time and their contributions to the global financial landscape.

A Brief Survey of the Important Financial Centres in China

Hong Kong, Beijing, Shanghai and Shenzhen have different functions and roles in China's financial framework in terms of their strengths and competitiveness in different financial markets. Investigation into their history, basic structures, major factors, financial markets, important industries and related areas and policies are important to identify and understand the competitiveness of these financial centres.

Hong Kong

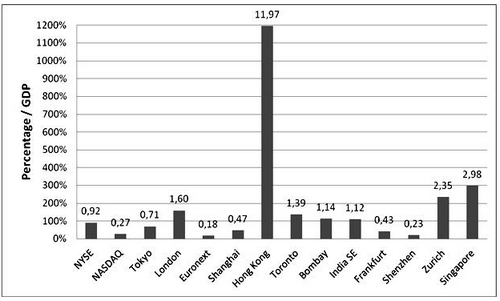

Hong Kong has a relatively stable political and social environment where capital is fully mobile, and the banking system is mature. Hong Kong's rule of law supports an open and transparent fund-raising platform for the world and particularly for Mainland enterprises. The fair, transparent and non-political legal and regulatory environment and institutions attracted many Mainland enterprises who seek to ‘go out’, either state-owned or private, to list their stocks in Hong Kong in order to introduce foreign capital into their business. In fact, with the stagnant economy of western countries and the vigorously growing economy of China after the subprime mortgage crisis in 2008, more and more foreign companies have considered to list on the Hong Kong Stock Exchanges (HKEx) in order to enjoy the growth of the Asian market. Although Chinese companies dominate Hong Kong's stock market, especially the large state-owned enterprises such as China Construction Bank, Industrial and Commercial Bank of China and China Mobile, HKEx still has 17 foreign listed companies, compared to Mainland's stock exchanges with zero foreign company listings. Hong Kong's stock exchange ranked 1st in the world with the benchmark against the size of the economy and under the ratio of market capitalization as percentage of GDP (Fig. 1). The common characteristics of a high market cap-to-GDP ratio in the world, such as Switzerland and Singapore, are that they serve as regional financial hub with unique financial services and functions, and have domestic companies with significant regional and international business. Hong Kong’s high market cap-to-GDP ratio is primarily due to the listing of Mainland enterprises in Hong Kong and many listed companies in Hong Kong have substantial investments in the Mainland and overseas markets. Thus Hong Kong is without doubt, a very special and important financial centre in the world. Hong Kong's IPO market has pushed ahead of others in recent years due to the fast growth of listings from Chinese companies. Chinese overseas IPOs mainly list on the HKEx Main Board (see Table 1), which promoted the total funds raised by IPOs in Hong Kong to rank 1st in the world in 2009 and 2010. The future of the HKEx is quite promising, as the role of Hong Kong as a gateway between China and the world continues to increase. China's financial integration into the global economy can bulk up Hong Kong's balance sheet more than that of other financial centres outside the Mainland in Asia.

Fig. 1. Top 10 and Selected Domestic Capitalization Stock Exchanges over GDP (the end of 2010)

Source: World Federation of Exchanges; World Bank database.

Table 1

IPOs from Overseas Chinese Companies (in 2009–2010)

|

|

2010 |

2009 | ||||

|

|

US$ billion |

|

US$ billion |

| ||

|

Stock Exchanges |

Fund raised by IPOs |

Average Fund raised by IPOs |

Number of IPOs |

Fund raised by IPOs |

Average fund raised by IPOs |

Number of IPOs |

|

HKEx Main Board |

28.83 |

0.41 |

71 |

24.84 |

0.48 |

52 |

|

NYSE |

2.63 |

0.12 |

22 |

0.46 |

0.09 |

5 |

|

NASDAQ |

1.26 |

0.05 |

23 |

1.48 |

0.18 |

8 |

|

SGX Main Board |

0.28 |

0.03 |

8 |

0.15 |

0.03 |

5 |

|

KOSDAQ |

0.18 |

0.04 |

4 |

0.10 |

0.03 |

3 |

|

FWB |

0.12 |

0.12 |

1 |

0.07 |

0.07 |

1 |

|

KRX Main Board |

0.00 |

0.00 |

0 |

0.04 |

0.04 |

1 |

|

SGX Catalist |

0.00 |

0.00 |

0 |

0.005 |

0.005 |

1 |

|

HKEx GEM |

0.00 |

0.00 |

0 |

0.004 |

0.004 |

1 |

|

Total |

33.29 |

0.26 |

129 |

27.14 |

0.35 |

77 |

Source: Chinese Enterprises IPO Reports, 2009–2010.1

Hong Kong's fund market is also very strong. For funds traded on both the stock exchange and the OCT market, Hong Kong outperforms Beijing, Shanghai and Shenzhen. Assets under management and the number of top 20 world private equity firms in Hong Kong are far greater than those of Beijing, Shanghai and Shenzhen. In fact, Hong Kong has become the second largest asset management centre in Asia, just after Japan. The well-established, mature and sophisticated asset management industry in Hong Kong matches China's needs and builds up safe investment channels for high foreign currency reserves and domestic savings. In the meantime, Hong Kong serves as the gateway for overseas investors to invest in the mainland of China. Mutual fund and insurance companies from western countries choose Hong Kong as the first place to expand their business in the Asia-Pacific region. Moreover, Hong Kong possesses the highest density and quality asset management talents in terms of higher percentage of people engaged in the financial sector among Asian financial centres (see Table 2). More than 80 per cent of the world's regional or international fund management companies set up their regional headquarters in Hong Kong and majority of fund companies based in Hong Kong are foreign institutions. This has contributed to rapid development of the asset management market in Hong Kong.

Table 2

Employments in the financial sector among the major financial centres (the end of 2009)

|

IFC |

Employments in Financial Sector (in thousand) |

Percentage in total population |

Year-end Resident Population of IFCs (in million) |

|

Greater London |

315.20 |

(4.11 %) |

7.66 |

|

New York City |

465.1 (July 1, 2008) |

(5.56 %) |

8.36 (July 1, 2008) |

|

Frankfurt |

74.271 |

(11.05 %) |

0.67 |

|

Tokyo |

269.00 |

(2.07 %) |

12.99 (1 October, 2009) |

|

Hong Kong |

212.70 |

(3.00 %) |

7.09 (the end of 2010) |

|

Singapore |

126.00 |

(3.37 %) |

3.734 |

|

Shanghai |

195.00 |

(1.01 %) |

19.21 |

|

Beijing |

182.70 |

(1.04 %) |

17.55 |

|

Shenzhen |

90.98 |

(1.02 %) |

8.91 |

Source: Based on the data from the above cities' statistics departments.

Hong Kong's prospect of becoming the largest offshore RMB bond centre in the world is promising. Contrary to the relatively small Hong Kong Dollar bonds market, the development of a RMB-denominated bonds market is important to the status of Hong Kong as an international financial centre. China also proactively promotes Hong Kong's bond market. Since 2007, the central government permitted Mainland financial institutions to issue RMB bonds in Hong Kong. In 2009, the measure was opened to the Chinese Ministry of Finance and the subsidiary companies in the Mainland of Hong Kong banks. From 2007 to 2009, having achieved consistent increases over these three years, a total of RMB 38 billion yuan-valued RMB-denominated bonds (including the national debt) were issued in Hong Kong. In 2010, yuan-valued RMB-denominated bonds reached about RMB30 billion yuan (He 2011). China, as part of its effort to internationalize its currency and open its financial markets, plans to allow Hong Kong insurers to invest in the Chinese inter-bank bond market and encourage Mainland companies to issue RMB bonds in Hong Kong.

The insurance industry in Hong Kong has continued to excel and grow in sophistication. Gross premiums routinely contribute to a total of 11–12 per cent of GDP, making Hong Kong the second largest insurance market in Asia after Japan. If measured by premium income alone, Hong Kong ranks the 25th in the world. The total number of insurance companies' headquarters, premiums, insurance density and insurance penetration in Hong Kong are larger than any financial centre in China (see Table 3). All of the world's largest reinsurance companies have longstanding offices in Hong Kong, including Munich Re, Swiss Re, General Re (Berkshire Hathaway), and Hannover Re. As in other sectors, significant regional offices are being built in Hong Kong mainly to cover the Chinese market (Pauly 2011). Among all the insurance business types, long-term insurance dominates Hong Kong's insurance market. The future growth of Hong Kong's insurance market lies in the economic rise of China and the openness of China's insurance industry. For many Hong Kong-based insurers that are not entirely focused on local businesses, their future plans are obviously shaped by developments in China. Insurers and reinsurers use Hong Kong as a base for regional operations for Hong Kong's transport links to Europe and North America, ease of access to the Mainland, solid legal regime and better living conditions. If Chinese insurers invest in foreign markets in the near future, Hong Kong will benefit from these investments because the possibilities for joint ventures with foreign insurers as well as for stand-alone Chinese insurance operations based in Hong Kong will be tremendous (Pauly 2011).

Table 3

Total number of insurance companies' headquarters, premiums, insurance density and insurance penetration in Hong Kong, Beijing, Shanghai and Shenzhen (the end of 2009)

|

Financial Center |

No. of insurance companies' headquarters |

Premiums (billion) |

Insurance density (per capita expenditure) |

Insurance penetration (premium as a % of GDP) |

|

Hong Kong |

– |

137.31 (HKD, the end of 2005) |

19796 (end of 2005) |

8.3 (end of 2005) |

|

Beijing |

13 |

697.6 (RMB) |

4044 |

5.9 |

|

Shanghai |

38 |

665 (RMB) |

4821 |

4.0 |

|

Shenzhen |

12 |

271.6 (RMB) |

3074 |

3.3 |

Source: China Insurance Regulatory Commission Shanghai Bureau 2009; China Insurance Regulatory Commission Beijing Bureau 2009; China Insurance Regulatory Commission Shenzhen Bureau 2009.2

In terms of the financial futures and derivatives markets, there is no doubt that Hong Kong outperforms other financial centres in China. Hong Kong's futures and derivatives market is open and well-established. It has the largest OTC derivative market in Asia, though the market is still relatively small compared to Europe and the United States. There are many different types of financial futures and derivative products traded in Hong Kong, while most of them do not exist in China. After the sub-prime crisis in 2008, the Hong Kong Securities and Futures Commission, Hong Kong government, Hong Kong Monetary Authority and the HKEx together plan to set up a regulation system for OTC derivatives in the near future. This project will definitely contribute to the further development of Hong Kong's derivative market.

Capital can freely flow in and out of Hong Kong due to the lack of controls on foreign exchange, which boosts Hong Kong's foreign exchange market. In 2010, Hong Kong was the sixth largest foreign exchange market in the world, the third largest in Asia behind Singapore and Japan. The Hong Kong foreign exchange market is even stronger than China's, not to mention those of Beijing, Shanghai and Shenzhen.

Hong Kong is one of the top-ten international banking centres in terms of the volume of external transactions, and the second largest in Asia after Japan. The banking sector plays a vital role in establishing Hong Kong as a major loan syndication centre in the region. In terms of the number of banks, banking assets and inter-bank turnover value, Hong Kong outperforms Beijing, Shanghai and Shenzhen. As a matter of fact, Hong Kong has become one of the highest concentrations of banking institutions in the world; seventy of the world largest 100 banks perform operations in Hong Kong. Its banking industry is more international and active than any other banking centre in China. In terms of multinational corporations (MNCs), Hong Kong possesses a larger number of MNCs and MNCs' regional headquarters than any other financial centre in China. At present, Hong Kong is an ideal place for MNCs to set up their headquarters.

Table 4

Multinational corporations in Hong Kong, Beijing, Shanghai and Shenzhen (the end of 2010)

|

|

|

Number of MNCs |

Number of MNCs' regional headquarters | |||

|

Hong Kong |

6612 |

1298 |

| |||

|

Beijing |

536 |

82 |

| |||

|

Shanghai |

837 |

305 |

| |||

|

Shenzhen |

400 (June 2009) |

n.a. |

| |||

Source: Jiang 2011; Statistics Bureau of Shenzhen Municipality 2009; Shanghai Industrial Real Estate Evaluation Research Centre 2010; Total number of multinational corporations' regional headquarters in Hong Kong 2010.3

To sum up, Hong Kong is strong in almost all financial markets. However, as is commonly known, Hong Kong is weak in its bond market and the Growth Enterprise Market. Due to the lack of development in Hong Kong's information technology and related industries, its Growth Enterprise Market grows very slowly, falling behind Shenzhen's ChiNext market. For over three decades, Hong Kong has been making desperate attempts in trying to promote its bond market; however, it is still far from enough. Its future growth lies in the internationalization of RMB and the economic rise of China.

Beijing

The importance of Beijing in China's financial framework is mysterious to many due to national capital functions including the control of currency policies and the dominance of state-owned enterprises and powerful organizations. Zhao (2003) and Zhao et al. (2004) argued that Beijing is the most important financial centre in China because of its role as the centre of financial policy-making. The number of foreign companies and their headquarters, foreign bank branches and representative offices, foreign direct investment (FDI), turnover of stock and securities transactions, deposits of financial institutions, loans of financial institutions and employment in finance, insurance and real estate illustrate Beijing's financial functions in China (Zhao et al. 2004; Wang et al. 2007). The great presence of Beijing in China's overall financial development demonstrates the strength of its financial centre. The forces underlying the formation of a financial centre were also analyzed, and it is found that asymmetric information created the need for geographic agglomeration of financial activities based on the source of information. Beijing, as the prime source of policy information, was more likely than other Chinese cities to be the national pre-eminent financial centre when the Chinese financial markets become more open to foreign firms in the near future.

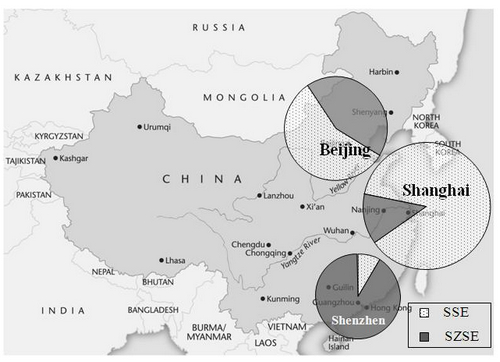

Beijing is a considerably strong financial centre in China although it does not have a stock exchange. It performed better than Shanghai and Shenzhen with regard to total fund-raising by equities, A-shares, IPOs and H-shares. Beijing's total market capitalization of A-shares also ranked the 1st in China. Besides, there are many large state-owned enterprises headquartered in Beijing, which contribute to the good performance of Beijing's securities market. The geographical distribution of Beijing, Shanghai and Shenzhen's listed companies on SSE and SZSE revealed that Beijing possesses the second largest number of listed companies in Chinese cities (Fig. 2). Newly listed Beijing companies in A-share and H-share markets dominate the market which is highlighted by the total fund-raised by A-shares, H-shares and IPOs. In addition, the total trading value was the second largest and raised capital of A-shares was the largest in China, representing the significance of Beijing in the Chinese stock market (see Table 5).

Fig. 2. Geographical distribution of listed companies in Beijing, Shanghai and Shenzhen (April 2010)

Source: Shanghai Stock Exchange Monthly Report, 2010; Shenzhen Stock Exchange Monthly Report, 2010.4

Note: SSE = Shanghai Stock Exchange; SZSE = Shenzhen Stock Exchange.

Table 5

Regional distribution of stock turnover and IPOs of A-Shares (2008)

|

|

Turnover Value (RMB million) |

Issued Volume (million share) |

Total Issued Volume in China (%) |

Raised Capital (RMB million) |

Of total raised capital in China (%) |

|

Beijing |

8410.91 |

6988.53 |

60.79 |

54686.12 |

52.87 |

|

Guangdong |

7827.09 |

593.69 |

5.16 |

6502.75 |

6.29 |

|

Shanghai |

9111.26 |

110 |

0.96 |

1895.60 |

1.83 |

|

Beijing's bond market is the largest in China. Bonds in China are traded on both stock exchanges and the OTC market, and more than 90 per cent of bonds are traded on the latter. Since Treasury Bonds (T-bonds) are issued by the Ministry of Finance in China and bills/notes are issued by the People's Bank of China, which are headquartered in Beijing and share half of the total outstanding amount of bond classes in China (Wang et al. 2010),6 the role of Beijing in China's bond market is significant and irreplaceable. Moreover, four big commercial banks, 13 joint-stock commercial banks and more than 100 state-owned companies are headquartered in Beijing, such as China Unicom, China Mobile and China National Petroleum Corporation. The large total issuance of T-bonds and corporate bonds make Beijing considered as the largest bond market in China.

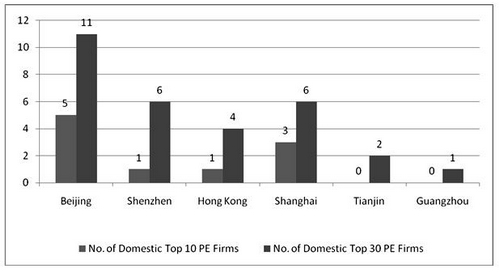

The Private Equity (PE) fund industry in Beijing performs very well because of the asymmetrical information existing in the market. As the financial policy and supervision centre, Beijing receives information and policy trends of the financial industry almost instantly (Deng 2010). More importantly, the unique role of Beijing as the policy-maker and the place of financial supervision institutions enhance the importance of private equity in Beijing. The total number of world's top 20 private equity firms in Beijing was the largest in Mainland China but less than that of Hong Kong (see Table 6). Beijing had the largest amount of both the number of PE funds' investments and investment amounts of PE funds in China. The total number of domestic PE funds in Beijing was also the largest (Fig. 3). Beijing outperforms in the PE fund industry any other cities in China; it received more than half of all industrial funds licensed by the central government. In addition, a great majority of large PE investment institutions at home and abroad have headquarters in Beijing.7 The reason for this phenomenon is that companies going public should get approval from the China Securities Regulatory Commission, which is located in Beijing. Profit-earning of the PE investment is driven by exploring and acquiring asymmetrical information in the market, those information-sensitive overseas and domestic PE Firms are thus attracted to Beijing to take advantage of the information flow.

Table 6

Presence of Top 20 world private equity firms in Beijing, Shanghai, Shenzhen, Hong Kong, New York and London (2009)

|

Rank |

Firm name |

Beijing |

Shanghai |

Shenzhen |

Hong Kong |

New York |

London |

|

1 |

TPG |

Y |

Y |

N |

Y |

Y |

Y |

|

2 |

Goldman Sachs Principal Investment Area |

N |

N |

N |

Y |

Y |

Y |

|

3 |

The Carlyle Group |

Y |

Y |

N |

Y |

Y |

Y |

|

4 |

Kohlberg Kravis Roberts |

Y |

N |

N |

Y |

Y |

Y |

|

5 |

Apollo Global Management |

N |

N |

N |

Y |

Y |

Y |

|

6 |

Bain Capital |

N |

Y |

N |

Y |

Y |

Y |

|

7 |

CVC Capital Partners |

Y |

Y |

N |

Y |

Y |

Y |

|

8 |

The Blackstone Group |

Y |

Y |

N |

Y |

Y |

Y |

|

9 |

Warburg Pincus |

Y |

Y |

N |

Y |

Y |

Y |

|

10 |

Apax Partners |

N |

Y |

N |

Y |

Y |

Y |

|

11 |

First Reserve Corporation |

N |

N |

N |

N |

N |

Y |

|

12 |

3i |

Y |

N |

N |

N |

Y |

Y |

|

13 |

American Capital |

N |

N |

N |

Y |

Y |

Y |

|

14 |

Hellman & Friedman |

N |

N |

N |

N |

Y |

Y |

|

15 |

Providence Equity Partners |

N |

N |

N |

Y |

Y |

Y |

|

16 |

Advent International |

N |

N |

N |

N |

Y |

Y |

|

17 |

Terra Firma Capital Partners |

N |

N |

N |

N |

N |

Y |

|

18 |

General Atlantic |

Y |

N |

N |

Y |

Y |

Y |

|

19 |

Fortress Investment Group |

N |

N |

N |

N |

Y |

Y |

|

20 |

Silver Lake |

N |

N |

N |

Y |

Y |

Y |

|

|

Total |

8 |

7 |

0 |

14 |

18 |

20 |

Note: Y = Yes, N = No.

Source: The 2009 PEI 300, 2009.8

Fig. 3. Number of domestic private equity firms of the year 2010 in China

Source: Zero2IPO Group.9

The insurance market of Beijing and Shanghai has developed well. For premiums, insurance density and penetration from 2003 to 2005, Beijing functioned better than Shanghai. Before 2007, the premium income and insurance penetration of Beijing were larger than those of Shanghai; however, Shanghai's insurance payment and density were larger since 2007. In 2009, total premium income and insurance penetration of Beijing were larger than those of Shanghai and Shenzhen (see Table 3), and the total number of branches of insurance companies in Beijing remain the largest in China. The headquarters of major insurance companies such as China Life, The People's Insurance Company Group, Taikang Life and Xinhua Life, reside in Beijing. There is more than 4000 billion yuan in total assets of the insurance industry in China, with 50 per cent coming from Beijing and around 25 per cent from Shanghai. The headquarters of the China Insurance Regulatory Commission in Beijing provide a unique environment for insurance companies to have rapid access to tactical information for policy making. In addition, a great many large state-owned enterprises are located in Beijing, which is beneficial for extending insurance businesses and for communication and cooperation among different companies.

Beijing's banking industry is the largest in China as Beijing is the centre for domestic banks, and the four major commercial banks, policy banks as well as a lot of regional banks are concentrated in Beijing. With respect to the banking industry, Beijing is rather strong as a domestic banking centre despite its underdevelopment in foreign banking (see Table 7).

Table 7

Domestic and foreign banking sector in Beijing, Shanghai and Shenzhen (the end of 2009)

|

|

financial centre |

No. of banking institutions |

No. of people working in these institutions |

No. of corporate bodies |

|

Domestic Banks* |

Beijing |

3399 |

82779 |

45 |

|

Shanghai |

3060 |

75204 |

45 | |

|

Shenzhen |

1224 |

44539 |

22 | |

|

| ||||

|

Foreign Banks |

Beijing |

81 |

6069 |

6 |

|

Shanghai |

n.a. |

n.a. |

18 | |

|

Shenzhen |

81 |

4231 |

4 | |

Note: * No. of domestic banking institutions includes branches; Business networks do not include headquarters.

Source: China Banking Regulatory Commission.10

The predominance of Beijing in the Mainland's domestic banking industry can be reflected from the interbank market, as Beijing's monthly turnover value was about twice as large as the total value of Guangdong and Shanghai.11 By the end of May 2011, with respect to the number of Fortune 500's global headquarters (though they largely belong to PRC's mega-sized state-owned enterprises), Beijing ranked 1st even exceeding those of London and New York.

In summary, Beijing's role as a financial centre cannot be underestimated. Beijing is quite strong in the stock market, bond market, PE fund market and insurance market. Beijing has become a large domestic banking centre and an ideal place for MNC headquarters (see Table 4). The functions and roles of Beijing are unique and incomparable in Chinese specific financial framework.

Shanghai

The tertiary sector has gained the dominant position in Shanghai's economy with the contraction of the secondary sector. The secondary sector in 1978 accounted for well over 70 % of Shanghai's economy and has since downsized to 39 % in 2010. The tertiary sector has expanded since 1978 from 23 % to account for 59 % of Shanghai's total GDP in 2010 (Luo 2012); commerce and financial services make up the top two subsectors within the tertiary sector, indicating the rise of Shanghai as an important financial centre.

Shanghai has its advantages in a higher rate of economic growth with a much larger bond market, a sizeable commodity market and a well-diversified industrial structure. In comparison to Hong Kong, Shanghai does not have a fully convertible currency, transparent and non-political regulatory regime and rule of law, however, its sizeable domestic economy and financial markets prop up Shanghai as a major domestic financial centre in China.

Shanghai is considered as the capital centre in China as its financial markets are well established and diversified under a joint endeavor of central and municipal governments. The Shanghai Stock Exchange (SSE) has grown very rapidly over the past decade. Therefore, it is important to investigate Shanghai's stock market. Having made a comparison of the stock markets of Beijing, Shanghai and Shenzhen, we can note that Shanghai ranked 1st with respect to the total number of listed companies, of listed H-shares companies, the total number of fund companies' headquarters and securities companies' headquarters, total stock turnover value and so forth. Compared to Beijing, Shanghai has more listed companies on Chinese stock market and H-share market; however, the funds raised by newly listed companies were smaller than that of Beijing because the central government proactively encourages state-owned enterprises to list outside China. Shanghai's stock market has its own advantages, therefore it is impossible to define their rankings. The ostentatious prosperity of Shanghai's stock markets is due to its sizeable domestic economy under the Yangzi River Delta economic zone. Several studies have showed that companies listed in China tend to list on their neighbouring stock exchanges (Fig. 2). According to the Chinese statistical yearbook, in 2010, the GDP per capita of Shanghai, Jiangsu and Zhejiang were ranked in China's top five. Shanghai shareholders is the main source of shareholders in SSE's stocks, accounted for about 25 per cent. That is because most mass investment capitals in China usually go to the stock market and real estate industry due to the inconvertibility of the RMB and lack of investment producers provided by the banking sector.

Shanghai's fund market performed better than those in Shenzhen and Beijing. The first listed investment fund in China – Zibo Town and County Enterprises Fund – was listed on the SSE in 1993; the first listed open-end fund was launched by the China Southern Fund and the first Exchange Traded Fund (ETF) – Huaxia SSE 50 ETF was listed in 2010; the first two China-listed tracking Hong Kong stock indices ETF was launched in June, 2012 and listed on SSE and Shenzhen Stock Exchange (SZSE) simultaneously in October 2012. Although the ETF was first launched on the SSE in 2005, its turnover value grew very fast and exceeded that of the HKEx in 2009. The reason is that the Central Government has been positively pushing the financial development of Shanghai over the past decade in an effort to expand the influence of Shanghai in the world as well as to upgrade its image and status as an international financial centre. Assets under management and total number of fund companies of Shanghai ranked 1st in China (see Table 8). Shanghai's fund companies occupy half of the market share of assets under management in China. For funds traded on stock exchanges, the SSE was better than the SZSE in terms of turnover value and volume because Shanghai enjoys special policies initiated by the central government to build itself as an international financial centre. In May 2009, the Central People's Government of China published an official document, aiming at promoting the development of financial institutions in Shanghai, including mutual fund management companies. This policy is greatly beneficial to Shanghai to develop its fund industry. As these supportive policies are put into practice, the financial information platform is well equipped and once the related laws and rules are up to international standards, Shanghai will enjoy a faster growth of its fund market.

Table 8

Number of fund companies in Beijing, Shanghai and Shenzhen

|

|

The end of March, 2010 |

The end of 2008 | |

|

City |

Number of Fund Companies |

% of number of total fund companies in China |

Number of Fund Companies |

|

Beijing |

7 |

12 % |

7 |

|

Shanghai |

30 |

50 % |

30 |

|

Shenzhen |

16 |

27 % |

17 |

Source: China Securities and Futures Statistical Yearbook 2009;12 Deng 2010.

The development of an insurance industry in Shanghai is the fastest in China. As a matter of fact, the rapid development of the insurance headquarters economy is a part of the strategy of Shanghai's goal to become an international financial centre by the end of 2020. In April 2010, the central government announced ‘Opinions on Promoting Shanghai to Speed up the Development of Modern Service Industry and Advanced Manufacturing, Building an International Financial Centre and the Views of an International Shipping Centre’. This is the first time that China's central government purposefully made policies to build Shanghai as an international financial centre and shipping centre. Shortly after the announcement, Wu Dingfu, at that time the chairman of the China Insurance Regulatory Commission, proclaimed that the commission would support Shanghai to develop China's insurance products innovation and technology research and development (R&D) centre as well as insurance management and logistics centre. By May 1991, the China Pacific Insurance Group was set up in Shanghai, which laid a foundation for the development of insurance industry there. The Shanghai municipal government puts greater efforts in promoting the development of an insurance headquarters economy in order to promote faster development and healthier industrial structure of the insurance sector. The favourable policies not only enhance the political environment for the insurance industry, but also help attract more national and international insurance companies to settle down in Shanghai. The efforts are paying off. The Ping An Group, headquartered in Shenzhen, set up a second headquarters in Shanghai, and moved four of its eight subsidiaries' headquarters to Shanghai. For Ping An Insurance of China, Shenzhen is its administrative centre, while Shanghai is the profitable centre (Tong 2009). Total assets of Shanghai's insurance industry have also increased. By the end of 2007, Shanghai's insurance companies' total assets accounted for about 25 per cent of China's insurance industry's total assets. The most evident advantage of Shanghai's insurance industry rests on its financial market and trading. Shanghai has several important financial markets and exchanges: the Shanghai Stock Exchange, Shanghai Future Exchange, Shanghai Gold Exchange, Foreign Exchange market, etc. As the concentration of these financial markets and exchanges increase, Shanghai has become an important place to insure capital in China.

Shanghai has become the foreign banking centre of China. It possesses the largest number of foreign banks' headquarters, deposits and loans of foreign financial institutions in China. By 2009, 191 foreign firms had established regional headquarters in Shanghai, far exceeding the numbers in Beijing and Shenzhen. Although nation-wide banks locate their headquarters in Beijing for the advantage of access of tacit information from the central government's banking bodies, the majority of China's banks are listed on SSE. While Beijing is strong in the domestic banking industry, Shanghai has the largest number of foreign banks' corporate bodies in China. As for the number of domestic banking corporate bodies, Shanghai is equivalent to Beijing. In 2005, People's Bank of China set up the Shanghai Head Office to govern the rapidly growing operations and business of domestic and foreign banking bodies in Shanghai. Historically, Shanghai had opened corporate RMB business to foreign banks earlier than Beijing. Foreign banks that entered China's market in the early stages preferred to locate their headquarters in Shanghai. These foreign banks mainly focus on retail business, and most of them are concentrated in the rich YRD region since the Pearl River Delta market was already covered by Hong Kong's banks. In fact, foreign banks that entered the Chinese market in 2007, all set up their headquarters in Shanghai. Many foreign banks that entered China's market after 2007 still chose Shanghai as their headquarters, including Hong Kong Hang Seng Bank and DBS. By the end of 2010, eight out of ten big foreign banks set up their headquarters in Shanghai (Zhang and Zhang 2011). The concentration of foreign banks in Shanghai can be expressed in the total deposits and loans of foreign institutions, which absorbed over 80 per cent market share of total deposits and loans of all foreign companies in China.13 Shanghai's banking sector is quite promising as it attracts the largest number of foreign banks as well as the majority of foreign bank businesses, making it the second largest banking centre in China.

The headquarters of China's foreign exchange trading system is located in Shanghai and preforms differently from that of other financial systems. The China Foreign Exchange Trading System (CFETS), also known as the National Interbank Funding Centre, is a sub-institution of the People's Bank of China. Its core functions include providing trading, information and services for the operation and transmission of the central bank's monetary policies. The CFETS also serves as a benchmark to the interbank lending, bond and foreign exchange markets. China's first foreign exchange futures were issued by the Shanghai Foreign Exchange Transactions Centre in 1992. The products of foreign exchange futures included RMB to the US dollar, pound, euro and yen. The trading of foreign exchange derivatives in China has increased rather quickly in recent years. The total turnover value of foreign exchange swaps and forward foreign exchange in Shanghai outperformed that of Beijing and Shenzhen.14 Shanghai's share of financial futures, options, foreign exchange market and being home to China's Financial Futures Exchange, the only future exchange in China, have made Shanghai a financial powerhouse in more ways than its Beijing and Shenzhen counterparts.

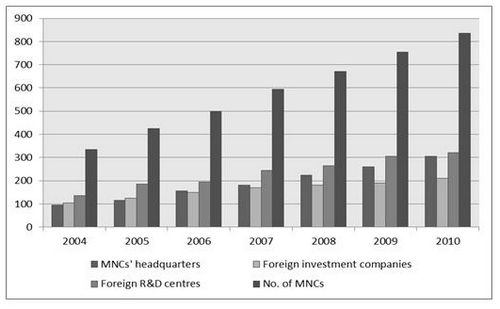

Shanghai is an attractive place for MNCs to do business in China. By the end of 2010, there were 213 foreign investment companies, 319 foreign R&D centres and 305 MNCs' regional headquarters (see Fig. 4). Among them, 74 were Fortune 500 companies' regional headquarters. Shanghai has already become a financial centre that possesses the largest number of MNC headquarters in China.15 Before 2002, there were no MNC's regional headquarters in Shanghai. However, the number grew to 319 by the end of 2010. The growth in the number of MNCs regional headquarters in Shanghai can be partly attributed to Shanghai's preferential policies. In 2002, with the support of the Ministry of Commerce of China, Shanghai Municipal People's Government promulgated the ‘Shanghai Municipality, Encouraging the Establishment of Regional Headquarters by Foreign Multinational Corporations Tentative Provisions’. As more and more foreign companies enter and set up their regional headquarters in Shanghai, the total number of foreigners has increased to over 140,000 by the end of July 2008, accounting for about 30 per cent of total foreigners in China. In 2008, the Shanghai government revised its previous policy, in hopes to improve MNC's access into Shanghai's market issued ‘The Provisions of Shanghai Municipality on Encouraging Multinational Corporations to Establish Regional Headquarters in Shanghai’. This new policy simplifies the exit and entry procedures of MNCs' top foreign managers. At the end of 2008, the Shanghai government once again promulgated ‘Several Opinions Regarding the Implementation of the Provisions on Encouraging the Relocation of Regional Headquarters in Shanghai’ by attracting Multinational Corporations Headquarters. In the document, the government clearly states that if MNC's set up their regional headquarters in Shanghai, they will enjoy preferential policies. Apart from the Shanghai Municipal People's government, several districts and counties of Shanghai also issued related preferential policies to attract MNCs' regional headquarters. The future development of a headquarters economy in Shanghai is promising.

Fig. 4. MNCs' headquarters in Shanghai (2004–2010)

Source: Shanghai Headquarter Economy and the Development of Headquarter Business Park Report 2010 (by Shanghai Industrial Real Estate Evaluation Research Centre).

Shanghai's continuous preferential policies enhance its status as an important financial centre for MNCs and their headquarters. Apart from policies, Shanghai has other advantages that outperform other financial centres in China. In April 2011, the European Union Chamber of Commerce in China and the Roland Berger Strategy Consultants together published the ‘European Business in China: Asia-Pacific Headquarters Study 2011’. Shanghai, due to its proximity to the sizable domestic market, was at the top of the list for being one of the most attractive locations in the Asia-Pacific region for multinational companies to establish their regional headquarters. Charles-Edouard Bouée, President in Asia and Member of the Global Executive Committee of Roland Berger Strategy Consultants, stated that with the gradual global economic shift towards the Asia-Pacific region, many multinational companies attribute increasing strategic importance to this region, especially as regional GDP and consumer demand growth rates exceed those in other regions. In line with this trend, more and more companies are establishing their regional headquarters in the Asia-Pacific region. Whereas this step also reflects China's growing importance in the world and the significance of Shanghai as the largest business and financial centre in China.

Shenzhen

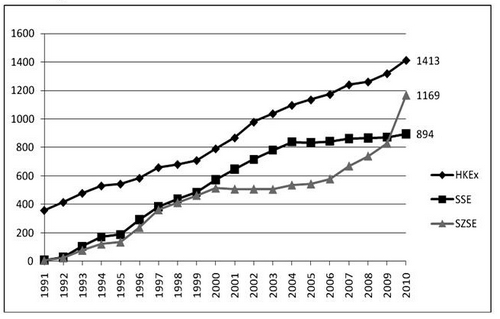

Shenzhen has many advantages over other financial centres in China, including its advantage of the small and medium enterprise (SME) board and the ChiNext, China's NASDAQ-style stock market on SZSE. The ChiNext was found in 2009, which was designed for high-growth companies that do not fit for the listing requirements of the SSE. Shenzhen's ChiNext board has become the world's third largest market for growth enterprises due to its proximity to Hong Kong and the irreplaceable experimental role of financial innovation in China. The SME board's uniqueness and the ChiNext's suitability in the Chinese market make both operations grow rapidly. Although it was founded only three years ago, ChiNext have already outperformed the HKEx Growth Enterprise Market in all aspects. ChiNext, in terms of market capitalization and trade value, became the largest one among the similar boards in Asia. Although the public and various scholars criticized the fact that the ChiNext still has the old problems of China's capital market, like overvaluation and speculative fever, the establishment of ChiNext has attracted many growing companies to be listed on SZSE. In 2010, the number of listed companies in SZSE exceeds that of the SSE (see Fig. 5).

Shenzhen is considered as the most important fund centre in China due to its proximity to Hong Kong. According to ‘The Outline of the Plan for the Reform and Development of the Pearl River Delta’ announced by the National Development and Reform Commission, a regional financial centre is the national Strategic Positioning for Shenzhen. The future position of Shenzhen is to cooperate with Hong Kong and become the Chinese private wealth management centre. Shenzhen has a lot of investment and management companies, and private equity and venture capital funds are the advantage of its fund industry. What is more important, the Shenzhen government announced ‘The Regulations on Promoting the Development of the Private Equity Industry’ to support the development of its private equity funds. This was the first time the municipal government clearly highlight its support for the private equity fund industry.

Fig. 5. Number of listed companies on HKEx, SSE and SZSE (1991–2010)

Source: Securities and Futures Commission 2010; Hong Kong Exchanges and Clearing Fact Book, various years; Shanghai Stock Exchange Statistics Annual, various years; Shanghai Stock Exchange Monthly Report, January 2007 – December 2010; Shenzhen Stock Exchange Fact Book, various years.16

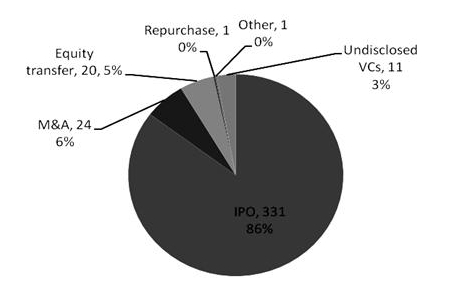

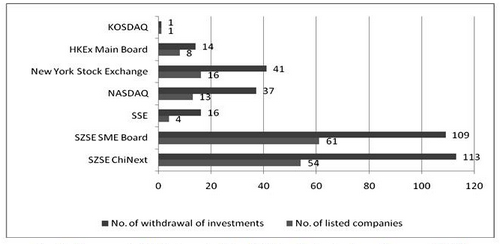

Venture Capital (VC) funds in Shenzhen are active and suit the needs of growing companies. Shenzhen has become the biggest venture capital hub in China with the total number of VC fund companies ranking first in 2010. VC is financial capital provided to early-stage, high-potential, high risk, and growing start-up companies. The investment model of VC funds puts money by bartering for an equity proprietorship in the invested companies, which usually have a modern technology or business model in high tech industries, such as biotechnology, information technology and software. In China, venture capital funds are heavily invested in the high-tech industry, whereas private equity funds tend to invest in more diversified industries. The recent investment models and characteristics of VC funds in China are inclined to invest in the newly listing small, medium and growing companies. VC usually claims back the funds from the investment after earning satisfactory profits; and the primary exit route for VC is IPO. There were 331 IPOs supported by 157 VC companies, accounted for 86 per cent of the total number of withdrawals in 2010. In China, the establishment of ChiNext on the SZSE promotes the development of VC funds as the exit or withdrawal of VC funds becomes easier. Just in 2010, the total number of VC investments and VC investment amounts were 526 and US$ 2.72 billion respectively, accounting for 64.4 per cent and 50.5 per cent of the total number of VC investments and their amounts in China. ChiNext as well as the SZSE SME board has become the primary destination of VC investments. The major exit route for VC funds to claim back money from investments in China goes through IPOs, which accounted for a majority proportion of the total number of withdrawals (Fig. 6). In 2010, there were 157 companies listed on stock exchanges at home and abroad by IPOs through 331 investments of VC funds. In the Chinese market alone there were 119 companies listed on the SSE and SZSE by IPOs supported by the VC companies' investments (Fig. 7). At the end of 2010, half of the top 20 domestic venture capital firms were situated in Shenzhen, making Shenzhen the biggest venture capital hub in China, surpassing Beijing and Shanghai.

Fig. 6. Exit routes of VC funds in China (2010)

Source: Zero2IPO Group 2010b.17

Fig. 7. Corporate IPOs invested by VC funds in stock exchanges (2010)

Source: Zero2IPO Group.

Shenzhen is an experimental zone for financial innovations in China. Shenzhen has a long history on implementation of reforms and opening up policies ahead of other cities in China since it was designated as a Special Economic Zone in the 1980s. At the early stage of development, Shenzhen provided many preferential policies to attract FDI. Processing trade industries (processing with materials, assembling supplied components, and then exporting the final products to overseas markets) were very popular in Shenzhen in the 1990s due to its proximity to Hong Kong. Many Hong Kong industrialists moved their production processes to Shenzhen seeking lower production costs. Hong Kong enterprises brought advanced management concepts, new modes of operation and so forth to Shenzhen. These indirect effects were beneficial for Shenzhen's economic growth and attractiveness to other foreign MNCs. Hong Kong's enterprises had become innovators, generated investment and nurtured Shenzhen's business environment, making it easier for foreign enterprises to do business in China regions. The prosperity of foreign investment initiated domestic investment and attracted a lot of money from other parts of the Mainland to invest in Shenzhen from spheres such as real estate, logistics, financial industries, etc. Hong Kong remains the largest source of FDI in Shenzhen. By the end of 2010, there were about 42,000 Hong Kong companies in Shenzhen and US$ 60 billion in FDI from Hong Kong, accounting for 80 per cent of the total foreign companies and two-third of the total FDI in Shenzhen.

Apart from Hong Kong's contribution, Shenzhen municipal government actively conducts a preferential policy to attract foreign companies setting up their headquarters. In 2007, the Shenzhen municipal government promulgated ‘Some Opinions on Accelerating the Development of Headquarter Economy in Shenzhen’ which states that any company that establishes its headquarters or moves to Shenzhen will get support from the government in financing, use of land, human resources as well as the simplification of related procedures. In fact, under a lot of foreign investments and new technologies, Shenzhen itself cultivated several global corporations, like Huawei technologies, ZTE Corporation, BYD, Tencent, China Merchants Bank and Ping An Insurance. The function and role of reforms and opening-up frontier moved Shenzhen forward to become an experimental zone for financial innovation in China, especially of the pilot plan approved by the central government for the development of Shenzhen-Hong Kong Modern Service Industry Cooperation Zone in Qianhai. Internally, the Shenzhen municipal government also provided different kinds of preferential policies to promote financial innovation. For insurance industry the Shenzhen government issued ‘Measures for Accreditation of Headquarter Enterprises in Shenzhen (Trial)’ and the ‘Detailed Implementation Rules of Several Opinions on Accelerating the Development of a Headquarter Economy in Shenzhen (Trial)’ in October 2008, which provides 5 billion RMB to award enterprises that would set up or move their headquarters to Shenzhen in the next five years. This preferential policy is the direct reason for the movement of China Life to Shenzhen (Tong 2009). As a matter of fact, China Life Insurance (Overseas) had already moved its headquarters from Beijing to Shenzhen since 2007 on the consideration of other favouring aspects of Shenzhen. Aside from the preferential policy, one of the reasons for insurance companies to move their headquarters to Shenzhen is the good investment environment and unique institutional innovation, which is beneficial for the development of insurance business. Shenzhen's government supports the innovation development of its insurance industry and have made Shenzhen into a major experimental place of insurance innovation development in China (Xiao 2010). Another favourable factor is Shenzhen's close proximity to Hong Kong which enhances the flow of talented people between Hong Kong and Shenzhen and allows Shenzhen's financial industry to learn from Hong Kong's advanced financial practices.

The Strengths and Potential Cooperation of Financial Centres in the Greater China Region

Based on the various strengths and competitiveness of Hong Kong, Beijing, Shanghai and Shenzhen in different financial sectors, this part will discuss the direction of development and opportunities for cooperation among the financial centres in the Greater China region. Hong Kong, Beijing and Shanghai are in a similar position with respect to the stock markets in terms of the regional distribution of listed companies and turnover values in China. As for the bond market, Hong Kong and Beijing have achieved a similar level. Regarding the whole fund market, Hong Kong was in the first position due to the participation of the world’s leading fund houses. Hong Kong is also the number one insurance market in the Greater China due to its exuberant and multi-dimensional insurance industry. Beijing and Shanghai are in similar positions on commodity future market and rapidly growing owing to the Chinese economy's continuous brisk advancement. Hong Kong still ranks first in the foreign exchange and related derivatives market among the financial centres in China, but for the on-shore foreign exchange market in the Mainland, Beijing ranks the first because of the foreign exchange controlled by the central government bodies. Beijing's banking sector is similar to the foreign exchange market. Hong Kong is a top-ten international banking centre in terms of the volume of external transactions, but Beijing is the Chinese banking centre as the ‘Big Four’ state-owned commercial banks, policy banks as well as majority of the domestic banks' headquarter are all concentrated in Beijing. Although many financial markets are relatively weak in Shenzhen compared to Beijing and Shanghai's scales and advantages, the functions of Shenzhen in the VC market and in financial innovation are highly important to China's financial development. Hong Kong is a vibrant international financial centre invigorated by a sophisticated financial infrastructure, world-class financial professionals, a robust regulatory regime, high liquidity and efficiency. Beijing, Shanghai and Shenzhen are powerful in providing domestic financial services for foreign investors to invest in the Mainland's markets. Together they serve the massive rise of China's economy that increasingly captures the global investors' attention and that has become one of the most robust emerging markets in the world. In general, Hong Kong together with Beijing, Shanghai and Shenzhen will represent the league or fleet of financial centres and services in China and perform unique and incomparable financial functions in Asia and the world financial system. Besides, Hong Kong and the Mainland financial centres can strive for cooperation in several financial products and segment markets. With different complementary advantages they will together serve well for investors from Asia and all over the World.

Hong Kong's practice in common law system, similar to the institutional system in London and New York, provides the best basis for financial development and economic growth according to comparative studies on Anglo-American Common Law system and European Civil Law system (La Porta et al. 1997, 1998; La Porta, Lopez-de-Silanes, and Shleifer 2008). Hong Kong's history as a British colony compels the continuance and maintenance of its common law system, rules of equity, ordinances, subordinate legislation and customary law after the establishment of Hong Kong as a Special Administrative Region in 1997 (Zhao 2010). Hong Kongs legal system is comparable to those financial centres which adopted Anglo-American common law, such as New York and London, whereas China uses the European Civil Law system. Several scholars found that those financial centres that adopt Anglo-American legal system tend to be market-led and put priority on the protection of shareholders, but the financial centres applying the Continental legal system incline to bank-led financial centres and mainly protect the interests of creditors (Levine 1998; Ergungor 2004). As a matter of fact, civil law countries have both the weakest investor protections and the least developed capital markets compared to common law countries; ‘because a good legal environment (good investor protection) protects the potential financiers against expropriation by entrepreneurs, and it raises their willingness to surrender funds in exchange for securities, and hence expands the scope of capital markets’ (La Porta et al. 1997: 1149). Rajan and Zingales (1998) also find that countries with better developed financial systems show superior growth in capital-intensive sectors that rely particularly heavily on external finance. In short, stock markets operating under the Anglo-American legal system perform better than those under a Continental legal system. Under the Anglo-American legal system, stock markets achieve capital growth over the years; whereas the stock markets with a Continental legal system only protect the principles of capital or even result in loss of money at times (Zhao 2010). Thus, companies listed on HKEx achieve capital growth through the times, while those on the SSE and SZSE experience capital losses.

Shanghai's financial industry is catching up Hong Kong, but the market environment in the Mainland still has several problems due to insufficiencies of regulatory enforcement and supervision integrity. State-owned enterprises dominate the market with their total assets and businesses taking up around 90 per cent of total assets and businesses of Shanghai and Shenzhen's financial markets. However, there are more than 200 listed companies subjected to security enforcement actions by China Securities Regulation Commission of the SSE and SZSE since 1992. Zhang (2004) pointed out that the fundamental reason is the regular scandals in financial markets. One of the most essential features of the ownership of Chinese listed companies is the dominance of the substantial shareholders. There is no effective and practical mechanism to monitor and restrict the substantial shareholders under the civil law system as they can expropriate the minority shareholders for private benefit. For example, HKEx has a corporate governance code to enforce accountability of issuers (the listed companies) and their directors, which was written and amended by the HKEx after consultations with listed issuers, market practitioners, and professional and industry associations. In fact, the Mainland's financial centres are weak in regulatory enforcement, supervision, and requirement of information disclosure; the finance-related industries, including accounting, law, financial services, etc. lack their own integrated industry codes of conduct. Therefore, scandals of Chinese listed companies show the potential for fraud and glitches in the regulatory and legal systems as well as the fiasco of corporate governance in China.

Under these circumstances, there is a room for cooperation among the HKEx, SSE and SZSE. Companies listed on the HKEx are more transparent under a better regulatory and legal system; while those listed on the SSE and SZSE are not transparent enough as we can judge from those common scandals of listed companies in China. There were 80 A and H dual-listed companies in Hong Kong by the end of 2012, about two-third of them are state-owned enterprises. That means that these dual-enterprises are governed by HKEx, and SZSE/SSE's listing rules and related listing regulations. The HKEx, SZSE, SSE, and the regulatory bodies, Hong Kong Securities and Futures Commission and China Securities Regulatory Commission could jointly establish a united regulatory and supervisory standard and build up an information exchange system for disclosure of price sensitive information for these dual-listed companies, in order to enhance listing regulations and supervision in Hong Kong and the Mainland's financial centres, and strike a reasonable balance between ensuring market transparency and safeguarding the legitimate interests of state-owned listed corporations in preserving certain information in confidence to facilitate their operation and business development. In fact, building Hong Kong-Shanghai-Shenzhen joint cooperation on listing regulation and supervision on a par with international standard could help promote a continuous disclosure culture among listed corporations to enhance market transparency and quality in the Mainland's financial centres, and to bring Shanghai and Shenzhen's regulatory and supervision regime for listed corporations more in line with other international financial centres, and to enhance Hong Kong's strength as a premier capital formation platform.

The collective formulation of a sophisticated trading platform and/or sub-stock exchange in Qianhai, Shenzhen for the ChiNext of Shenzhen could provide a safe and more resilient financing channel for high-tech and high-growth enterprises in Hong Kong and the Mainland on the basis of complementing existing strengths of both sides. The Hong Kong Growth Enterprise Market (GEM) was established in 1999; unfortunately, it was immediately hit by the burst of the dotcom bubble, resulting in its sluggish performance either in number of listed companies, or in market capitalization, or in trading value. In fact, the investment banks and PE and VC funds prefer the Mainland's high-tech/high-growth enterprises to list on NASDAQ or Alternative Investment Market of London Stock Exchange in order to raise fund and claim back money from IPO and the secondary offering easier. As a matter of fact, the establishment of ChiNext brought hope of the emergence of a brand-new tailor-made capital platform for the needs of the Mainland's enterprises engaged in independent innovation and other growing venture enterprises. Although the ChiNext has already become the largest one among the ilk in Asia since its establishment in 2009 in terms of total market capitalization, as well as the number of listed companies and trading value, it is speculated and overvalued by high price-earnings ratios, high stock issuance prices and excessive fundraising of IPOs. The problems in the ChiNext show the weak supervision, non-transparency and system defects in the Mainland's financial market full of insider trading, speculation, the impairment of small shareholders' rights and interests and so forth. Therefore, the approval given by the central government for the development of Shenzhen-Hong Kong Modern Service Industry Cooperation Experimental Zone in Qianhai is a tremendous opportunity for leveraging Shenzhen-Hong Kong cooperation to jointly develop the growth enterprises market in China.

In the actual operations, the Shenzhen government can ask the SZSE to invite the HKEx to establish a sophisticated trading platform and/or sub-stock exchange in Qianhai under ‘B.O.T (build – operate – transfer)’ basis, which has been used in the infrastructure projects in Shenzhen, such as Longhua line of Shenzhen Metro. The SZSE could transfer the ChiNext trading to this new platform in Qianhai and spread its operation authorities and regulatory powers over the platform and/or sub-stock exchange to HKEx. The HKEx's rich experience and fine regulatory framework for listing companies in line with international standards could strengthen market transparency and regulatory quality in the ChiNext, enhance the standard of governance required of the listed high-tech/high growth enterprise, and evict corporate corruption and management misconduct. Shenzhen and Guangzhou still have a great number of high-tech/high-growth companies that are waiting for listing and fundraising, they do not suit to be listed on overseas financial markets. The Shenzhen – Hong Kong cooperation to develop the growth enterprises in the Mainland could generate benefits for the supervision, regulatory and legal systems in China's financial markets, and sustain steady and healthy growth. The proximity, close economic ties and sharing complementary advantages with Hong Kong support Shenzhen to have the unique and best position among China's financial centres to undertake this kind of cross-border cooperation for financial innovation in China's financial market and system.

The cooperation on collective development of private equity funds with Beijing would create a win-win situation for enhancing Hong Kong's position as the preferred city for private equity operating across Asia. Hong Kong is an import private equity fund centre in Asia for capital from all over the world to invest in the Mainland's markets and enterprises due to its role as a gateway to China, to its excellent financial infrastructure, better regulatory and legal system, developed financial market and abundance of skilled professionals. However, in the contemporary China market, the government has become the main source of funds for private equity. Since Beijing is China's political centre, private PE funds tend to move and gather in Beijing to have an easier and more frequent access to asymmetrical information from the central government organs via formal or informal networks in Beijing in order to change their investment decision and direction immediately once the central government issued or adjusted its policies. Therefore, Beijing becomes the PE fund centre in China and Asia (excluding Japan).

According to Thomson Reuters' study, in the first half of 2011, the Asian-Pacific private equity investments in China accounted US$ 6209.3 million, and Beijing shared almost 50 per cent of the market in China, within the same period the amount in Hong Kong was only US$ 44.8 million (see Table 9). This study also shows that private equity funds in Beijing exceeded those of Hong Kong. In 2009, the Beijing municipal government successively promulgated ‘Tentative Measures for the Establishment of Foreign-invested Equity Investment Fund Management Enterprises in Beijing’ and ‘Opinions on Promoting the Development of the Equity Investment Fund Industry’ to promote the development of equity investment funds in Beijing by providing convenient taxation, supporting policies on company registration, and attracting foreign financial talents. Half a year later, the ‘Tentative Measures for the Establishment of Foreign-invested Equity Investment Fund Management Enterprises in Beijing’ was promulgated in an effort to promote the development of equity investment funds. Foreign-invested equity investment fund companies can apply new investment models for business in China and obtain capital support from the Beijing government. They can also be offered the same policies as Chinese equity investment fund companies receive. In fact, many foreign PE companies in Hong Kong also have established their business and office in Beijing, and the preferential policies on private equity in Beijing are beneficial to both foreign-invested equity investment fund companies and Hong Kong-based PE companies. Hong Kong's government should strive for further liberalization measures and policies under the Closer Economic Partnership Agreement (CEPA) from the central government for the thresholds of market entry into the Beijing's PE market as the same treatments and standards applied to domestic PE companies. Zhongguancun of Beijing, known as China's Silicon Valley, has more than 20,000 high-tech companies (Yu 2011), but only about 400 of them had completed reorganization and institutionalization according to the listing requirements of SSE or SZSE, and just about 21 companies were listed on the ChiNext market through IPOs by the end of 2010 (Zhang 2010). PE companies usually claim money back from the investment after earning satisfactory benefits. IPO is the major exit route for claims of funds according to the current common practice in China. Therefore, Beijing has a lot of potential customers for PE enterprises. Hong Kong's PE industries with their unique advantages can help promote the development of Beijing's PE market. If the threshold of market entry for Hong Kong-based PE companies into the Beijing's market could be lower than that of direct investment foreign PE companies, it could attract more foreign PE firms leveraging Hong Kong as gateway into the China's PE market. Hong Kong will endeavour to meet the overall development needs of the country and achieve a win-win situation, and contribute to the development and cooperation of the financial centres in China.

Table 9

Asia Pacific (excluding Japan) private equity investments in the first half of 2011

|

Company Nation |

No. of Deals |

No. of Companies |

No. of Firms |

Sum Invested (UD$ mil) |

|

China |

164 |

164 |

128 |

6,209.3 |

|

India |

112 |

109 |

95 |

1,501.7 |

|

South Korea |

39 |

36 |

21 |

1,262.1 |

|

Indonesia |

2 |

2 |

2 |

269.7 |

|

Vietnam |

4 |

4 |

4 |

103.4 |

|

Philippines |

2 |

2 |

2 |

52.4 |

|

Hong Kong |

7 |

7 |

18 |

44.8 |

|

Singapore |

7 |

7 |

2 |

15.9 |

|

Malaysia |

2 |

2 |

3 |

1.8 |

|

Taiwan |

2 |

2 |

16 |

1.0 |

|

|

|

|

|

|

|

Total |