Late Capitalism and Neo-Liberalism – A Global Perspective on the Current Phase of the Long Wave of Capitalist Development

Journal: Journal of Globalization Studies. Volume 4, Number 1 / May 2013

The world is plunging into the second great depression of its modern history. The financial crisis provoked by the subprime market ignited a global recession in 2009 and then a new recession emerged in 2012 in Europe. Through this process, a major recomposition of the social regime of accumulation is under way.

Although the concept of ‘crisis’ is certainly confused, three different meanings use to be attached to it: a periodical crisis, a regulation crisis and a systemic crisis. The current period can be described by a regulation crisis, but it is also a systemic crisis. The present paper discusses the current phase of the long wave in late capitalism.

Keywords: crises, Kondratieff waves, late capitalism, accumulation, financial capital.

The Long Time of Capital

The concept of regulation crisis has been discussed for a while as part of a vision of self-structuring and balancing capitalism. Instead, we refer to the concept proposed by Pierre Dockès and Bernard Rosier (1983), namely that of a neoliberal ‘productive order’, considering that capitalism periodically refines its mode of functioning in order to respond to its contradictions. Indeed, capitalism is based upon a social mechanism of exploitation and accumulation of capital, but its mode of functioning evolves through time.

This understanding was the basis for Kondratieff's theory of long cycles of the conjuncture (Kondratieff 1992, 1998), as they were named in his time, or long waves of capitalist development as they were named thereafter. The concept of ‘cycles’ allowed for a wrong idea of automaticity and repetition that is rejected by historical evidence.

An adversary of Nikolay Kondratieff, Leon Trotsky, shared this view of an undulatory process in economic accumulation. In the article published in 1923, he stated that

We observe in history that homogeneous cycles are grouped in a series. Entire epochs of capitalist development exist when a number of cycles is characterized by sharply delineated booms and weak, shortlived crises. As a result we have a sharply rising movement of the basic curve of capitalist development. There are epochs of stagnation when this curve, while passing through partial cyclical oscillations, remains on approximately the same level for decades. And finally, during certain historical periods the basic curve, while passing as always through cyclical oscillations, dips downward as a whole, signalling the decline of productive forces (Trotsky n.d. [1923]).

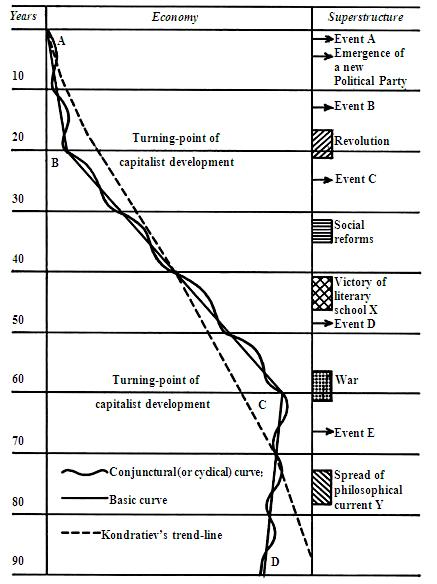

The scheme here reproduced illustrated his vision of such cycles.

Graph 1. The curve of capitalist development (Trotsky 1923)

The investigation on these long periods of capitalism attracted the attention of very different researchers, such as Joseph Schumpeter, Ragnar Frisch and Jan Tinbergen, and was taken up by Ernest Mandel (1985, 1995), Richard Goodwin and Christopher Freeman, among others.1 For these researchers, the distinction between the upturn and the downturn is crucial and no mechanism can assure the transition from a period dominated by a recession and a new period of upsurge.

Therefore, there is no symmetry between both turning points: whereas for the exhaustion of a long period of expansion the economic factors dominate, for the recovery after a long period of depression other factors are necessary. Freeman and his collaborators (Freeman and Louçã 2002) insisted on the importance of the socio-institutional framework as a key for the mismatch between the available techno-economic paradigm and social conditions for its development. And Ernest Mandel considered the political and social relationships as part of the new wave's determination. For him, endogenous economic factors were decisive for the exhaustion of the upsurge and exogenous political factors for the emergence of new upsurge after decades of downturn.

According to this view, the evolution of post-war capitalism can be described according to two waves. The first is from the end of the Second World War until the crisis of the 1970s and the turning point of the early 1980s. It has been called the Thirty Golden Years, or the Fordist epoch. Its coherence was certainly different from that of the second wave in the next period, from the 1980s until nowadays, the neoliberal epoch.

Each of these epochs can be described according to four main dimensions: accumulation regime, technological paradigm, social regulation and international division of labour.

1) The accumulation regime describes how production and realization are combined. From the point of view of production, growth and therefore accumulation are as intensive as gains in productivity allow for it. From the point of view of realization, either it is facilitated by mass consumption, given the level of wages, or it is blocked if we have an unequal distribution of wealth limiting the growth of demand. Consequently, the notion of accumulation regime also refers to the rules of the game, concerning the structure of the ruling class itself, namely the relations among industrial and banking capital and firms, or between shareholders and managers.

2) The technological or techno-economic paradigm describes the relations between the mode of production and the available techniques: in each period, a constellation of innovations is available to be diffused in the economy, following the lead of a key-factor and a dominant new branch, such as the automobile in the past or the information and communications products afterwards. But the availability of technical innovations is not sufficient, and the mismatch between this paradigm and the social regulation framework may block the process of accumulation.

Let us concentrate first on the potentialities of major innovations' diffusion. As history shows, their demonstration effect was so powerful in the case of Arkwright's water-frame that it urged some of his rivals and competitors to physical destruction of his equipment. Despite this hostility, success and high profitability of Cromford Mill and his other factories stimulated numerous imitators to invest in cotton mills, especially at the expiration of his disputed patents. Some of the early canal investments, such as the Worsley-Manchester Canal, made large profits. On a far greater scale, the Rainhill Trials of various steam locomotives followed by the successful and profitable operation of the Liverpool-Manchester Railway led to an enormous boom in railway investment and indeed to a huge financial bubble based on the excitement caused by often exaggerated estimates of the potential profits to be made. Railway promoters, such as George Hudson in Britain and the Vanderbilts in the United States, also made huge profits from speculation and financial manipulation. The profits of Carnegie, Krupp and Ford provided examples of the vast amounts that could be accumulated by successful innovative entrepreneurship. The profits of IBM and those of Microsoft, or Apple, were hugely impressive, since they became the most profitable firms in the world.

A distinguishing recurrent characteristic of the long waves is that in each case, although the individual innovations were unique and very different, a cluster of innovations emerged which offered the clear-cut potential for immense profits based on proven technical superiority over previous modes of production. Minor incremental improvements, of course, occurred all the time but the innovations, which were at the heart of each wave we have analyzed, offered quite dramatic changes in productivity and profitability. However, these highly profitable innovations were not isolated events but part of a constellation of interrelated product, process and organizational innovations. Sometimes it was a new process, which generated the main super-profits, sometimes it was an array of new products, sometimes it was mainly organizational changes, as in the case of Ford's assembly line or the Internet, but in all cases there were interdependent developments, both technically and economically. The Kondratieff wave generated after the end of the Great Depression and the Second World War was the age of oil, automobiles, motorization and mass production, under the impulse of radical innovations but also of major social changes. The nature of social regulation is crucial for the mode of development of modern capitalism.

3) Social regulation involves the determination of wage, organization of work, labour laws and the norms of social action of the State as it concerns social security, public services and other parts of indirect wage. This is a major component of the social order's construction and the creation of legitimacy, but, during periods of contraction, social regulation tends to be out of the phase with the process of capital accumulation, which demands major transformations in the social distribution of value.

In fact, during such periods of downturn of the long wave, crises of adjustment are generated by the mismatch between the potentialities of the new techno-economic paradigm and the social regulation framework, namely the condition of work and payment, of professional education and other social norms, the contracts, traditions and social culture.

In some cases, history shows that the expansionary impetus from the new may be so great that it imparts an upward thrust to aggregate industrial production and/or GDP despite a structural crisis of adaptation and high levels of structural unemployment. This was apparently the case in Britain in the 1830s and 1840s and in the United States in the 1880s and in the 1920s. On the other hand, the tempestuous growth of the automobile and oil industries in the 1920s was not sufficient to overcome the depressive trends in the USAand the world economy in the 1930s, exacerbated as they were by severe political crises, international conflicts and monetary crises. The possibility of a contemporary second great contraction evokes this example.

In any case, recurrent high levels of structural unemployment are always a manifestation of these adjustment crises in each long wave. The statistics for the nineteenth century are very poor, but there is strong evidence of very serious unemployment in the 1830s and 1840s in Britain, while there was also widespread unemployment in most industrial countries in the 1880s and especially in those which were most advanced in the use of machinery. There is, of course, abundant statistical evidence of the heavy structural unemployment in the 1920s and 1930s and again in the 1980s and 1990s until nowadays, when the unemployment is reaching unthinkable levels. Even in the 1920s boom in the United States, there were sectors experiencing severe adjustment problems, such as coal, railways and ship-building. In Germany and Britain, heavy industry in general, but especially the steel industry and the ship-building industry, experienced prolonged problems of structural adjustment. In the 1980s, the automobile industry, the oil industry, the synthetic materials industry and again the steel industry were among the many industries which experienced severe adjustment problems.

It is quite obvious that such extensive changes as mechanization, electrification, motorization, and computerization with each successive crisis of structural adjustment have led to a variety of conflicts.

The depth of social contradictions, which may be exacerbated during a structural crisis, is illustrated no less clearly by the labor conflicts which are engendered.

4) Finally, the international division of labor corresponds to the organization of the world economy and defines insertion of each country in the global market, as well as its relations with other economies. This refers to different problems, namely who extracts raw materials, who produces the industrial goods and the more sophisticated services, who dominates the channels of communication and the information technologies. But it also involves money and exchange markets, namely the definition of the world reserve currency and the control of investment and international financial flows. This defines a hierarchy of powers according to financial, military and political relationships.

Changes in the regulatory regime, whether at national level or international level, can raise the most fundamental political and ideological conflicts within and between nations. These were the cases of the conflicts over the Corn Laws in the 1830s and 1840s in Britain and the later conflict on Tariff Reform in Britain in the late nineteenth and early twentieth centuries. The problems of tariff protection also had profound effects in the United States, Germany and Japan as they industrialized and caught up in technology. Fundamental national interests are often felt to be at stake and friction over trade issues can be a major source of conflict at the international stage more generally, as illustrated in the Anglo-German naval armaments race before 1914, as well as in the current emergence of the neo-mercantilist policy of the German government in the framework of the European Union.

Table 1 summarizes our view of the contemporary transformations according to these four criteria.

Table 1

Fordism and neoliberalism

|

|

Fordist Capitalism Upswing to the long wave 1945–1975 |

Neoliberal Capitalism Downswing of the long wave 1980–… |

|

Accumulation regime |

Fordism |

Financiarization |

|

Techno-economic paradigm |

Taylorism |

Information Technology |

|

Social regulation |

Social contract |

Flexibility |

|

International division of labour |

Internationalization |

Globalization |

The Curves of Contemporary Capitalism

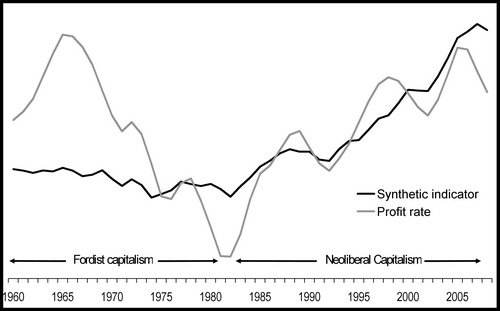

Now we recur to a method one could call ‘spectographic’, consisting in defining the long periods through a battery of indicators2 from which we extract a synthetic indicator as a simple arithmetic mean. This indicator closely follows that of the profit rate (Graph 1).

Until about the middle of the 1980s, this indicator is flat, illustrating the regulatory power of the regime. But the profit rate is descending3 since 1967 in the USA, then in all large capitalist economies from the general recessions of 1974–1975 and 1980–1982. This was the time for the major turning point of the 1980s, reestablishing the profit rate, in spite of the large fluctuations corresponding to the 1991–1993 and 2000–2002 recessions.

With this restoration of the profit rate, the synthetic indicator shows an important recovery and an almost exponential growth, which highlight the occurrence of large transformations of the structure of capitalism.

Graph 2. Synthetic indicator and profit rate

Note: see Appendix for statistical sources.

Before discussing the components of this synthetic indicator, we shall examine the evolution of productivity, since it is an essential feature of the capitalism dynamics: as the Graph indicates, during the Fordist period, productivity and the profit rate follow the same trajectory, since productivity is the root of profit. The exhaustion of the productivity's gains is the reason for the decline of a productive order and namely of the crisis of Fordism.

A second conclusion is that the profit rate growth is reestablished since the advent of the neoliberal period, in spite of the modest gains of productivity as compared to those of the Fordist period. This simply indicates that the creation of profit establishes other ways and tools.

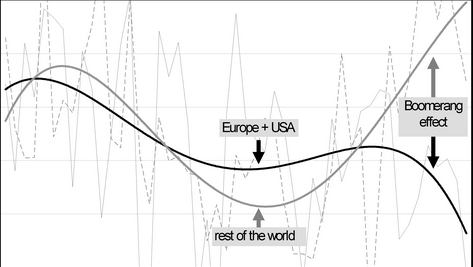

A third conclusion from this evidence is the ‘boomerang effect’ of globalization: in the USA and Europe the productivity gain declines but in the emergent economies, which are now the centers of the dynamic of capitalism it rockets.

Graph 3. Growth rate of per capita GDP (1960–2008)

Note: In %, trend in dark colour. Source: see Ameco and Maddison in the Appendix.

Repartition of Value and Realization

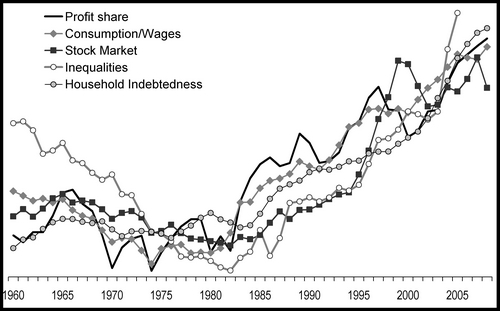

The departing point of the understanding of this evidence is the division between the shares of labour and capital. Given that the productivity gains are not comparable to those of the Fordist period, the essential tool to sustain the profit rate is lowering the share of labour, or to increase the exploitation rate. This is what happens since the 1980s, as Graph 4 proves.

Graph 4. Distribution of income

Source: Listed in the Appendix.

But if this is the mode of reestablishing the profit rate we face the traditional problem of realization: who shall buy the goods if demand is restrained by the relative decrease of wages? This is certainly also a Keynesian interrogation, but evidently not restricted to Keynesianism: the contradiction between demand and realization is an essential feature of the capitalist mode of production. For neoliberal capitalism, the answer was debt, increasing consumption through credit, as shown in Graph 4.

The growth of financial revenues (the stock market indicator in Graph 4) corresponds to the growth of inequality (see also Graph 4). These curves follow the same path.

The World Economy

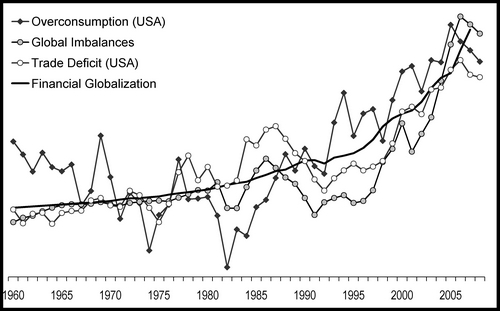

The second root of the neoliberal model is the growth of credit and debt of many economies, including that of the USA. Between 1980 and 2002, the U.S. GDP represented about 21 per cent of the world GDP. Then, it was reduced to 19 per cent in 2007, to the benefit of the emerging economies. The USA model has been based on domestic overconsumption generating a growing external deficit. The household saving rate tended to zero. This is shown in Graph 5, and the parallel between the deficit and overconsumption is telling. Therefore, the requirement of capital to finance the USA deficit became a major factor of international difficulties, not least what Larry Summers called the ‘balance of financial terror’.

Graph 5. Configuration of the world economy

Source: Listed in the Appendix.

In this framework, finance played a crucial role for the reproduction of the neoliberal model for the last three decades. Indeed, the role of finance was to allow for the transfer of value and capital and to construct the coherence of the model. But its contradictions mounted, although it was not the public deficit of the USA but the subprime market that ignited the financial meltdown: this led to the explosion of ‘fictitious capital’, as Marx named it, given that the financial titles are in fact rights to access the future distribution of surplus value. The crisis is therefore imposed when these claims are devaluated, since their dimension is disproportionate to the surplus effectively generated in the economy. As a consequence, this is not a simple financial crisis but, rather, a systemic crisis of the neoliberal order.

Furthermore, as the neoliberal model developed generating a mountain of debt, this devaluation creates a new tension. As banks are saved by massive injections of liquidity and the nationalization of private debt, the austerity plans require the people to pay for the potential losses of finance. Austerity is violence applied in order to impose the rights of access to future surpluses the Capital does not accept to renounce to.

Nevertheless, this implies a blockage of the system given its unstable foundations. Three contradictions demonstrate such instability.

The first is repartition: the margin rate, that is the part of profits in value added, peaked at its pre-crisis level in the USA while in Europe its recovery is under way. This was made possible by the gains in productivity and essentially by the freezing of wages. Yet, the repression of consumption implies a jobless recovery. This is why a new recession is on the horizon, threatening the profit rate again.

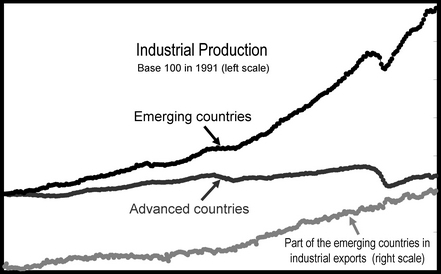

The second is globalization: as a recent UN report states, ‘the global recovery has been dragged down by the developed economies’ (UN/DESA 2011). Indeed, it is up to the emergent economies to propel the dynamics of capitalism, as shown by Graph 6. For the last two decades (1991–2011) industrial production augmented 24 per cent in the advanced countries. For the same period, its growth was 2.4 times in the emerging countries and their part in world exports is now 51 per cent. There is no precedent in the history of capitalism and this implies further contradictions and major changes.

Graph 6. Emerging economies

Sources: CPB, Centraal Planbureau, World trade monitor. URL: http://www.cpb.nl/en/data.

Finally, the budgetary policy:the correction of the deficits requires a reduction of the public expenses that creates new recessive pressures and further contraction of demand. This contradiction is accentuated by the sovereign debt crisis. The rejection, by the German government, of the proposal to mutualize the public debts through an emission of eurobonds and a decisive monetary intervention of the European Central Bank as the lender in the last resort, proves that the European Union is not ready to solve its institutional problems and to dare to exclude the financing of public debt from the speculative markets. Therefore, the euro remains under threat and defaults are still possible.

These contradictions highlight a ‘chaotic regulation’ as part of the difficulty to readdress the social regulation required by recovery towards a new wave of growth and accumulation. Our conclusion, as far as the theory of the long waves of capitalist development is concerned, is that we live through the perturbations of a major social change that neoliberal struggles do impose. The convergence of the debt crisis, the major budgetary restrictions and demand contraction, with the threat of a new recession in Europe, the transformation of the laws ruling the labour market, the lowering of the wages and pensions, provide an explosive framework. This is a systemic crisis not just because of its inner dynamics, but also because of what is at stake with the dominant strategies.

For the thirty years after the Second World War, a regulated capitalism was based upon mass consumption augmented by the wage increases. Afterwards, in the three decades of deregulated capitalism in the neoliberal mould, demand was fuelled by debt. Nowadays, neither wages nor debt: demand is restricted. Capitalism, in the period of the transition between two Kondratieff long waves, is therefore radical: social regression is offered to the majority of the population as the only hope for the future.

Notes

1 For a panorama see Louçã 1999; Freeman and Louçã 2002.

2 The precise definitions are given in the Appendix. All series are standardized and the variables are center-reduced, that is each value is taken as the deviation from the average and divided by the standard deviation.

3 Profit rate is computed for the four main typically capitalist economies: the USA, Germany, France and the United Kingdom (see Appendix).

References

Dockès, P., and Rosier, B.

1983. Rythmes économiques. Crises et changement social, une perspective historique. Paris: La Découverte/Maspéro.

Freeman, C., and Louçã, F.

2002. As Time Goes by – From the Industrial Revolution to the Information Revolution. Oxford: Oxford University Press.

Kondratieff, N. D.

1992. Les Grands Cycles de la Conjoncture. Paris: Economica.

Kondratiev, N. D.

1998. The Works of Nikolai D. Kondratieff. London: Pickering and Chatto.

Louçã, F.

1999. Ernest Mandel and the Pulsation of History. In Achcar, G. (ed.), The Legacy of Ernest Mandel. London: Verso. URL: http://digamo.free.fr/loucapul.pdf.

Mandel, E.

1985. Partially Independent Variables and Internal Logic in Classical Marxist Economic Analysis. Social Sciences Information 14(3). URL: http://gesd.free.fr/mandel85.pdf.

1995. Long Waves of Capitalist Development. A Marxist Interpretation. London: Verso.

Trotsky,L.

n.d. [1923]. The Curve of Capitalist Development. URL: http://gesd.free.fr/ curvecap.pdf.

1923. On the Curve of Capitalist Development. Viestnik sotsialisticheskoy akademii 4. In Russian (Троцкий Л. Д. О кривой капиталистического развития. ВестникСоциалистическойакадемии 4).

UN/DESA

2011. WorldEconomicSituationandProspects 2011. URL: http://tinyurl.com/wesp11.

Appendix

Statistical Sources

Ameco. European Commission database. URL: http://tinyurl.com/AMECO11.

Maddison, A. Statistics on World Population, GDP and Per Capita GDP, 2008. URL: http://gesd.free.fr/amaddi.xls.

Consumption/Wages: ratio of private consumption/wages, USA + European Union at 15. Source: Ameco. URL: http://tinyurl.com/AMECO11.

Debt USA: debt of families USA. Source: Federal Reserve, Flow of Funds. URL: http://tinyurl.com/FlowFund.

Financial globalization: ratio of the external claims to the world GDP. Source: Bichler, S., and Nitzan, J. (2010), Imperialism and Financialism. A Story of a Nexus. September. URL: http://bnarchives.yorku.ca/294/.

Inequalities: part of the richest 1 % (8 countries). Source: Atkinson, A., Piketty, T., and Saez E., Top Incomes in The Long Run of History. NBER Working Paper 15408. October 2009. URL: http://gesd.free.fr/aps2009.xls.

Overconsumption USA: propension to consume of families. Source: Bureau of Economic Analysis.

Profit share: part of profits in the value added (4 countries: the USA, Germany, France, the UK). Source: Ameco. URL: http://tinyurl.com/AMECO11.

Profit rate: average of 4 countries (the USA, Germany, France, the UK). Source: Husson, M. 2010. The Debate on the Rate of Profit. International Viewpoint 426, July. URL: http://hussonet.free.fr/debaproe.pdf.

Stock Market: Dow Jones deflated by the implicit price of the USA GDP, http://www.djaverages.com/.

Synthetic indicator: arithmetic average of the other indicators.

USA Deficit: Trade deficit as % of GDP. Source: Bureau of Economic Analysis.