Shale Gas: An Energy Miracle or a Climate Disaster?

Journal: Journal of Globalization Studies. Volume 5, Number 2 / November 2014

In recent years one has witnessed an increasing interest in the shale gas issue with the greatest level of concern at different levels of society, up to the political ones. The present article analyzes data on the shale gas resources, both worldwide and in certain regions. The authors assess the possibilities of shale gas production and prospects of its use to substitute other types of energy. They also present the model of atmosphere and climate change due to emissions from additional unconventional gas production and combustion. It is shown, that to maintain stable climatic system, the production of abundant unconventional gas resources should be accompanied by the equivalent reduction of coal use.

Keywords: unconventional gas resources, world production, atmospheric emissions, climate change.

Introduction

The first decades of the twenty-first century were marked by several striking events in mass and energy interactions within the ‘man – environment’ system:

1) for the first time after the oil shock of the 1970s the world energy consumption increased with a rather high annual mean rate of 2.6 per cent (in previous decades it was 1.9 and 1.3 per cent respectively) (BP 2014);

2) for the first time since 1965, coal has regained the leading position in the global fuel mix (5.33 billion tons of coal equivalent (btce) in 2011), terminating a fifty-year era of oil (oil consumption in 2011 was at 5.25 btce) (Ibid.);

3) for the first time in the two-centuries industrial history, the energy consumption in developing countries surpassed the level of developed economies starting from 2008 (Ibid.);

4) for the first time the annual anthropogenic carbon dioxide emission is close to the critical value of 10 Gt (Giga=billion tons) of carbon (Ibid.);

5) the annual average CO2 concentration has reached the level of 400 ppm (parts per million), which is an unprecedented amount in the last three million years (Tans and Keeling 2014; Pagani et al. 2010; Fedorov et al. 2013);

6) the global average surface air temperature increase starting from the pre-industrial period has come close to one degree Celsius (Jones et al. 2014), that is unprecedented through the late Holocene (last 6,000 years).

These facts remind that modern society faces the following new great challenges:

1) Are there enough natural resources on the Earth for the rapidly developing world economy?

2) Will the uncontrolled increase of anthropogenic burden on the climate system lead to fatal consequences for civilization?

However, to conduct an adequate analysis of the present global trends one cannot ignore some positive signs of the last decade:

1) the renewable energy sources with virtually zero CO2 emissions demonstrate the maximum growth rate among all available types of fuel (in 2000–2009 by 12 per cent per year, and the last three years by 18 per cent annually) (BP 2014);

2) for the first time in the past three decades a slightly negative trend of global air temperature is recorded (Jones et al. 2014).

In the early twenty-first century, probably the most significant event in the world energy industry was the wide use of a new fuel type (shale gas) in the United States (EIA 2013a). In just a few years (2007–2012), the production of this unconventional gas reached 270 billion m3 there, which allowed the country to reduce its huge gas imports, which has quite recently been the largest in the world. Despite the fact that today the extensive recovery of shale gas takes place only in the United States and Canada, many other countries have shown interest in use of this new unconventional fuel type. The peculiarity of shale gas consists in its quite a uniform distribution over the world; thus, many countries currently importing energy resources (e.g., China, Poland, Ukraine, and Turkey) can hope to attain higher energy and in some cases even political independence. A notable feature of recent years is the so-called ‘shale gas euphoria’ which is typical, however, mostly of the governmental authorities, political, and business circles. Unfortunately, the discussions concerning the environmental problems related to shale gas production practically always imply only such regional aspects as allocation of large territories and soil and water pollution. However, shale gas, as well as other unconventional gas sources (first of all, coal-bed methane and tight gas), represents a huge reservoir of carbon which, if released into the atmosphere, can produce significant changes in the global carbon balance and lead to large transformations of the climate system. According to recent estimates (Mohr and Evans 2011), these processes may substantially affect global primary energy mix. In its turn, the changes in the amount and structure of the world energy consumption will have a profound influence on atmosphere and climate on a global scale. In this study we analyze global resource and environmental problems connected with increasing production of unconventional gas.

Unconventional Gas Resources

Shale gas falls under the category of so-called unconventional gas sources (Perlova 2010). According to geological indications, this category encompasses gas deposits which are held by absorption, or dissolved in water, or contained in low-permeable and deep-seated collectors. If the technology for commercial production of gas is not developed, such gas relates to unconventional gases according to technological or otherwise economic criteria if the production cost exceeds the market price. The worldwide resources of gas from unconventional sources are huge and amount to more than 4000 trillion m3, which is at least by an order of magnitude larger than the resources of natural gas. Table 1 shows the distribution of these resources according to the type of gas. One should emphasize that the data presented in Table 1 refer rather to geological resources, while technically recoverable resources may be considerably smaller and will probably change over time as additional information becomes available.

Table 1

World unconventional gas resources estimates

| sources | Resources, trillion m3 |

| Gas hydrates | 2500–21000 |

| Coal-bed methane | 200–250 |

| Gas in deep occurrences | 200–350 |

| Tight gas | 180–220 |

| Shale gas | 380–420 |

Source: Perlova 2010.

Gas hydrates, that is gas in frozen state in ice, account for the major part of unconventional gas sources. As we see in Table 1, the worldwide resources of methane hydrates are very large although they have been estimated rather approximately and thus may vary within an order of magnitude.

Russia, a country with a considerable part of its territory located in the permafrost zone, has favorable conditions for the availability of essential resources of gas hydrates, which was pointed out by the Soviet specialists already in the 1940s (Solovjev 2003). In the 1960s, the first deposits of gas hydrates were discovered in the northern part of the Soviet Union. The development of the Messoyakh deposit in Siberia, which started in 1969, and where attempts to extract natural gas directly from hydrates were, from the experts' view, a success for the first time (Ibid.), can serve as an example of gas production from hydrates.

According to recent assessments of Gazprom VNIIGAZ experts (Perlova 2010), the hydrate gas reserves available in Russia amount to around 400 trillion m3 and are located in the north of the European part and Siberia. Huge gas hydrate deposits are also available in the continental shelf of the Arctic Ocean seas.

Coal-bed methane comprises an essential part of unconventional sources of gas and predominantly refers to methane adsorbed into the solid matrix of coal.

The distribution of coal methane deposits around the world is presented in Table 2. The previously existed technology for extracting gas from coal beds did not allow gas to be produced in a purposeful manner and to be used for supplying gas for households and industry due to a low yield of gas from these beds. In recent years, the situation has somewhat changed due to the development (and some decrease in the cost) of techniques for horizontal drilling and multistage hydraulic bed fracturing (HBF).

Different kinds of coal contain different amounts of methane. Brown coals have low methane content, whereas anthracites have a large content of methane, the latter have essentially lower permeability. In Russia, coals from the Vorkuta and Kuznetsk coal basins are the most promising ones for producing gas. The main reserves of coal methane in Russia are concentrated in Siberia, where experimental commercial production of coal-bed gas has recently been organized in the Taldom area of the Kuznetsk coal field.

Table 2

Top ten countries with shale gas and coal-bed methane technically recoverable resources (trillion m3)

| rank | Shale gas | Coal-bed methane | ||

| Country | Resources estimate* | Country | Resources estimate** | |

| 1 | China | 31.6 | Russia | 12.6 |

| 2 | Argentina | 22.7 | China | 10.9 |

| 3 | Algeria | 20.0 | Australia | 6.7 |

| 4 | United States | 18.8 | United States | 4.5 |

| 5 | Canada | 16.2 | Canada | 3.7 |

| 6 | Mexico | 15.4 | Indonesia | 3.2 |

| 7 | Australia | 12.4 | Ukraine | 1.7 |

| 8 | South Africa | 11.0 | Kazakhstan | 1.7 |

| 9 | Russia | 8.1 | India | 1.2 |

| 10 | Brazil | 6.9 | Poland | 1.0 |

| WORLD | 207 | WORLD | 49.6 | |

* Source: EIA 2013b.

** Source: OECD/IEA 2012.

We will not dwell on the gases in low permeable collectors and deep beds, but will consider the shale gas in more detail, a fuel that has recently attracted especially keen attention not only in the economic, but also in the wide political circles of different countries.

Shale Gas Resources

Shale gas is a kind of natural gas distributed in collectors located in the shale bed layers. Individual gas reservoirs contain not large amounts of resource, but they are huge in totality, due to which special production technologies emerge.

The estimates of shale gas reserves available in different regions and countries around the world that are given in various information sources may differ considerably, which to a significant extent can be attributed to short-term and political considerations.

The most recent report prepared by the US Energy Information Administration (EIA 2013b) excluded from consideration some Middle East countries, particularly rich in traditional hydrocarbon resources. The reserves of coal methane were also not considered. According to these EIA assessments, the worldwide recoverable resources of gas (both conventional and unconventional) totaled 648 trillion m3 with shale gas accounting for 32 per cent (207 trillion m3) of them (EIA 2013b). Only high-quality formations the most promising in terms of shale gas production were taken into account in assessing the resources. The EIA experts indicate that exploratory drilling will make it possible to obtain more accurate estimates of the reserves taking into account such parameters as yield of gas from the wells and the area where production can be organized.

Thus, shale gas resources suitable for commercial production are estimated around the world (except for some Asian countries) at 207 trillion m3 (or 271 btce, which is twice as low as the conventional gas resources). However, unlike conventional natural gas, shale gas is distributed over the globe more or less uniformly, a circumstance that, of course, makes it quite attractive as a local energy resource. Its resources (in trillion m3) are estimated at 47.7 in North America, 40.5 in South America, 38.5 in Africa, and 39.8 in Asia (mainly in China). The reserves of shale gas in Europe are estimated at 17 trillion m3 (22 btce).

According to assessments of the Russian Ministry for Economic Development, the production of unconventional gas in Europe may amount to 15 billion m3/year (around 20 million tce), a figure that in itself cannot have even the smallest effect on either the gas or the more so total energy balance of the region. In this connection it is appropriate to remind that the annual gas consumption in Europe (excluding Russia) exceeds 540 billion m3, including 180 billion m3 supplied from Russia.

The EIA report (EIA 2013b) indicates that the majority of shale deposits are located in the regions that suffer from shortage of conventional sources, in particular, in China, South America, and Europe. Therefore, shale gas could comprise a considerable share in the national energy balance of only certain countries, for example, in France (the estimated reserves amount to 3.9 trillion m3), Poland (4.2 trillion m3), Ukraine (3.6 trillion m3), and South Africa (11.0 trillion m3). It is emphasized that shale gas in South Africa which is totally deprived of traditional gas resources can be used as raw material for producing liquefied gas.

The amount of gas exported from Russia might be substituted by the shale gas produced in the nearest European neighboring states, for example, in Poland and Ukraine. But to what extent is such a prospect real?

Recently, Polish specialists have essentially lowered the data on estimated recoverable resources of shale gas in the country's interior, according to the information contained in the report of the Polish Institute of Geology published in March 2012. The recoverable resources of shale gas in Poland are now estimated at 365–768 billion m3, which is significantly smaller than the EIA assessments. In view of the fact that the consumption of gas in Poland amounts to 16.6 billion m3/year and import – 11 billion m3/year (EIA 2013a), the country can (theoretically) substitute the whole amount of imported gas by domestic production for decades. At the same time, coal accounts for a considerable share of fuel used in the energy industry of Poland, which in the future should be replaced, at least partially, by more environmentally friendly natural gas. Therefore, even with an expected growth of domestic production of shale gas, Poland will probably continue to import natural gas. Thus, the production of own shale gas will hardly give more than a somewhat diversified range of sources for importing natural gas and probably decreased import from Russia.

Nonetheless, the interest in Polish gas is quite significant. By 2012, Poland had granted more than a hundred concessions for carrying out exploration works. However, approximately 60 test wells drilled in Polish shale basins did not bring encouraging results, due to which the inspiration concerning the prospects of Polish shale gas has calmed down to a considerable extent. Moreover, three out of six major US/Canadian companies involved (Exxon Mobil, Talisman and Marathon) have pulled out of Polish gas exploration. The shares of a few independent companies specializing in European shale gas have dropped during the past two years by 70 per cent. On the other hand, sixty wells is a negligibly small number for drawing up important conclusions, while at least one hundred is needed to accurately assess the potential of the country's reserves. For comparison, 13,700 boreholes have been drilled in the single largest American shale basin of Barnett. Nevertheless, in 2014 Poland plans to become the first country in Europe to start commercial, although very limited shale gas production in the western Baltic basin.

The Ukrainian State Geological Service has recently increased its assessment of shale gas resources to 12.5 trillion m3, whereas the U.S. Geological Service has reported about only 3.6 trillion m3. At present, Ukraine imports from Russia around 25 billion m3 of natural gas a year (BP 2014), which is nearly three times larger than the amount of import in Poland, but puts forward the objective to increase the shale gas production up to 13 billion m3 within the next decade. But we will see if Ukraine has enough courage to produce such amount of this commodity, which is still very expensive, technologically and environmentally unfriendly, to be able to completely get rid of the Russian gas import. Nonetheless, one should clearly understand that for Ukraine, as well as for Poland, production of own shale gas is one of the most important components in their struggle for national sovereignty, and there is no doubt that both countries will take every effort to fully implement their ambitious targets in this field.

In Russia, the Baltic, Baikal, Volga and Pechora, Transbaikal, and Olenek platforms are the main shale gas formations, and according to assessments carried out by Gazprom VNIIGAZ (Perlova 2010), the total geological resources of shale gas may amount to 6–8 trillion m3, which is fully consistent with the EIA recent estimate equal to 8.1 trillion m3 (EIA 2013b). Some authors give even more optimistic assessments (up to 20 trillion m3), which is only slightly smaller than the estimates made by the same authors for Europe and China (Ibid.). However, one should bear in mind that at present, the environmental safety and production costs rather than the resource availability are the key aspects determining possible development of this new natural resource. In this connection one should have a closer attention to the experience of the United States, who is an acknowledged pioneer in the field of shale technologies.

At present, the United States occupies the leading position not only in proven recoverable reserves but also in production of shale gas. In 2012, the production of gas in the United States totaled 681 billion m3 (Mohr and Evans 2011) with unconventional sources (coal-bed methane and shale gas) share of more than 45 per cent. The shale gas share is constantly growing which has already resulted in a significant redistribution of the world gas market between the players and a formation of surplus supply by early 2010. As a result of growing production of shale gas, the previously constructed terminals for importing liquefied gas, which remained out of service, are being refurbished for export. In our opinion, this export may soon become quite large, up to 40–50 billion m3 already before 2020, and over 160 billion m3 by 2040. No doubt, in the nearest three or four years, the United States will become a net exporter of natural gas and the world runner-up to Qatar in the liquefied natural gas export.

The current situation with production of shale gas is entirely different on the other side of the Atlantic. Although some EU countries announced their intent to produce gas from shale, the environment specialists shortly thereafter subjected these intentions to serious criticism. These specialists are of strong belief that HBF operations, which are an integral part of shale gas production technology, inflict irreparable damage to the environment. As a result, France has already rejected plans of shale gas production and placed focus on its nuclear power industry; exploration works have been suspended in Germany, Hungary, Romania, and the Czech Republic, and eventually in Bulgaria and Lithuania the HBF operations have been recently prohibited by law. Currently Poland, where it is predominantly politicians who make statements about such method of production, Ukraine, where this matter also has a serious political context, and the United Kingdom with a strong support from its government still remain among a few states in Europe intending to continue attempts to produce gas from shale.

Outside Europe and North America it is China, Argentina, Australia, and India who have the best perspectives to develop commercial unconventional gas production. China has the largest in the world shale gas resources (31 trillion m3 or over 15 per cent of the world total) and has already become the third, after the USA and Canada, country to commence its commercial production. China is planning to produce over 60 m3 of shale gas by 2020 and 90 billion m3 by 2030.The total unconventional gas production in China will reach 230 billion m3 by 2030 divided between coal-bed (115 billion m3), shale (85 billion m3), and tight gas (30 billion m3) (EIA 2013b).

In Russia even experimental production of shale gas is not carried out, which is by no means surprising in view of huge recoverable reserves of conventional natural gas with the cost of production currently 5–6 times lower than for shale gas. However, Russia is planning to produce some 50 billion m3 of unconventional gas by 2030 from coal- bed and tight formations deposits.

The Environmental Aspects of Shale Gas Development

For the further analysis, it is worthwhile to point out the specific features relating to the shale gas production technology. Already in the early nineteenth century it was known that shale rock did contain gas. However, this rock features high density and low permeability, and gas accumulates in small isolated ‘pockets’. The first commercial gas well in shale rock was drilled in the United States as far back as 1821 near Fredonia town in the New York State by William Hart, who is regarded in the United States as the ‘father of natural gas’. George P. Mitchell and Tom L. Word are the initiators of large-scale production of shale gas in the United States.

But it is only at the time of energy crisis in the 1970s that the US government assigned financial support for the development of shale deposits in search for new sources of fuel. The exploration works were carried out, during which four giant shale formations were discovered: Barnett, Haynesville, Fayetteville, and Marcellus, stretching for several tens of thousands of square kilometers and, supposedly, containing huge gas deposits. However, at that time these reserves were inaccessible, and the works on developing the relevant production technologies were suspended after petroleum prices had subsequently dropped in the 1980s.

Commercial production of shale gas became possible only after new technologies had emerged. The modern shale gas production technology implies drilling of one vertical well and a few horizontal boreholes with a length of up to two or three kilometers (Dmitrievskiy and Vysotskiy 2010). A mixture of water, sand, and chemical agents is then forced under pressure into the wells. After that, the gas collector walls are destructed under the effect of hydraulic fracturing, and the accessible gas is pumped back up to the surface. Horizontal drilling is carried out by means of innovating seismic modeling techniques 3D GEO, which involves a combined use of geological investigations and mapping with computer-aided data processing, including visualization. As in other gas deposits, gas migrates in natural manner from a high-pressure region to a low-pressure one; therefore, central to the gas production technology is setting up regions with variable pressure (Ibid.).

The theoretical background of the bed hydraulic fracturing technology was developed jointly by the members of the Academy of Sciences Sergey A. Khristianovich and Yuri P. Zheltov at the Petroleum Institute of the USSR Academy of Sciences back in 1953.

In the United States the Devon Energy Co. was the first to start a large-scale commercial production of shale gas in the Barnett Shale basin, where a horizontal well was drilled for the first time in 2002 (Dmitrievskiy and Vysotskiy 2010). The decadal experience gained from operation of wells in the Barnett Shale, Fayetteville Shale, Marcellus Shale, and Haynessville Shale formations quite definitely revealed the following problems (Ibid.):

– large bodies of water must be available near the deposits for using the bed hydraulic fracturing technology: a mixture of water (7500 t), sand, and chemicals is used for making one hydraulic fracture. As a result, significant amounts of used contaminated water are accumulated near the deposits, which are not recovered by the producers in compliance with the environmental standards;

– the experience gained from development of the Barnett Shale play shows that the life cycle of shale wells is much shorter than that of the wells of conventional natural gas;

– the formulae of substances used by shale gas producing companies for hydraulic fracturing are confidential. According to the data presented in reports prepared by environmental specialists, production of shale gas entails significant contamination of ground waters by toluene, benzene, dimethylbenzene, ethylbenzene, arsenic, and other substances. It is known that some companies use a polymer-thickened salt-acid solution, and 80–300 t of chemical agents is used for making a single hydraulic fracturing operation;

– considerable losses of methane into the atmosphere occur in shale gas production, which may lead to aggravation of the greenhouse effect;

– the production of shale gas is profitable only under the conditions of stable demand and high gas prices.

The chemical mixture used by the Halliburton Co. comprises around 1.53 per cent of the total volume of solution and includes hydrochloric acid, formaldehyde, acetic anhydride, propargyl and methyl alcohols, and ammonium chloride. The Chesapeake Energy Co. uses its own composition of chemical mixture, but its amount in the hydraulic solution is much smaller and equal to 0.5 per cent. On the whole, gas producing companies use around 85 different toxic substances for producing shale gas.

There are also other environmental problems connected with shale gas production, primarily those concerned with utilizing the spent liquid after HBF. Apart from water and sand, this liquid contains various chemical additives for achieving more efficient HBF, which entails the danger of groundwater contamination. An increased probability of micro earthquakes in the places where HBF was carried out, as well as in places where the used liquid is pumped into underground cavities, for example, for utilizing it, has been confirmed scientifically. The possibility of gas leakage into the atmosphere during the well construction and operation stages relates to more long-term and least studied problems. According to the assessments presented in Howarth et al. 2011, the leaks into the atmosphere expected during shale gas production may comprise 4–8 per cent of the total gas yield, which is about twice as much as by production of conventional gas.

The use of shale gas instead of coal makes it possible to achieve significantly smaller amount of hazardous emissions from thermal power stations into the atmosphere. Thus, it can be assumed that the use of shale gas may entail reduction of NOx emissions by a factor of two and complete elimination of SO2 emissions. However, in calculating the environmental gains it is important to take into account the amount of emissions over the entire chain of production process, and the environmental gain estimated with such an approach turns to be significantly smaller, because the leaks of methane, a gas producing an extremely strong greenhouse effect, which occur during its production and transportation, significantly amplify the total greenhouse effect. With the percentage of leaks corresponding to the upper range of existing estimates (around eight per cent of the gas yield), a power station burning shale gas becomes similar in total emissions to conventional pulverized coal-fired power stations.

Economic Aspects of Shale Gas Development

There are extremely contradictory assessments for economic indicators of the shale gas production. The Chesapeake Energy Co. is the forerunner in shale gas production in the United States, which regularly presents the main indicators of its financial activities in free access. According to the analysis of Chesapeake Energy performance indicators, the actual net cost of shale gas production in 2008 was equal to $192.6 per 1000 m3. However, some experts argue that the real costs for producing shale gas are even higher and amount to $212–283 per 1000 m3. Some specialists believe that the companies producing shale gas artificially report lower costs, than real net cost of shale gas.

But now we can state that as of early August 2012, the cost of shale gas production in the US deposits ranged between $130 and 260 per 1000 m3 and that in Canada, $140–230/1000 m3. At the same time, the consumer prices for gas in that region are at a level of around $100/1000 m3 (EIA 2013a), which nonetheless is a factor of 2.5 lower than it was before the beginning of the ‘shale revolution’ in 2008.

But there is also another point of view. The point is that shale gas may be ‘dry’ (without admixtures) and ‘wet’ (with gas condensate containing ethane or butane). This condensate is widely used in the production of plastics, and the prices for it are higher than for gas itself, and it is exactly due to gas condensate that the producing companies get additional gain in the price. Thus, selling byproduct components makes the shale gas production profitable even with low domestic prices. As regards dry gas, its production under the currently existing conditions is still unprofitable.

Nonetheless, the US Government is quite satisfied with the currently existing gas prices, because it is exactly what is badly needed for the US economy for stimulating its growth. This is why the Government actively supports the shale projects. The low interest rate for loans is a factor stimulating investments in gas wells, despite low prices for consumers. In addition, the US power companies stake serious hopes on export of gas products and production technologies as a means for achieving better profitability. In addition, the current unprecedentedly low level of domestic prices will hardly remain and will likely start growing at a stable annual rate of 3.5 per cent already this year (EIA 2013a).

Unconventional Gas and Changes in Atmosphere and Climate

Unfortunately, discussions about the environmental problems related to shale gas production almost always imply only such regional aspects as disruption to rural communities, earthquakes and ground water pollution. However, shale gas, as well as other unconventional gas sources (coal-bed methane and tight gas), contains great amounts of carbon, which can significantly change the global carbon balance and lead to substantial changes in the climate system, if released into the atmosphere. Here we evaluate the greenhouse footprint of unconventional gas production and consumption.

Table 3

Various scenarios of natural gas production

| Scenario | Resources, btce | Production peak | |||||||

| conventional | unconventional | total | |||||||

| conventional | un-conventional | total | year | btce / year | year | btce / year | year | btce / year | |

| Klimenko and Tereshin (2010a) | 490 |

| 490 | 2045 | 5.8 |

|

| 2045 | 5.8 |

| Klimenko and Tereshin (2013) | 490 | 420 | 910 | 2045 | 6 | 2075 | 5.5 | 2065 | 10.0 |

| Present study | 540* | 430* | 970 | 2045 | 5.7 | 2080 | 5.9 | 2065 | 11.1 |

* Source: EIA 2013b; OECD/IEA 2012.

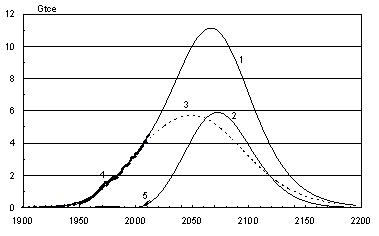

The predicted values of unconventional gas production are based on the estimates of unconventional gas resources given in Table 3, where the results of our earlier calculations (Klimenko and Tereshin 2010b) are presented for comparison purposes (note that calculations in Klimenko and Tereshin 2010b take into account only conventional gas resources). It is obvious that an introduction of unconventional gas sources would sharply increase the role played by natural gas in the world economy, and the peak of annual recovery would grow from 6 to roughly 11 billion tce and shift into the second half of the twenty-first century (Fig. 1). Even at the end of the current century, total gas production is expected to exceed contemporary values, while a complete depletion of these resources is expected only at the end of the twenty-second century. Natural gas will likely become the main component of the world energy balance as early as at the beginning of the 2030s. One can assume that by this time a mass production of unconventional gas will be developed in several countries outside North America and first of all in China, India, Australia, and Argentina.

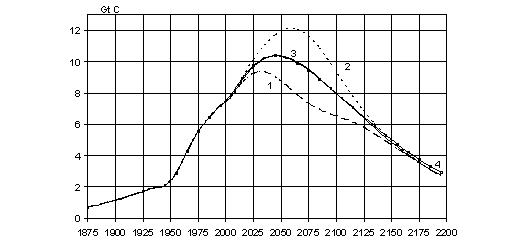

Nevertheless, from the viewpoint of possible changes in the atmospheric composition and climate, carbon dioxide emissions from combustion of both natural gas and all other fossil fuels are essential, because they depend on the total energy consumption and the world fuel mix. The results presented here are based on the genetic forecast of energy consumption (see the detailed description of the procedure in Klimenko and Tereshin 2010a, 2010b, 2013), which has proved its reliability in long-term forecasting. This method implies stabilization of the world energy consumption at the level of around 30 billion tce by the end of the current century, with the dominating role played by non-fossil sources (mostly unconventional and renewable sources (URS) – solar, wind, hydro, and bioenergy sources). Experience has shown that the long-term forecast of the energy mix represents a much more complicated problem; therefore, we will further consider two extreme scenarios and an intermediate one, namely: the whole volume of unconventional gas consumption is used to substitute either coal (Scenario 1), or URS (Scenario 2), or coal and URS in equal portions (Scenario 3).

The results of simulations presented in Fig. 2 show that the implementation of Scenario 3 would yield a path of future carbon emissions almost the same as that produced by the so-called ‘historical’ scenario whose consequences have been comprehensively discussed in our recent publications (Klimenko and Tereshin 2010a, 2010b, 2013; Khrustalev et al. 2008; Arzhanov et al. 2012) and can be characterized as causing a certain concern with the scale of upcoming climate changes. The substitution of coal with unconventional gas would lead to rapidly reaching (already in two decades) the peak of carbon emission at slightly above 9 Gt of carbon per year, while the replacement of URS causes growth of this peak almost to 12 Gt of carbon per year and shifts it to the second half of the present century.

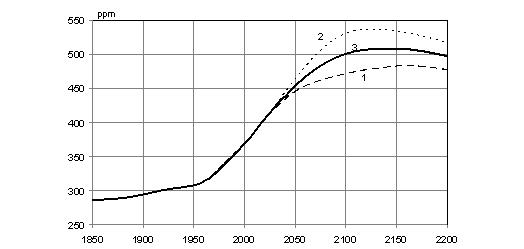

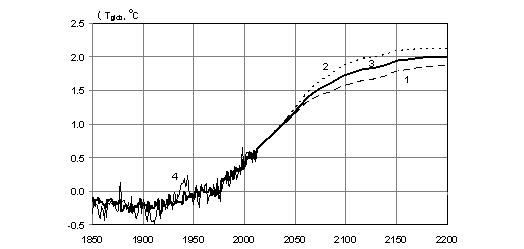

Under different scenarios of unconventional gas resources development, the changes in the global carbon cycle are significant and they are clearly seen from the variations in carbon dioxide content in the atmosphere (Fig. 3) and the temperature response of the climate system (Fig. 4). Simulation of the global variations in atmospheric CO2 content have been conducted by Dr. Olga V. Mikushina using the box-diffusion model of the carbon cycle; that of the surface air temperature, using the regression-analytical model of climate developed at the Moscow Power Engineering Institute (Klimenko et al. 1997).

As was mentioned above, the shale gas production is associated with significant methane leakage rate into the atmosphere, up to 4–8 per cent of total gas production, and this value is considerably higher than in the case of conventional natural gas production. With respect to this, some researchers claim serious concerns that the release of these amounts of methane, whose greenhouse effect is 25 times stronger than that of carbon dioxide, can intensify global warming. Based on our simulations, under the assumption that technological leakages amount to six per cent of total gas production, we argue that the maximal methane release into the atmosphere from shale gas production will be reached between 2050–2120 and will account for 100–200 million tons per year, or 10–15 per cent of the estimated total emission from all its sources. This will lead to a certain increase in the methane atmospheric content and corresponding higher radiative forcing of this gas during this period by about ten per cent as compared to the basic scenario (Klimenko and Tereshin 2010a).

However, due to the anticipated decline of unconventional gas production with the respective reduction of methane emission and owing to the comparatively short lifetime of this gas in the atmosphere (12 years), the methane concentration will eventually approach the value of the basic scenario during the twenty-second century. Finally, we estimate the contribution of the additional methane due to shale gas production to the anticipated temperature response a few hundredths of a degree Celsius. Partial substitution of coal by unconventional gas in the world energy balance will lead to a noticeable decrease in the anthropogenic impact on the climate system, shifting it down from the critical limits of 500 ppm of CO2 concentration and 2°C of temperature rise as compared to the pre-industrial epoch. However, a slow-down of URS growth rate and preservation of the current orientation to fossil fuels are very dangerous because both the carbon dioxide concentration and then the air temperature will exceed these critical limits well before the end of the current century and remain beyond them for at least two or three centuries. Under these conditions, a significant increase in the acidity of the oceanic upper layer is inevitable, and this will cause massive extinction of many marine species, first of all, corals (Knowlton 2001; Hoegh-Guldberg et al. 2007). This would mean an economic collapse of many developing countries where tourism and offshore fishery are the basic sources of income. For example, in Asia coral reefs alone provide about one-quarter of the annual total fish catch and food for about a billion people. In the Caribbean basin tourism is a major foreign currency earner and in some countries it accounts for up to a half of the gross domestic product. The long-term temperature departure above 2°C (or just 1.2°C above the current value) would almost inevitably cause a partial melting of the Greenland Ice Sheet and of all non-Antarctic glaciers with the following increase in the global sea level by at least two meters (Oppenheimer and Alley 2005; Jevrejeva et al. 2011) and local sea level rise up to three meters (Meyssignac and Cazenave 2012) and a significant weakening of the meridional overturning oceanic circulation in the North Atlantic as well. The latter will likely result in significant changes in the global distribution of surface winds, rainfall and soil moisture and could lead to a global reduction of the terrestrial vegetation net primary production by several per cent (Vellinga and Wood 2002).

Conclusions

1. There is still a substantial uncertainty concerning economical and environmental aspects of mass shale gas production which leaves room for doubts and hampers its further development. Provided present resources assessments are correct, unconventional gas and, first of all, shale gas may solve some regional energy (import substitution) and environmental (coal substitution) problems. However, unconventional gas cannot be regarded as an ‘additional’ energy source, capable to meet the growing energy demand.

2. The large-scale production of shale gas outside North America will hardly be possible in the nearest future. The pattern in which the shale gas reserves are distributed over the globe allows us to assume that it can replace to a significant extent the natural gas supplied from Russia in some European countries (Poland and Ukraine), but this is unlikely to take place until the end of the current decade. However, unconventional gas becomes increasingly important and will make up more than 50 per cent of global gas production in the second half of the current century.

3. The net cost of shale gas production is currently several times higher than that of conventional natural gas in major gas producing countries. To develop a shale gas deposit one should spend from $3 to $4 million per each well. Due to the specific features of shale gas production technology, the costs for maintaining shale gas wells in serviceable state are significantly higher than in traditional deposits.

4. The production of shale gas entails considerable emissions of methane into the atmosphere. Fortunately, this is not a dangerous factor aggravating the greenhouse effect even if the amount of leaks is close to their upper limit estimated at eight per cent of the yield. The expansion of shale gas production does not come in serious contradiction with the growing climate protection requirements. In addition, a substitution of coal by shale gas will result in twofold reduction of NOx emissions and complete elimination of SO2 emissions.

5. The shale gas problem has many aspects, of which the political aspect is undoubtedly the dominating one. As a new source of energy, shale gas is noticeably inferior to traditional natural gas not only in its consumer properties (price, environmental, and technological attractiveness), but also in the availability of resources and will not be able to seriously compete with natural gas at the global level in the nearest two to three decades. In the short term, the shale gas can become an attractive resource only at regional and local levels and only under the conditions of strong protective measures.

6. To maintain stability of the climate system, the production of abundant unconventional gas resources should be accompanied by the equivalent reduction of coal use. In this case one can view shale and other unconventional gas sources as an energy bridge over the current century yet reducing greenhouse gases emissions compared to oil and coal.

Acknowledgments

The study was supported by Ministry of Science and Education of Russia (basic and project parts), Russian National Foundation (grant No. 14-19-00765) and Russian Foundation for Basic Research (grants No. 12-08-00367, and 13-08-00872).

The authors are thankful to Dr. O. V. Mikushina for model simulations and A. O. Morozova for collecting data.

Arzhanov, M. M., Eliseev, A. V., and Klimenko V. V. et al. 2012. Estimating Climate Changes in the Northern Hemisphere in the 21st Century under Alternative Scenarios of Anthropogenic Forcing. Izvestiya, Atmospheric and Oceanic Physics 48(6): 573–584.

BP. 2014. Statistical Review of World Energy 2014. URL: http://www.bp.com/content/dam/ bp/pdf/Energy-economics/statistical-review-2014/BP-statistical-review-of-world-energy-2014-full-report.pdf.

Dmitrievskiy, A. N., and Vysotskiy, V. I. 2010. Shale Gas: A New Vector in the Development of the Worldwide Market of Hydrocarbon Raw Materials. Gas Industry 8: 44–47. In Russian (Дмитриевский, А. Н., Высотский, В. И. Сланцевый газ: Новый вектор развития мирового рынка углеводородного сырья. Газовая промышленность 8: 44–47).

EIA – Energy Information Administration. 2013a. Annual Energy Outlook 2014 with Projections to 2040. US EIA.

EIA – Energy Information Administration. 2013b. Technically Recoverable Shale Oil and Shale Gas Resources: An Assessment of 137 Shale Formations in 41 Countries outside the United States. US EIA.

Fedorov, A. V., Brierley, C. M., Lawrence, K. T. et al. 2013. Patterns and Mechanisms of Early Pliocene Warmth. Nature 496(7443): 43–49.

Hoegh-Guldberg, O., Mumby, P. J., Hooten, A. J. et al. 2007. Coral Reefs under Rapid Climate Change and Ocean Acidification. Science 318(5857): 1737–1742.

Howarth, R. W., Santoro, R., and Ingraffea, A. 2011. Methane and Greenhouse Gas Footprint of Natural Gas from Shale Formations. Climatic Change Letters 106(4): 679–690. DOI 10.1007/s10584-011-0061-5.

Jevrejeva, S., Moore, J. C., and Grinsted, A. 2011. Sea Level Projections to AD 2500 with a New Generation of Climate Change Scenarios. Global and Planetary Change 80–81(1): 14–20.

Jones, P., Harpham, C., Osborn, T. et al. 2014. Combined Land and Marine Temperature Anomalies Datasets. Climatic Research Unit. Norwich: University of East Anglia. URL: http://www.cru.uea.ac.uk/cru/data/temperature/.

Khrustalev, L. N., Klimenko, V. V., Emelyanova, L. V. et al. 2008. Dynamics of Permafrost Temperature in Southern Regions of Cryolithozone under Different Scenarios of Climate Change. Earth's Cryosphere 12(1): 3–11. In Russian (Хрусталев, Л. Н., Клименко, В. В., Емельянова, Л. В. и др. Динамика температурного поля многолетнемерзлых пород южных районов криолитозоны при различных сценариях климатических изменений. Криосфера Земли 12(1): 3–11).

Klimenko, V. V., and Tereshin, A. G. 2010a. World Power Engineering and Global Climate after the Year 2100. Thermal Engineering 57(12): 1035–1041.

Klimenko, V. V., and Tereshin, A. G. 2010b.World Energy and Climate in the Twenty-First Century in the Context of Historical Trends: Clear Constraints to the Future Growth. Journal of Globalization Studies 1(2): 27–40.

Klimenko, V. V., and Tereshin, A. G. 2013. Unconventional Gas and Transformation of the Global Carbon Balance. Doklady Earth Sciences 453(1): 1113–1116.

Klimenko, V. V., Klimenko, A. V., Andreichenko, T. N. et al. 1997. Energy, Nature, and Climate. Moscow: MEI Publishing. In Russian (Клименко, В. В., Клименко А. В., Андрейченко, Т. Н. и др. Энергия, природа, климат. Москва: Издательство МЭИ).

Knowlton, N. 2001. The Future of Coral Reefs. Proceedings of the National Academy of Sciences 98(10): 5419–5425.

Meyssignac, B., and Cazenave, A. 2012. Sea Level: A Review of Present-Day and Recent-Past Changes and Variability. Journal of Geodynamics 58: 96–109.

Mohr, S. H., and Evans, G. M. 2011. Long Term Forecasting of Natural Gas Production. Energy Policy 39(9): 5550–5560.

OECD/IEA 2012. Golden Rules for a Golden Age of Gas. World Energy Outlook. Special Report on Unconventional Gas. Paris: OECD/IEA, International Energy Agency.

Oppenheimer, M., and Alley, R. B. 2005. Ice Sheets, Global Warming, and Article 2 of the UNFCC. Climatic Change 68(3): 257–267.

Pagani, M., Liu, Z., LaRiviere, J., and Ravelo, A. C. 2010. High Earth-System Climate Sensitivity Determined from Pliocene Carbon Dioxide Concentration. Nature Geoscience 3(1): 27–30.

Perlova, E. V. 2010. Commercially Significant Nontraditional Sources of Gas: Worldwide Experience with their Development and Prospects for Russia. Territoria Neftegaz 11: 46–51. In Russian (Перлова, Е. В. Коммерчески значимые нетрадиционные источники газа: Мировой опыт освоения и перспективы для России. Территория Нефтегаз 11: 46–51).

Solovjev, V. A. 2003. Natural Gas Hydrates as Potential Mineral Resource. Russian Chemical Journal 48(3): 59–69. In Russian (Соловьев, В. А. Природные газовые гидраты как потенциальное полезное ископаемое. Российский химический журнал 48(3): 59–69).

Tans, P., and Keeling, R. 2014. Global Greenhouse Gas Reference Network. Trends in Atmospheric Carbon Dioxide. NOAA/ESRL. URL: http://www.esrl.noaa.gov/gmd/ ccgg/trends/.

Vellinga, M., and Wood, R. A. 2002. Global Climatic Impacts of a Collapse of the Atlantic Thermohaline Circulation. Climatic Change 54(3): 251–267.