Long-Wave Economic Cycles: The Contributions of Kondratieff, Kuznets, Schumpeter, Kalecki, Goodwin, Kaldor, and Minsky

Almanac: Kondratieff waves:Juglar – Kuznets – Kondratieff

Abstract

The current work highlights the empirical and epistemological contributions made by economists regarding the cyclical nature of economic and social development. We examine the main mechanisms of economic cycles involving different time scales, with a particular focus on long wave theory. Long wave theories include Kondratieff's theory of cycles in production and relative prices; Kuznets' theory of cycles arising from infrastructure investments; Schumpeter's theory of cycles due to waves of technological innovation; Keynes–Kaldor–Kalecki demand and investment oriented theories of cycles; Goodwin's theory of cyclical growth based on employment and wage share dynamics; and Minsky's financial instability hypothesis whereby capitalist economies show a genetic propensity to boom-bust cycles. The paper also discusses the methodological and empirical challenges involved in detecting long duration cycles.

Keywords: production cycles, infrastructure cycles, accelerator – multiplier mechanism, innovation cycles, Goodwin cycles, Keynes–Kaldor cycles, Samuelson accelerator-multiplier cycles, Kalecki cycles, Minsky asset price-leveraging cycles, spectral analysis, wavelet analysis.

All things come in seasons – Heraclitus

One can never step into the same river twice – Heraclitus

1. Introduction

After a thirty year period of relative tranquility in the world economy – the so-called period of ‘great moderation’ – the U.S. economy suffered a financial meltdown in 2008 that triggered the ‘great recession’. These events have motivated new interest in theories that can explain long periods of expansion that end suddenly with deep recessions. One approach, which has been intellectually unfashionable for many years, is the theory of long economic waves.

This paper examines the empirical and epistemological contributions made by economists regarding the cyclical nature of economic and social development. The paper discusses the main mechanisms of economic cycles involving different time scales, with a particular focus on long wave theory. As part of this survey, the paper shows the continuing relevance of the theoretical constructs developed by Nikolai Kondratieff (also, Kondratiev, Кондратьев) and Simon Kuznets (Кузнец), both for modern macroeconomics and for assessing possible future scenarios. The paper also shows the difficulty of modeling long wave analysis as it poses significant challenges to the equilibrium method which dominates shorter period economic analysis.

Empirical economists and economic historians have voiced diverse views on economic cycles. On the one hand, there seems to be good evidence for business cycles based on a shorter time scale, and the endogenous dynamics of shorter cycles appear to be clear and distinct. On the other hand, long wave cycles are more controversial, involve different theoretical mechanisms, and are harder to verify empirically – in part because data is inevitably more limited owing to the reduced frequency of such cycles. Several different theories of the long wave exist. These include Kondratieff's theory of cycles in production and relative prices; Kuznets' theory of cycles arising from infrastructure investments; Schumpeter's theory of cycles due to waves of technological innovation; Keynes–Kaldor–Kalecki demand and investment oriented theories of cycles; Goodwin's theory of cyclical growth based on employment and wage share dynamics; and Minsky's financial instability hypothesis whereby capitalist economies show a genetic propensity to boom-bust cycles.

Business cycles of shorter duration can be explained by inherent mechanisms that generate cyclical fluctuations in economic activity. However, the mechanical view of long waves is more problematic and challenging. We discuss both those challenges and a recently ‘discovered’ evidence regarding components of long duration cycles. The notion of a financially based long wave Minsky super-cycle, which has been largely overlooked by contemporary economist, appears to have become more relevant in the wake of the financial crisis and the end of the ‘Great Moderation’.

The paper is organized as follows. Section 2 examines the long wave theories of Kondratieff and Kuznets. Section 3 builds on the preceding discussion and analyzes varying time scales and mechanisms of economic cycles prevalent in economic theory. Section 4 examines a Minsky-type of long-period cycles. Section 5 discusses the methodological and empirical challenges involved in detecting economic cycles, particularly those of long duration. Section 6 concludes the paper.

2. The Legacy of Kondratieff and Kuznets

2.1. Kondratieff and theory of long waves

Writing in the early 1920s Nikolai Kondratieff advanced the idea of the probable existence of long wave cycles in capitalist economies lasting roughly between 48 and 60 years. Within that, there is a period of accumulation of material wealth as productive forces move to a newer, higher, level of development. But at a certain point there commences a decline in economic activity, only to re-start growing again later (Kondratieff 2004 [1922]). This mechanism has been dubbed, in economic literature, as Kondratieff cycles.

It should be noted that prior to Kondratieff, some empirical efforts on systematizing the cyclicality of economic crises was carried out by van Gelderen (1913), Buniatian (1915), and de Wolff (1924), which Kondratieff admits to in his publications (see end note in Kondratieff 1935). Though Kondratieff's ideas were not well accepted by the official Soviet economics he insisted on his main argument and in short time followed up with more rigorous publications. Only few English language translations were available at the time (most notably, Kondratieff 1935). Nevertheless, the potency of his ideas was recognized quickly entering the work of subsequent economists (e.g., Schumpeter 2007 [1934]; Kuznets 1971; Rostow 1975; and others) as we review in the next section.

The gist of Kondratieff's argument came from his empirical analysis of the macroeconomic performance of the USA, England, France, and Germany between 1790 and 1920. The economist looked at the wholesale price levels, interest rate, production and consumption of coal and pig iron, production of lead for each economy and price movements (Kondratieff 1935). Using a peculiar statistical method – de-trending the data first and then using an averaging technique of nine years to eliminate the trend as well as shorter waves of Kitchin (Kitchin 1923) type – Kondratieff suggested a regularity of ups and downs in the data on a long time scale. Within that there were intermediate waves along with long waves. As a result, Kondratieff stated that economic process was a process of continuous development. Among possible explanations to the long wave cycles Kondratieff mentions: a) changes in technology; b) wars and revolutions; c) appearance of new countries on the world map; and d) fluctuations in production of gold (Kondratieff 1935, 2002).

All four appear as valid external shocks in pushing any particular economy or the world economy into a downward or upward cycle path. However, after careful analysis it became evident that external factors could not be the sole determinants of shocks in economic transformation. The missing part is the accumulation of preceding events, and the development of economic – but also social, and political – relationships over long cycles that may help to endogenize the external factors.

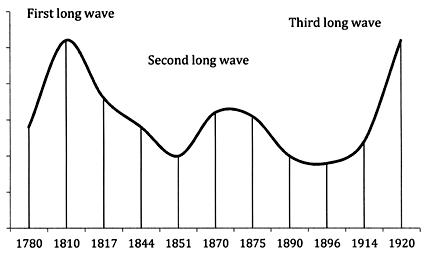

Fig. 1a illustrates an approximation of Kondratieff's original timeline of long wave cycles. Kondratieff's original estimation was based on a commodity prices index for the USA, England, and France in his work of 1935 (see Kondratieff 1935). Subsequently, with popularization of Kondratieff's views, extensions to the original analysis, roughly following the 40–60 years rule, began to appear.

Fig. 1a. Long waves cycles illustration

Source: authors' approximation based on Kondratieff (1935).

One of the first to catch on the logic was Schumpeter (1939) who pointed out the distinction between short (Kitchin cycles of 3–4 years), medium (Juglar cycles of 9–10 years),[1] and long (Kondratieff cycles of 54–60 years) cycles in his analysis of economic development. We discuss some of them below.

As to mechanisms, Kondratieff already pointed to a large-scale accumulation of innovative activity, that is inventions and processes modifications that required fifty or more years before complete insertion, absorption in the production method. The role of innovation, implied in Kondratieff's analysis, is captured by the internal dynamic tendencies described in detail in Schumpeter's The Theory of Economic Development (Schumpeter 2007 [1934]). In turn, Garvy (1943) subjects Kondratieff's proposition to sharp criticism from positions of Soviet economists and from the point of view of Western economics. Paradoxically, in either case the conclusion appears to be that Kondratieff was too hasty in assigning the term ‘cycle’ to his propositions, as those do not correspond to the internal evolutionary dynamics following some mechanism of cycles.

There was a difference however in the Western economists' views and their contemporary Soviet counterparts. From the Western economist point of view, articulated by Garvy (Ibid.), there was no sufficient statistical evidence to warrant any regularity, that is cyclicality, to Kondratieff's analysis. The Soviet economists writing around the time of Kondratieff's original publications and shortly after (e.g., Studensky, Oparin, Pervushin, Bogdanov, Sukhanov and others, see Garvy 1943 for concise discussion and references) rejected the term ‘cycle’ in reference to the capitalist production mode since that implied some type of capitalist system's perpetuity. At the time that was in direct opposition with the socialist beliefs of gradual phasing out of the capitalist economy into its next logical stage of socialism, as was implied by then dominant interpretation of Marx's Capital (2003 [1867]). These beliefs in rapid phased successions picked up from simplistic interpretations would feed into initial enthusiasm around shock therapy reforms in post-socialist economies in the early 1990s (Gevorkyan 2011).

Recently, researchers working within Kondratieff's original methodological scope have attempted to extend their analysis across the twentieth century with focus on predictive capabilities of such work into the nearest future. Some find the ongoing economic deterioration in the world economy fitting calculations of the Fifth Long Wave of the Kondratieff cycle (e.g., Korotayev and Tsirel 2010; Kondratieff 2002; Akaev 2009; and others), some of them using spectral analysis. A re-validation of the very four exogenous shocks (technology, wars, shifts in boundaries, and value of gold) so carefully documented and refuted by Kondratieff himself took place in some of those papers. Exogenous shocks are surely important ‘occurrences’, yet, the internal dynamics in the evolution of economic relationships over a long time period and staging economic development must be considered as well. We address this in further detail below, using more modern empirical methods.

2.2. Kuznets' novel analysis of development

Simon Kuznets received the Nobel Prize in Economics in 1971 for his empirical analysis of economic growth, where he identified a new era of ‘modern economic growth’. Like Kondratieff, Kuznets relied on empirical analysis and statistical data in his pioneering research. Absorbing his findings on historical development of the industrial nations with initially abstract categories of the national income decomposition, Kuznets developed a concept of long swings, though disputed, now referred to as Kuznets cycles or Kuznets swings (e.g., Korotayev and Tsirel 2010).

The Kuznets swings' period is ranged between 15–25 years and initially connected by Kuznets with demographic cycles. In that analysis, the economist observed and quantified the cyclicality of production and prices, linking with immigrant population flows and construction cycles. Researchers have attempted to connect these cycles with investments in fixed capital or infrastructure investments (see Ibid. for literature review). Focusing on developed economies of North America and Western Europe, Kuznets computed national income from late 1860 forward with structural breakdowns by industry and final products. He also provided measures of income distribution between rich and poor population groups.

Kuznets unveiled the deficiency of constrained theoretical work built on simplified assumptions. He was critical of capital and labor as the sole factors sufficient for economic growth. Instead analysis must encompass information on technology, population and labor force skills, trade, markets, and government structure. Kuznets carried his analysis further in developing measures of national income through categories of consumption, savings, and investment (e.g., Kuznets 1949, 1937, 1934, etc.), eventually leading to a system of national income accounting.

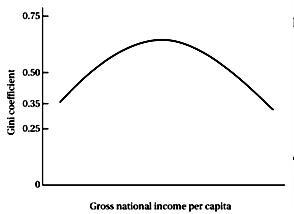

It should also be noted that while working on the problem of income inequality, Kuznets was one of the first to look at economic growth measurements in the developing world (e.g., Kuznets 1971, 1966, and 1955). His well-known inverted U-shaped curve measuring inequality on the y-axis and economic development, expressed as change in GNP on the x-axis was an intellectual breakthrough of the time (see Fig. 1b). The conclusion is that while the economy remains in agricultural stage income inequality among different groups within the economy is low. As the national economy embarks on the process of industrialization inequality rises over time, then it falls again.

Fig. 1b. Kuznets curve

This describes the experience of developed economies in Western Europe and North America, that is the initial phases of industrialization cause sharp rises in inequality. Upon reaching a critical saturation point, inequality subsides while economic growth continues. This happens through the emergence of a ‘middle class’, improved education facilities, health care, and governance. It is interesting to note that further structural change and the shifting of resources to services and the financial sector, may increase inequality again, as, for example, is seen in the U.S. economy since the 1980s. It may be argued that this somewhat correlates to a popular analysis in development economics on the transition mechanisms from traditional to modern industrial sectors.

A variant of the Kuznets curve is also utilized in the analysis of environmental problems. This application suggests an immediate deterioration in air quality and intensification of environmental problems at the initial industrializing stages until spreading affluence and emergence of middle class introduces legislative and other controls on hazardous production (WB 1992; Grossman and Krueger 1995 and more recently Stern 2004). Elsewhere, these implied predictions of fading inequality offered a strong intellectual foundation for the mentioned reforms of the early 1990s in Eastern Europe and the former Soviet Union (Gevorkyan 2011). In studies of sequencing of market liberalization reforms and limitations of the state in the economy there were omitted the negative externalities of shock therapy policies. Yet, in the early 1990s, the promise of immediate market reforms and potential access to greater income opportunities did not materialize at the height of the reforms. In fact, income inequality problems still remain relevant and critical on policymakers' agendas two decades since the ‘transition’. The absence of the universal tendency of declining income inequality raises a question of how one measures economic development and what time-frame to consider is ‘sufficient’ to measure the rise of ‘welfare’ over time.

Finally, Kuznets (1973) brings up six key characteristics of modern economic growth, based on methodology consistent with national income accounting and historical analysis of economic development: 1) increase in per capita growth and population in developed economies; 2) increasing productivity rates; 3) increasing rate of structural transformation; 4) rising urbanization and secularization; 5) spread of technology and infrastructure improvements (communications); 6) limits to wide-scale spread of economic growth and benefits. Therefore despite seeming improvements, Kuznets noted persistence of disproportionate economic growth worldwide and apparently some broader measures of welfare.

Broadly speaking, such persistence of long wave-like tendencies on a global scale, a feature of contemporary industrial and financial globalization, supports the concept of redefined fundamental uncertainty (Gevorkyan and Gevorkyan 2012). Here the uncertainty of the direction, length, and capability of the post-great recession's potential recovery remains unclear. The lesser-developed economies (aka emerging markets) are worst affected in such circumstances, as the speculative foreign capital exits and industrial capacity remains inadequate on global competitive scale with absent technological advance.

Common between the work of both Kondratieff and Kuznets was the motivation to define the mechanisms of economic growth and development, and systematize core tendencies driving the transformational momentum. That in turn connects directly to the earlier discussion on cyclicality in development.

3. Time Scales and Mechanisms of Economic Cycles

As mentioned, the work of Kondratieff and Kuznets fostered a systematic approach to modern understanding of long economic swings. Numerous authors have further proposed not only different mechanisms underlying cycles but also cycles on different time scales. An early theory of cycles was put forward by Robert Owen in 1817, who stressed wealth inequality and poverty, originating in industrialization, yielding under-consumption as a reason for economic crises. Sismondi, in the middle of the 19th century took a similar view and developed a theory of periodic crises due to under-consumption. This led to the discussion of the ‘general glut’ theory of the 19th century, which Marx and other classical economists also extensively contributed to.

More specifically, a mechanism of cycles on a shorter times scale, of 8–10 years duration, was developed by Juglar (Juglar cycles), resulting, as he saw it, from the waves in fixed investment. Later, Kitchin, in the 1920s, introduced an inventory cycle of 3–5 years. Later an important contribution was made by Schumpeter (1939), who referred to the ‘bunching’ of innovations and their diffusion as a cause for long waves in economic activity.

Roughly at the same time, Samuelson (1939), influenced by the Spiethof accelerator and the Keynesian multiplier principle, developed the first mathematically-oriented cycle theory using difference equations.[2] Others, such as Rostow (1975), had proposed the theory of stages of growth. Simultaneous with Samuelson, Kalecki (1937) developed his theory of investment implementation cycles where he saw significant delays between investment decisions and investment implementations, formally introducing differential delay systems as tool for studying cycles.

Kaldor (1940), rooted in Keynesian theory, developed his famous nonlinear investment-saving cycles, which took into account aggregate demand. Later, Goodwin (1967) proposed a model of growth cycles, which took into account classical growth theory, but was based on unemployment-wage share dynamics, since the overall growth rate, as well as productivity growth, are kept constant in the long run. We will first discuss cycle theories on a longer time scale and then move to the Goodwin and Keynes-Kaldor cycles. We also briefly include a discussion of Kalecki's cycle theory (1971) and how it might relate to Kondratieff.

3.1. The Kondratieff long swings

The above review raises a few critical questions that need proper evaluation. For example, it is difficult to detect clear mechanisms in the Kondratieff cycles (e.g., as sketched in Fig. 1a above). If anything is working here as a mechanism, it must be some exhaustion of endogenous and exogenous factors: in the long upswing prices are rising, interest rates rise and wages rise, raw materials and non-renewable resources may be exhausted, causing to drive up prices and wages. New technologies are discovered in periods of long down swings, which come to be used in a new upswing. New resources are discovered, such as iron ore, coal, gold and other metals, which Kondratieff argues to be endogenously expanded through new discoveries but both technology and resources will finally be exhausted too: resource and product prices rise, deposits at saving banks rise, but also interest rates and wages rise and a downturn begins. There is a struggle for markets and resources. New countries are opened up. There are market limits, such export limits, which restrict further expansions, as Kondratieff data on French exports show. Then, in the long downswing, prices fall, wages fall, interest rates fall, plenty of resources and unused production capacity push prices down, and unemployment reduces wages. Overall, there are some mechanisms indicated in Kondratieff, but not specifically modeled.

3.2. The Kuznets long swings

Further, Kuznets theory of development and fluctuations can be seen as an interesting intersection of two traditions in the economics of his time. On the one hand, he was interested in cyclical movements in numerous time series data, such as volume of all types of production and prices, seasonal and secular movements in industry income and national income and its components, long swings in economic activities, and business cycle analysis. On the other hand, he saw development as a time irreversible process of industry and national income development, which evolves in stages of economic growth, with plenty of structural changes. Each stage may have its particular saving rate, consumption patterns, unevenness and disequilibrium as well as income inequality. As described above, inequality first rises with industrialization and later declines. Kuznets conceptual framework can be seen as a mixture of cycle theories, referring to the accelerator principle for infrastructure investments, and a theory of stages of economic growth that were similar to those pursued by Rostow (1975). A similar view on stages of growth, that taken by Kuznets and Rostow, is also pursued by Greiner, Semmler and Gong (2005). Overall, Kuznets was ambiguous whether there are regular mechanisms generating cycles. He conjectured that cycles may be in the economic data solely as a result of certain historical ‘occurrences’.

3.3. The Schumpeter innovation cycles

Schumpeter's concept of competition deviates from the neoclassical conception in some essential aspects. First, competition is not limited to price or quantity adjustments. It is described as an evolutionary process, as a process of ‘creative destruction’. The engines of this development are capitalist enterprises. ‘Capitalism, then, is by nature a form or method of economic change and not only never is but never can be stationary ... The fundamental impulse that sets and keeps the capitalist engine in motion comes from the new consumer's goods, the new methods of production or transportation, the new markets, the new forms of industrial organization that capitalist enterprise creates’ (Schumpeter 1970: 83). The incentives for developing these types of technical change originate in transient surplus profits. What is taken as given in neoclassical general equilibrium analysis as parametric data, when the price and quantity adjustments occur is the explicandum in Schumpeter: process innovation, product innovation, new forms of organization of the firm and new forms of financial control.

Second, Schumpeter stresses that competition is not necessarily an equilibrating force. When referring to the existence of entrepreneurial firms and their rivalry, Schumpeter maintains that ‘there is in fact no determinate equilibrium at all and the possibility presents itself that there may be an endless sequence of moves and counter-moves, an indefinite state of warfare between firms’ (Ibid.: 79). Moreover, competition as an evolutionary process takes place through time, in discrete steps. For example, he writes, ‘Now the first thing we discover in working out the propositions that thus relate quantities belonging to different points in time is the fact that, once equilibrium has been destroyed by some disturbances, the process of establishing a new one is not so sure and prompt and economical as the old theory of perfect competition made it out to be, and the possibility that the very struggle for adjustment might lead such system farther away instead of nearer to a new equilibrium. This will happen in most cases unless the disturbance is small’ (Ibid.: 103). Indeed, in Schumpeter it is the product and process innovation, undertaken by the entrepreneur, which brings the economic system out of equilibrium, resulting in long waves and business cycles. Moreover, he even does not seem to be very interested in a theory of centers of gravitation for market forces as developed by the classical economists.

Third, in Schumpeter, competition is an evolutionary process, one of rivalry between firms motivated by the search for surplus profit. He calls this surplus profit the transient ‘monopoly profit’ of new processes and new products, ‘Thus, it is true that there is or may be an element of genuine monopoly gain in those entrepreneurial profits which are the prizes offered by capitalist society to the successful innovator. But the quantitative importance of that element, its volatile nature and its function in the process in which it emerges put it in a class by itself’ (Ibid.: 102). ‘The transient surplus profit does not appear as deviation from the perfectly competitive state of the economy and as a waste in the allocation of resources, but as a reward for the innovator and a gain for the capitalist society. On the contrary, the perfectly competitive economy, where every market agent behaves in the same way under the condition of parametrically given external conditions seems to imply a waste of resources ... working in the conditions of capitalist evolution, the perfect competitive arrangement displays wastes of its own. The firm of the type that is compatible with perfect competition is in many cases inferior in internal, especially technological, efficiency. If it is, then it wastes opportunities’ (Schumpeter 1970: 106). Thus, in Schumpeter's view, the entrepreneurial firms are powerful engines of progress and ‘in particular of the long-run expansion of total output’ (Ibid.).

Following Schumpeter's footsteps, the literature after Schumpeter has distinguished between radical and incremental innovation. The major waves of radical innovations, which were followed by the diffusion of this new technology and incremental innovations are.[3]

· The water-powered mechanization of the industry of the 18th and early 19th century;

· The steam-powered mechanization of the industry and transport of the middle of the 19th century (rail ways, steam engines, machine tools);

· The electrification of industry, transport and homes at the end of the 19th century;

· Motorization of industrial production, transport, civil economy and the war machinery (from ~1914 onward);

· Computerization and information technology from the 1960s and 1970s onward.

According to Schumpeter's oriented long wave theories, each of those radical innovations did not only create long waves in economic development, but each of those long waves were driven by different technology, originated in different countries and then diffused world wide.

3.4. The Samuelson accelerator-multiplier cycles

A model of medium-time scale is the one created by Samuelson (1939). The basic construction is as follows: consumer spending (via increased sales by firms) accelerates investment; output changes results in income changes through the multiplier, which, in turn, again stimulates sales, that is consumer spending.

The multiplier-accelerator model of Samuelson (Ibid.) can produce cycles. Take Сt = consumption, It = investment, Yt = income, C0 = autonomous consumption, I0 = autonomous investment, and G = C0 + I0; I = S = sY, therefore the multiplier is: ![]() Use:

Use:

Ct = C0 + αYt – 1, (1)

It = I0 + β (Yt – 1 – Yt – 1), (2)

Yt = Сt + It . (3)

Substituting (1) and (2) into (3) gives

Yt = С0 + αYt – 1 + I0 + βYt – 1 – βYt – 2,

G = C0 + I0,

Yt = G + (α + β) Yt – 1 – βYt – 2.

The standard form of a second order linear difference equation is:

Yt – (α – β) Yt – 1 + βYt – 2 = G, (4)

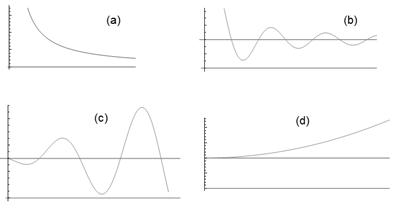

which is stable or unstable depending on the size of ?. Moreover, one can have contracting or expanding cycles depending on whether there exist imaginary parts of the eigenvalues (see Figs 2a – 2d).

When we replace income by profit flows Rt, one can turn the above into a kind of Kalecki model such as: It + 1 = A + αRt + b(Rt – Rt – 1). If one writes for spRt = It, ![]() , we get a similar second order difference equation:

, we get a similar second order difference equation:

![]() , (5)

, (5)

which again can be stable or unstable and it can produce unidirectional change or oscillations. The Kalecki model is further studied in Sub-section 3.7.

Figs 2a – 2d. Stable and unstable development and oscillations

3.5. The Goodwin growth and income distribution cycles

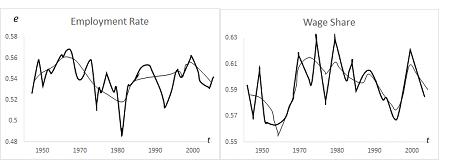

Other types of cycles that have been discussed, particularly in the Post War II period, where Goodwin's growth cycle theory that postulates an interaction of employment and wage share. It looked like a business cycle model when it was first proposed but, in fact, empirically it seems to operate also on a medium time scale.[4]

Goodwin (1967) postulates cycles driven by growth and income distribution. Low growth, generated by low profits and investment, generates unemployment, which in turn limits wage growth as compared to productivity. This gives rise to lowering the wage share: low wage share means high profit share and slowly rising investment, which reaches a turning point as employment and wage growth make the wage share rising and the profit share falling. By utilizing nonlinear differential equations, originally developed by Lotka and Volterra for the models of interacting populations, we can rewrite the Goodwin model of wage-employment dynamics as follows:

![]() ,

,

or as

,

,

where ![]() represents the time rate of change of the ratio of the employed to the total labor force and

represents the time rate of change of the ratio of the employed to the total labor force and ![]() is the change of the wage share. Both variables depend on the level of х and the constants a, b, c, d > 0. The coefficient, a, denotes the trend of employment if all income is reinvested (y = 0) and d is the fall in real wage if (x = 0). The symbol by denotes the influence of the wage share on the employment ratio, and cx the positive influence of employment on the wage share. Due to this interaction of the variables the employment ratio is prevented from rising and the wage share from falling without limits.

is the change of the wage share. Both variables depend on the level of х and the constants a, b, c, d > 0. The coefficient, a, denotes the trend of employment if all income is reinvested (y = 0) and d is the fall in real wage if (x = 0). The symbol by denotes the influence of the wage share on the employment ratio, and cx the positive influence of employment on the wage share. Due to this interaction of the variables the employment ratio is prevented from rising and the wage share from falling without limits.

For a growth model with trends as represented by Goodwin, the coefficients can be interpreted as follows: a = b – (m + n) where b is the output/capital ratio (Y/K), m is the growth rate of productivity and n is the growth rate of the labor force. All of those are taken as constants. Assuming a linearized wage function (for instance, ![]() and with m the growth rate of productivity as before, we obtain for the growth rate of the wage share the term

and with m the growth rate of productivity as before, we obtain for the growth rate of the wage share the term ![]() with m = d – e. Thus, the second pair of differential equations can be written as:

with m = d – e. Thus, the second pair of differential equations can be written as:

![]()

![]()

which is indeed equivalent to the first equation of the (above) system, except that it is written in terms of growth rates. The core of the last system shows that the change of the employment ratio depends on the profit share (1 – y) and that the change of the wage share depends on the employment ratio. This form has been used to explain the fluctuation of the employment ratio and the fluctuation of the industrial reserve army in Marx (Marx 2003 [1867]: ch. 23; see Goodwin 1967). The basic structure of this model represents the interacting variables of the employment ratio and wage share as dynamically connected.

The last system has two equilibria: (0, 0) and ![]() . The linear approximation of the system is with ξ1, ξ2 as small deviations from the equilibrium values

. The linear approximation of the system is with ξ1, ξ2 as small deviations from the equilibrium values

![]() .

.

The calculation of the Jacobian for the first linear approximation gives for the equilibrium ![]()

The real parts of the eigenvalues are zero and the linear approximation of the equilibrium point represents the dynamical structure of a center (Hirsch and Smale 1974: 258). With real parts of the eigenvalues zero, the linear approximation of the system through the Jacobian does not allow conclusions regarding the behavior of the dynamical system in the neighborhood of the equilibrium. Yet, as can be shown, by constructing a Liapunov function for the above system, which is constant in motion and hence has time derivatives ![]() the wage share-employment dynamics results in closed solution curves (Ibid.; Flaschel and Semmler 1987).

the wage share-employment dynamics results in closed solution curves (Ibid.; Flaschel and Semmler 1987).

The closed trajectories of the system are, however, only closed curves and the wage share-employment dynamics does not allow for persistent cycles, such as limit cycles (Hirsch and Smale 1974: 262; Flaschel 1984). In addition (see Flaschel and Semmler 1987), the dynamical system is structurally unstable, since small perturbations can lead to additional interaction of the variables (J11 or J22 can become nonzero). This leads to a qualitatively different dynamical behavior of the system, hence it can become totally stable or unstable. Under certain conditions the above system can also become globally asymptotically stable. This can occur if the conditions for Olech's theorem are fulfilled (see Flaschel 1984).

Equivalent results are obtained when in place of a linear wage function a nonlinear wage function is substituted in the system (see Velupillai 1979). The wage share-employment dynamics worked out originally by Goodwin for a model of cyclical growth and then applied by him to explain an endogenously created unemployment of labor depict a growing economy, whereas often models of nonlinear oscillations refer only to a stationary economy.

Since the change of the wage share and the change of labor market institutions such as bargaining and other protective legislature are slow, this model of economic cycles, however, does not really model business cycles but rather medium run cycles. On the other hand, for a theory of longer cycles the dynamical interaction of other important variables over time (such as waves of innovations, changes of capital/output ratio, productivity, relative prices and interest rates) as well as demand factors are neglected.

3.6. The Keynes–Kaldor demand driven cycles

The demand factors are considered in the next section presented here. The Keynes–Kaldor model seems to operate on a shorter time scale. It essentially refers to the role of demand, defined by the relation of investment and savings. In his article, Kaldor (1940) proposed such a shorter scale cycle model, a nonlinear model of business cycles, which after that has been reformulated in the light of mathematical advances in the theory of nonlinear oscillations, which take into account demand changes (Kaldor 1940, 1971; Chang and Smyth 1971; Semmler 1986).

Kaldor relies on a geometric presentation of a business cycle model which depends on a nonlinear relation between income changes and capital stock changes and which seems to generate self-sustained cycles without rigid specifications for the coefficients, time lags and initial shocks. The geometric presentation of his model of persistent business cycles due to the dynamic interaction between income changes and accumulation and dissolution of capital indeed also includes the possibility of limit cycles, that is asymptotically stable cycles regardless of the initial shocks and time lags.

His ideas are also formulated for a stationary economic system and can be represented by nonlinear differential equations in the following way (Chang and Smyth 1971):

![]()

where α is a reaction coefficient, ![]() the rate of change of income,

the rate of change of income, ![]() the rate of change of the capital stock, I = investment and S = saving as functions of the level of income and capital stock. According to the assumptions underlying the model, there is a unique singular point (Ibid.: 40). This type of Keynesian–Kaldorian model can give rise to persistent cycles (see Semmler 1986), it does not model the specific role of growth and income distribution, as Goodwin has stressed. Yet it stresses the role of endogenously changing demand. The linear approximation is:

the rate of change of the capital stock, I = investment and S = saving as functions of the level of income and capital stock. According to the assumptions underlying the model, there is a unique singular point (Ibid.: 40). This type of Keynesian–Kaldorian model can give rise to persistent cycles (see Semmler 1986), it does not model the specific role of growth and income distribution, as Goodwin has stressed. Yet it stresses the role of endogenously changing demand. The linear approximation is:

![]() ,

,

where the Jacobian is

,

,

where ![]() since

since ![]() and

and ![]() (Chang and Smyth 1971: 41). The determinant is

(Chang and Smyth 1971: 41). The determinant is ![]() which is positive because for the existence of a unique singular point it is assumed that

which is positive because for the existence of a unique singular point it is assumed that ![]() . The element,

. The element,![]() , is always negative. The linear approximation with the Jacobian represents at its core the investment-income dynamics according to which the change of income depends negatively on the level of the capital stock

, is always negative. The linear approximation with the Jacobian represents at its core the investment-income dynamics according to which the change of income depends negatively on the level of the capital stock ![]() and the change of capital stock depends positively on the level of income

and the change of capital stock depends positively on the level of income ![]() but there is a negative feedback effect from the level of capital stock to the change of capital stock and an ambiguous feedback effect from the level of income to the change of income

but there is a negative feedback effect from the level of capital stock to the change of capital stock and an ambiguous feedback effect from the level of income to the change of income ![]() . This will be explained subsequently.

. This will be explained subsequently.

Analyzing the singular point one can conclude that the equilibrium is a focus or a node and that the equilibrium is stable or unstable accordingly as ![]() This singular point also allows for a limit cycle, since the necessary condition for a limit cycle is that the dynamic system has an index of a closed orbit, equal to 1 (Minorsky 1962: 79). This excludes a saddle point as a singular point (see Ibid.: 77). Moreover, the most interesting point in this dynamic system is the ambiguous element

This singular point also allows for a limit cycle, since the necessary condition for a limit cycle is that the dynamic system has an index of a closed orbit, equal to 1 (Minorsky 1962: 79). This excludes a saddle point as a singular point (see Ibid.: 77). Moreover, the most interesting point in this dynamic system is the ambiguous element ![]() . According to Kaldor's graphical presentation, it is assumed (see Kaldor 1940: 184) that

. According to Kaldor's graphical presentation, it is assumed (see Kaldor 1940: 184) that

(1) ![]() for a normal level of income;

for a normal level of income;

(2) ![]() for abnormally high or abnormal lowly levels of income; and

for abnormally high or abnormal lowly levels of income; and

(3) the stationary state equilibrium has a normal level of income.

Fig. 3. Kaldor graph on nonlinear investment and saving functions

This might be illustrated by Fig. 3 with Y being the level of output, which shows that the normal level of Y is unstable and the extreme values of Y are stable. Mathematically this means that the trace ![]() changes signs during cycles. This is the negative criterion of Bendixson (Minorsky 1962: 82) for limit cycles, that is if the trace

changes signs during cycles. This is the negative criterion of Bendixson (Minorsky 1962: 82) for limit cycles, that is if the trace ![]() does not change signs, persistent cycles – limit cycles – cannot exist (see also Guckenheimer and Holms 1983: 44). As proven by Chang and Smyth (1971: section V), there indeed exists the possibility of stable cycles, limit cycles, under the assumption proposed by Kaldor.

does not change signs, persistent cycles – limit cycles – cannot exist (see also Guckenheimer and Holms 1983: 44). As proven by Chang and Smyth (1971: section V), there indeed exists the possibility of stable cycles, limit cycles, under the assumption proposed by Kaldor.

However, the three conditions as formulated above and originally formulated by Kaldor (1940: 1984) are not necessary for the existence of cycles. What is actually necessary for cycles is only that ![]() (i.e. that

(i.e. that ![]() switches signs) at some level of Y. Moreover, the singular point at the normal level of Y does not have to be unstable as a necessary condition for a limit cycle. The critical point can be stable (see Minorsky 1962: 75). In addition there also is the possibility that the system is globally asymptotically stable. This is the case if:

switches signs) at some level of Y. Moreover, the singular point at the normal level of Y does not have to be unstable as a necessary condition for a limit cycle. The critical point can be stable (see Minorsky 1962: 75). In addition there also is the possibility that the system is globally asymptotically stable. This is the case if: ![]() and (2)

and (2) ![]() everywhere.

everywhere.

The global asymptotic stability under these conditions follows from Olech's theorem (see Ito 1978: 312).

Evaluating Keynes–Kaldor's model of a demand driven business cycles one can say that Kaldor's formulation of an income-investment dynamics brought some advances regarding a theory of endogenously produced business cycles, especially formulations of the theory of cycles in terms of a theory of nonlinear oscillations (see also Kaldor 1971) one can extend this to include a formulation concerning the dynamics in employment and wage share which was originally more visible in classical models that referred to the profit-investment dynamics.

3.7. The Kalecki profit and investment cycles

To draw some similarities to the Kondratieff long wave theory, we can follow Kalecki (1971) and replace the income, Y, by profit flows П[5] and allow for ![]() to change its sign during the cycle. In some sense the role of profit, wages and income distribution – as in the Goodwin model – can be allowed to come in here.

to change its sign during the cycle. In some sense the role of profit, wages and income distribution – as in the Goodwin model – can be allowed to come in here.

In general it could be assumed that:

(Case 1) ![]() for profit income in an interval such as П1 < П < П2 (see Fig. 4). This may be due to a previous decrease in capital stock, production and employment which entail low construction cost for plants, low material and resource cost and low wage costs (relative to productivity), high profits and low interest rates and easy access to credit. These factors then may give rise to an expectation of rising profits on investments.

for profit income in an interval such as П1 < П < П2 (see Fig. 4). This may be due to a previous decrease in capital stock, production and employment which entail low construction cost for plants, low material and resource cost and low wage costs (relative to productivity), high profits and low interest rates and easy access to credit. These factors then may give rise to an expectation of rising profits on investments.

On the other hand, in other regions we can have:

(Case 2) ![]() with two clarifying conditions:

with two clarifying conditions:

(a) for П > П2 due to capacity limits, rising construction cost for plants and rising material and wage cost (relative to productivity), exhaustion of exhaustible resources, rising interest rates and but falling actual and expected profits. Profits and expected profits may fall due to the rise of those costs and wages – that cannot be passed on – in the long upswing. This looks similar to a mechanism that Kondratieff has indicated to eventually occur in his long upswing (see Sections 2.1 and 3.1).

(b) for П < П1 in a recessionary or slow recovery period, where firms invest in financial funds instead of in real capital (Minsky 1983) but due to the economic conditions in a recessionary period, the rate of change of saving in response to falling profits tend to drop faster than the rate of change of investment. Wage share may have been rising previously, and profit share falling but here investment is still not dropping completely to zero. This resembles the Kondratieff scenario of a long downswing and recessionary or stagnation period.

Though the economic intuition appears the same in our above stylized business cycle dynamics and the Kondratieff long waves phases, the time scales are probably different ones: one is a shorter one and the other a longer one, but the mechanisms may be the same. Yet, for a longer time scale much of the economic structure and relationships are likely to change.

In the history of economic thought the change of sign for ![]() during the economic cycle was verbally anticipated by many writers on the study of capitalist dynamics (Kalecki 1971: 123; Kaldor 1940: 184) and can be regarded as essential for a theory of fluctuations in economic development. Mathematically

during the economic cycle was verbally anticipated by many writers on the study of capitalist dynamics (Kalecki 1971: 123; Kaldor 1940: 184) and can be regarded as essential for a theory of fluctuations in economic development. Mathematically ![]() must change signs in order to generate self-sustained cycles. If

must change signs in order to generate self-sustained cycles. If ![]() and

and ![]() were zero,

were zero, ![]() and

and ![]() alone would determine the profit-investment dynamics. There would only be structurally unstable harmonic oscillations. The negative signs of

alone would determine the profit-investment dynamics. There would only be structurally unstable harmonic oscillations. The negative signs of ![]() and

and ![]() exert a retarding influence on accumulation, and

exert a retarding influence on accumulation, and ![]() represents an accelerating force on capital accumulation, whereas

represents an accelerating force on capital accumulation, whereas ![]() exerts a retarding influence in the boom period and an accelerating impact on profit and accumulation in the later phase of the recession.

exerts a retarding influence in the boom period and an accelerating impact on profit and accumulation in the later phase of the recession.

Intuitively, the existence of self-sustained cycles can be seen in Fig. 4 from the fact that the trajectories of П(t) and К(t) are bounded in absolute values and the profit-investment dynamics follow certain directions in the plane. Roughly speaking, for large enough П(t), ![]() turns negative and for large enough К(t),

turns negative and for large enough К(t), ![]() turns negative and vice versa. Geometrically, this is illustrated by Fig. 4.

turns negative and vice versa. Geometrically, this is illustrated by Fig. 4.

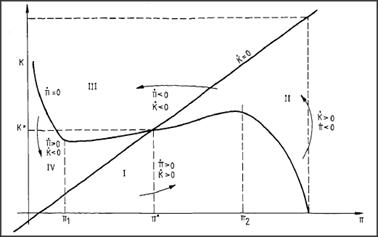

Fig. 4. Phase diagram

For ![]() we get the slope

we get the slope

![]() ,

,

and for ![]() the slope is

the slope is

![]() .

.

![]() Thus, in the plane of the Fig. 4 there are four quadrants. For reasons of simplicity we have assumed a linear investment function in Fig. 4. The system has a unique solution at П* and K* since the curve

Thus, in the plane of the Fig. 4 there are four quadrants. For reasons of simplicity we have assumed a linear investment function in Fig. 4. The system has a unique solution at П* and K* since the curve ![]() has a steeper slope than

has a steeper slope than ![]() when the latter is upward sloping in a certain region. This follows from the assumption in the model.[6] The determinant of the Jacobian of the dynamical system above is

when the latter is upward sloping in a certain region. This follows from the assumption in the model.[6] The determinant of the Jacobian of the dynamical system above is ![]() The singular point is a focus or a node and is stable or unstable accordingly as

The singular point is a focus or a node and is stable or unstable accordingly as ![]() < 0. A saddle is excluded, and the singular point has index 1 as necessary condition for a self-sustained cycle (Minorsky 1962: 176). (The singular point does not have to be unstable as Kaldor originally assumed; see Kaldor 1940: 182.) The existence of a self-sustained cycle follows intuitively from the analysis of the vector fields in the different regions, which correspond roughly to stages of economic cycles.[7]

< 0. A saddle is excluded, and the singular point has index 1 as necessary condition for a self-sustained cycle (Minorsky 1962: 176). (The singular point does not have to be unstable as Kaldor originally assumed; see Kaldor 1940: 182.) The existence of a self-sustained cycle follows intuitively from the analysis of the vector fields in the different regions, which correspond roughly to stages of economic cycles.[7]

For region I, which expresses the dynamics of a recovery period, К(t) is below the ![]() curve and П(t) is below the

curve and П(t) is below the ![]() curve; the decline in capital stock and its effect on profit (i.e. the effects of Cases 1 and 2) as well as other changes in economic conditions in a recessionary period will generate a positive rate of change of profit (since

curve; the decline in capital stock and its effect on profit (i.e. the effects of Cases 1 and 2) as well as other changes in economic conditions in a recessionary period will generate a positive rate of change of profit (since ![]() in region I, see also Case 1). Therefore, in region I we will find

in region I, see also Case 1). Therefore, in region I we will find ![]() and

and ![]()

The increase of profits and investments after a recessionary period will lead to rising К(t), but through the effect of Cases 1 and 2 (i.e. the negative effect of growth of capital stock on profits) the growth rate of II will become negative. Thus, in region II, indicating a boom period, we have ![]() and

and ![]() Hence, the arrows in Fig. 4, indicating the direction of the vector field of П and K, will start bending inward (see Case 2a which leads to

Hence, the arrows in Fig. 4, indicating the direction of the vector field of П and K, will start bending inward (see Case 2a which leads to ![]() ). With capital stock rising and

). With capital stock rising and ![]() due to a magnitude of capital stock greater than its stationary value K*, the capital stock must eventually decline (i.e. through the effect of Case 2). We also have

due to a magnitude of capital stock greater than its stationary value K*, the capital stock must eventually decline (i.e. through the effect of Case 2). We also have ![]() due to

due to ![]() at the beginning of a downswing period (capital may be accumulated more as money capital than as real capital).

at the beginning of a downswing period (capital may be accumulated more as money capital than as real capital).

In region III, indicating a downswing period, through the influence of ![]() on K(t), K(t) also starts declining; thus

on K(t), K(t) also starts declining; thus ![]() and

and ![]() Hence, for

Hence, for ![]() and

and ![]() the vector field is pointing inward. A decline of capital stock below K* in region IV, the recessionary period, however, eventually causes profits to rise. The recessionary period may slowly then turn into a recovery period, indicated by region I. This, of course, assumes again that eventually

the vector field is pointing inward. A decline of capital stock below K* in region IV, the recessionary period, however, eventually causes profits to rise. The recessionary period may slowly then turn into a recovery period, indicated by region I. This, of course, assumes again that eventually ![]() . The investment of financial funds turns into investment in real capital, thus investment out of profit tends to become greater than savings out of profit. The recessionary period (with wage increase below productivity, low material and capital cost, low interest rates and easy access to credit as well as a decline in capital stock and thus rising profit expectation[8] must have its impact on

. The investment of financial funds turns into investment in real capital, thus investment out of profit tends to become greater than savings out of profit. The recessionary period (with wage increase below productivity, low material and capital cost, low interest rates and easy access to credit as well as a decline in capital stock and thus rising profit expectation[8] must have its impact on![]() , for otherwise the recessionary period will endure.

, for otherwise the recessionary period will endure.

Therefore, under the economic conditions stated in Cases 1, 2a, and 2b the profit-investment dynamics creates its own cycles by which profit, investment and thus output and employment cannot exceed certain boundaries. The dynamic system is self-correcting and fluctuates within limits: for large enough K(t) is ![]() and for large enough П(t) is

and for large enough П(t) is ![]() . A similar argument holds for small enough K(t) and П(t). Thus, whereas the system with Cases 1 and 2 becomes stable at its outer boundaries (indicated by the negative sign of

. A similar argument holds for small enough K(t) and П(t). Thus, whereas the system with Cases 1 and 2 becomes stable at its outer boundaries (indicated by the negative sign of ![]() ), it cannot converge towards equilibrium, since the equilibrium is unstable (indicated by the positive sign of

), it cannot converge towards equilibrium, since the equilibrium is unstable (indicated by the positive sign of ![]() ). Therefore, the dynamics of the system will result in cycles (see Semmler 1986). These self-sustained cycles, resulting from the profit-investment dynamics, can be regarded as close to classical dynamics and conceptions and the original Kalecki model and reflects to a certain extent also the dynamics of output, income, resource cost, price level, wage and bank deposit and interest rate dynamics of the Kondratieff long wave theory. Though for such a cycle on long time scale many structural changes may occur that could significantly change the mechanisms and economic relationship over the cycle.

). Therefore, the dynamics of the system will result in cycles (see Semmler 1986). These self-sustained cycles, resulting from the profit-investment dynamics, can be regarded as close to classical dynamics and conceptions and the original Kalecki model and reflects to a certain extent also the dynamics of output, income, resource cost, price level, wage and bank deposit and interest rate dynamics of the Kondratieff long wave theory. Though for such a cycle on long time scale many structural changes may occur that could significantly change the mechanisms and economic relationship over the cycle.

4. The Minsky Financially Driven Basic Cycle and Super-Cycle

Next we discuss a Minsky long cycle: a financially-based approach to the long wave theory. Long cycles have historically been interpreted as an interaction of real forces with cost and prices. Kondratieff cycles emphasize secular changes in production and prices; Kuznets cycles are associated with economic development and infrastructure accumulation; Schumpeterian cycles are the result of waves of technological innovation; while Goodwin cycles are based on changes in the functional distribution of income arising from changed bargaining power conditions in a period of high growth rates and Keynesian theories express demand factors.

The work of Hyman Minsky provides an explicitly financially driven theory of business cycles. Minsky's own writings were largely devoted to exposition of a short-run cycle and a very long-run analysis of stages of development of capitalism. The short-run analysis is illustrated in two articles (Minsky 1957, 1959) that present a financially driven model of the business cycle based on the multiplier-accelerator mechanism with floors and ceilings. A later formalization is the Delli Gatti et al.'s work (1994) in which the underlying dynamic mechanism is increasing leveraging of profit flows, which roughly captures Minsky's (1992a) hedge-speculative-Ponzi finance transition dynamic that is at the heart of his famous financial instability hypothesis. The very long-run analysis of stages of capitalism's development is illustrated in Minsky's (1992b) essay on ‘Schumpeter and Finance’. These stages of development perspective have been further elaborated by Whalen (1999) and Wray (2009).

Recently, Palley (2010, 2011) has argued Minsky's (1992a) financial instability hypothesis also involves a theory of long cycles. This long cycle explains why financial capitalism is prone to periodic crises and it provides a financially grounded approach to understanding long wave economics.

A long cycles perspective provides a middle ground between short cycle analysis and stages of development analysis. Such a perspective was substantially developed by Minsky in a paper co-authored with Piero Ferri (Ferri and Minsky 1992). However, unfortunately, Minsky entirely omitted it in his essay (Minsky 1992a) summarizing his financial instability hypothesis, leaving the relation between the short and long cycle undeveloped.

Minsky's financial instability hypothesis maintains that capitalist financial systems have an inbuilt proclivity to financial instability that tends to emerge in periods of economic tranquility. Minsky's framework is one of evolutionary instability and it can be thought of as resting on two different cyclical processes (Palley 2010, 2011). The first is a short cycle and can be labeled the ‘Minsky basic cycle’. The second is a long cycle that can be labeled the ‘Minsky super cycle’.

The Minsky basic cycle has been the dominant focus of interest among those (mostly Post Keynesians) who have sought to incorporate Minsky's ideas into macroeconomics and it provides an explanation of the standard business cycle. The basic cycle is driven by evolving patterns of financing arrangements and it captures the phenomenon of emerging financial fragility in business and household balance sheets. The cycle (see Fig. 5) begins with ‘hedge finance’ when borrowers' expected revenues are sufficient to repay interest and loan principal. It then passes on to ‘speculative finance’ when revenues only cover interest, and the cycle ends with ‘Ponzi finance’ when borrowers' revenues are insufficient to cover interest payments and they rely on capital gains to meet their obligations.

Fig. 5. Minsky financing practices

The Minsky basic cycle embodies a psychologically based theory of the business cycle. Agents become progressively more optimistic in tranquil periods, which manifest itself in increasingly optimistic valuations of assets and associated actual and expected revenue streams, and willingness to take on increasing risk in belief that the good times are here forever. This optimistic psychology affects credit volume via the behavior of both borrowers and lenders – not just one side of the market. That is critical because it means market discipline becomes progressively diminished. Leveraging is increased but the usual text book scenario of corporate finance, whereby higher leverage results in higher risk premia, is not visible in the cost of credit. Instead, credit remains cheap and plentiful because of these psychological developments.

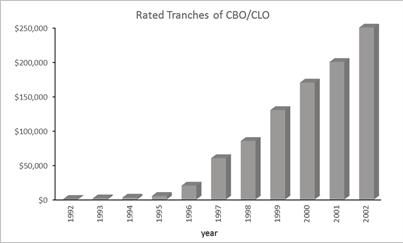

Our empirical analysis in Section 5.4 illustrates this credit dynamic for the recent long financial cycle beginning in the 1990s. Initially, it was a real cycle driven by information technology (IT). This IT bubble burst around 2000/2001. However, expansion resumed, owing to Minsky's financial cycle of over-optimism, high leverage, underestimation of risk, and expansion of new financial practices. The data show a high degree of leveraging during this period, an optimistic view of profit expectations, low risk premia, low credit spreads, and few credit constraints. Thus, contrary to corporate finance textbooks, the market generated high leveraging with low risk premia.

This process of increasing optimism, rising credit expansion and low risk perception is evident in the tendency of business cycle expansions to foster talking about the ‘death of the business cycle’. In the USA, the 1990s experienced much ‘talk’ of a ‘new economy’ which was supposed to have killed the business cycle by inaugurating a period of permanently accelerated productivity growth. That was followed, in the 2000s, by ‘talk’ of the ‘Great Moderation’ which claimed central banks had tamed the business cycle through improved monetary policy based on improved theoretical understanding of the economy. It is precisely this ‘talk’ which provides prima facie evidence of the operation of the basic Minsky cycle.

Moreover, not only does the increasing optimism driving the basic cycle afflict borrowers and lenders, it also afflicts regulators and policymakers. That means market discipline is weakened both internally (weakened lender discipline) and externally (weakened regulator and policymaker discipline). For instance, Federal Reserve Chairman Ben Bernanke (2004) openly declared himself a believer in the Great Moderation hypothesis.

The basic Minsky cycle is present in every business cycle and explains the observed tendency toward increased leverage and increased balance sheet fragility over the course of standard business cycles. However, it is complemented by the Minsky super cycle, that works over a longer time scale of several business cycles. This long-cycle rests on a process that transforms business institutions, decision-making conventions, and the structures of market governance including regulation. Minsky (Ferri and Minsky 1992) labeled these structures ‘thwarting institutions’ because they are critical to holding at bay the intrinsic instability of capitalist economies. The process of erosion and transformation of thwarting institutions takes several basic cycles, creating a long phase cycle relative to the basic cycle.

The basic cycle and long-cycle operate simultaneously so that the process of institutional erosion and transformation continues during each basic cycle. However, the economy only undergoes a full-blown financial crisis that threatens its survivability when the long-cycle has had time to erode the economy's thwarting institutions. This explains why full-scale financial crises are relatively rare. In-between these crises, the economy experiences more limited financial boom-bust cycles. Once the economy is in a full-scale crisis, it enters a period of renewal characterized by thwarting institutions, with new laws and regulations established and governing institutions empowered. That happened during the Great Depression of the 1930s and it is happening again, following the financial crisis of 2008.

Analytically, the Minsky long-cycle can be thought of as allowing more and more financial risk into the system via the twin developments of ‘regulatory relaxation’ and ‘increased risk taking’. These developments increase both the supply of and demand for risk.

The process of regulatory relaxation has three dimensions. One dimension is regulatory capture whereby the institutions intended to regulate and reduce excessive risk-taking are captured and weakened. Over the past twenty-five years, this process has been evident in Wall Street's stepped up lobbying efforts and the establishment of a revolving door between Wall Street and regulatory agencies such as the Securities and Exchange Commission, the Federal Reserve, and the Treasury Department. A second dimension is regulatory relapse. Regulators are members of and participants in society, and like investors they are also subject to memory loss and reinterpretation of history. Consequently, they too forget the lessons of the past and buy into rhetoric regarding the death of the business cycle. The result is willingness to weaken regulation on grounds that things are changed and regulation is no longer needed. These actions are supported by ideological developments that justify such actions. That is where economists have been influential through their theories about the ‘Great Moderation’ and the viability of self-regulation. A third dimension is regulatory escape whereby the supply of risk is increased through financial innovation. Thus, innovation generates new financial products and practices that escape the regulatory net because they did not exist when current regulations were written and are therefore not covered.

The processes of regulatory capture, regulatory relaxation, and regulatory escape are accompanied by increased risk taken by borrowers. First, financial innovation provides new products that allow investors to take more risky financial positions and borrowers to borrow more. Recent examples of this include home equity loans and mortgages that are structured with initial low ‘teaser’ interest rates that later jump to a higher rate. Second, market participants are also subject to gradual memory loss that increases their willingness to take on risk. Thus, the passage of time contributes to forgetting of earlier financial crisis, which fosters new willingness to take on risk. The 1930s generation was cautious about buying stock in light of the experiences of the financial crash of 1929 and the Great Depression, but baby boomers became keen stock investors. The Depression generation's reluctance to buy stock explains the emergence of the equity premium, while the baby boomer's love affair with stocks explains its gradual disappearance.

Changing taste for risk is also evident in cultural developments. One example of this is the development of the ‘greed is good’ culture epitomized by the fictional character Gordon Gecko in the movie Wall Street. Other examples are the emergence of investing as a form of entertainment and changed attitudes toward home ownership. Thus, home ownership became seen as an investment opportunity as much as providing a place to live.

Importantly, these developments concerning attitudes to risk and memory loss also affect all sides of the market so that market discipline becomes an ineffective protection against excessive risk-taking. Borrowers, lenders, and regulators go into the crisis arm-in-arm. Lastly, there can also be an international dimension to the Minsky long cycle. That is because ideas and attitudes easily travel across borders. For instance, the period 1980–2008 was a period that was dominated intellectually by market fundamentalism, which promoted deregulation on a global basis. University economics departments and business schools pedaled a common economic philosophy that was adopted by business participants and regulators worldwide. Organizations like the International Monetary Fund and World Bank also pushed these ideas. As a result, developments associated with the Minsky long cycle operated on a global basis giving rise to common financial trends across countries that multiplied the overall effect.

The twin cycle explanation of Minsky's financial instability hypothesis incorporates institutional change, evolutionary dynamics, and the forces of human self-interest and fallibility. Empirically, it appears to comport well with developments between 1981 and 2008. During this period there were three basic cycles (1981–1990, 1991–2001, and 2002–2008). Each of those cycles was marked by developments that had borrowers and lenders taking on increasingly more financial risk in a manner consistent with Minsky's ‘hedge to speculative to Ponzi’ finance dynamic. The period as a whole was marked by erosion of thwarting institutions via continuous financial innovation, financial deregulation, regulatory capture, and changed investor attitudes to risk, all of which is consistent with the idea of the Minsky long cycle.

The Minsky long cycle enriches long wave theory. In addition to adding financial factors, the Minsky cycle has different implications for the pattern of long waves compared to conventional long wave theory. Conventional theories see a separate long wave on top of which are imposed shorter waves. In contrast, the Minsky long cycle operates over a long time scale to gradually and persistently change the character of the short cycle (i.e. the Minsky basic cycle) until a crisis is generated.

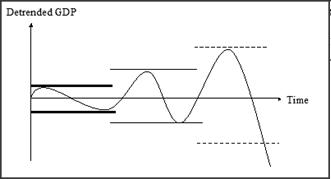

This pattern of evolution is illustrated in Fig. 6, which shows a series of basic cycles characterized by evolving greater amplitude. This evolution is driven by symmetric weakening of the thwarting institutions, represented by the widening and thinning of the bands that determine the system's floors and ceilings. Eventually the thwarting institutions become sufficiently weakened and financial excess becomes sufficiently deep that the economy experiences a cyclical downturn that is uncontainable and becomes a crisis.

Fig. 6. De-trended GDP – symmetric fluctuations

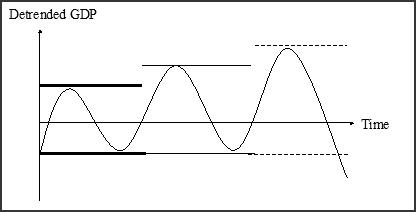

Fig. 6 shows the case where economy undergoes basic cycles of symmetrically widening amplitude prior to the crisis. However, there is no requirement for this. Another possibility is that cycles have asymmetrically changing amplitude. This alternative case is shown in Fig. 7 which represents Minsky's endogenous financial instability hypothesis as having an upward bias. In this case thwarting institution ceilings are less durable than the floors, giving rise to stronger and longer booms before crisis eventually hits. A third possibility is a long-cycle of constant amplitude and symmetric gradual weakening of thwarting institutions that eventually ends with a financial crisis. This richness of dynamic possibilities speaks to both the theoretical generality and historical specificity of Minsky's analytical perspective. The dynamics of the process are general but how the process actually plays out is historically and institutionally specific.

Fig. 7. De-trended GDP – asymmetric fluctuations

Analytically, the full Minsky system can be thought of as a combination of three different approaches to the business cycle. The dynamic behind the Minsky basic cycle is a finance-driven version of Samuelson's (1939) multiplier-accelerator formulation of the business cycle (see Section 3.4). This dynamic is essentially the same as that contained in new Keynesian financial accelerator business cycle models (Bernanke et al. 1996, 1999; Kiyotaki and Moore 1997). Thwarting institution floors and ceilings link Minsky's thinking to Hicks' (1950) construction of the trade cycle. The thwarting institutions are explicitly present in the floors and ceilings, but they can also be present in the coefficients of the multiplier-accelerator model, which determine the responsiveness of economic activity to changes in such variables as expectations and asset prices. Shifting and weakening of floors and ceilings and changing of the behavioral coefficients then capture the long-cycle aspect. This connects Minsky to long wave theory, with the role of financial innovation linking to Schumpeter's (1939) construction of an innovation cycle.

Despite these commonalities with the existing cycle theory, formally modeling Minsky's financial instability hypothesis is difficult and can be potentially misleading. Though models can add to understanding, they can also mislead and subtract.

One problem is that formal modeling imposes too deterministic phase length on what is in reality a historically idiosyncratic process. Adding stochastic disturbances jostles the process but does not adequately capture its idiosyncratic character, which Heraclitus described as ‘No man ever steps in the same river twice’. A second modeling problem is that the timing of real world financial disruptions can appear almost accidental. This makes it seem as if the crisis is accidental when it is, in fact, rooted systematically in prior structural developments, which had generated vulnerabilities.

A third problem is the financial instability hypothesis is a quintessentially non-equilibrium phenomenon in which the economic process is characterized by the gradual inevitable evolution of instability that agents are blind too, even though it is inherent in the structure and patterns of behavior – and agents may even know this intellectually.

This problematic of non-equilibrium is explicitly raised by Minsky (1992b: 104) in his ‘Schumpeter and Finance’ essay, ‘No doctrine, no vision that reduces economics to the study of equilibrium seeking and sustaining systems can have long-lasting relevance. The message of Schumpeter is that history does not lead to an end of history’.

5. Empirical Evaluation of the Cycle Theories of Different Time Scales

Next we discuss some methodology used in the extraction of cycles from data. In the literature there are three typical methods to empirically study cycles. These are, first, spectral analysis (Fourier's theorem), second, filtering methods (HP – filter, BP – filter and penalized splines), and, third, wavelet theory.[9] Since the advantages and disadvantages of the second one have been discussed widely, we will here more extensively focus on the first and the third methods.

5.1. A general approach of extracting cycles from data: Fourier's theorem

Generally speaking, a function is termed periodic if it exhibits the following properties:

f(х) = f(x + T).

In this case, T is known as the ‘period’ and, if x is time, then is the frequency. In the physical world there are many phenomena that exhibit periodic behavior, for example, pendulums, springs, and waves, to name just a few. Mathematical examples also abound.

It is interesting to consider what happens when periodic functions are added together. When several periodic functions are added together, some parts reinforce each other (when both are positive) and other parts cancel each other (when the functions are of opposite sign). But the interactions may be more or less complex and form surprising shapes, for example, a square wave.

From the physical world, we can readily observe certain properties of periodic phenomenon, for example, cancellation, reinforcement, damping, etc. When one moves away from two sound sources emitting tones of different frequencies, one hears, alternately, louder and softer tones.

It was observations of this kind that motivated Joseph Fourier, in the early 1800s to speculate that virtually any function could be formed by adding together the correct combination of periodic functions. In his famous analysis, Fourier defined a sequence of trigonometric values as follows: for any function, f, which is integrable from –π to π

All things come in seasons – Heraclitus

One can never step into the same river twice – Heraclitus

1. Introduction

After a thirty year period of relative tranquility in the world economy – the so-called period of ‘great moderation’ – the U.S. economy suffered a financial meltdown in 2008 that triggered the ‘great recession’. These events have motivated new interest in theories that can explain long periods of expansion that end suddenly with deep recessions. One approach, which has been intellectually unfashionable for many years, is the theory of long economic waves.

This paper examines the empirical and epistemological contributions made by economists regarding the cyclical nature of economic and social development. The paper discusses the main mechanisms of economic cycles involving different time scales, with a particular focus on long wave theory. As part of this survey, the paper shows the continuing relevance of the theoretical constructs developed by Nikolai Kondratieff (also, Kondratiev, Кондратьев) and Simon Kuznets (Кузнец), both for modern macroeconomics and for assessing possible future scenarios. The paper also shows the difficulty of modeling long wave analysis as it poses significant challenges to the equilibrium method which dominates shorter period economic analysis.