Long Wave Rhythms: A Pictorial Guide to 220 Years of U.S. History, with Forecasts

Almanac: Kondratieff Waves: Dimensions and Prospects at the Dawn of the 21st Century

Abstract

The macrohistorical rhythms that have structured US economic, social and political life since the nation achieved independence have been shaped by mode-locked Kondratieff, Kuznets and Juglar cycles. Details of this mode-locking are provided, together with the timing of the resulting upswings and downswings, recessions and depressions, technological revolutions and Menschian metamorphoses, generational dynamics and the phase structure of American political history. Using the resulting long-wave clock predictions are made of the key turning points in the next long wave that began in the 2007–2012 Kondratieff trough.

Keywords: Kondratieff waves, Kuznets cycles, Juglar cycles, metamorphosis model, mode-locked rhythms, social generations, technological revolutions, long-wave clock.

Introduction

The last Kondratieff peak occurred in the USA as inflation spiraled upward in 1980–1981. The on-time arrival in 2007 of the current Great Recession, a classic Kondratieff trough signaled by a stock market crash, confirms predictions made in 1991 (Berry 1991) but also reminds us that we live in a world where Kondratieff waves, Kuznets (growth) cycles and Juglar (business) cycles are mode locked in well-defined rhythms. Mainstream economists ignore these rhythms because they are largely exogenous to the policy instruments at their disposal. The purpose of this pictorial review is to provide an easy-to-understand guide that might be useful to those who wish to know about the patterns and proc- esses that economists neglect by synthesizing the results of a 20-year research program into U.S. macrohistory at the University of Texas at Dallas. We also offer a new set of predictions for the next 56-year trough-to-trough period. The studies that we utilize are listed in the References.

The Long Wave Clock

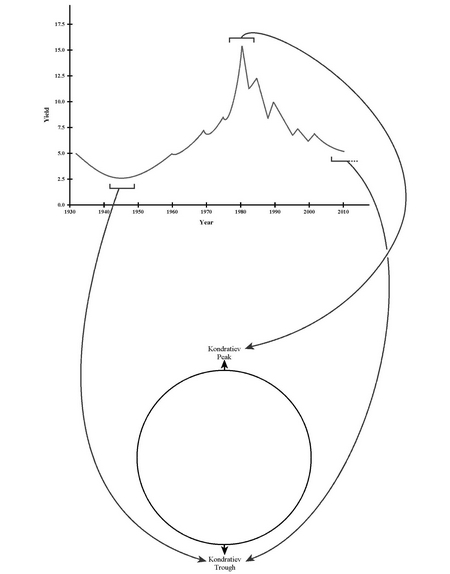

We begin by reintroducing the idea of long wave clock, as originally depicted by Brian J. L. Berry (1991). It is shown in Fig. 1 as a circle that has a Kondratieff peak at the top and a Kondratieff trough at the bottom. The relationship to upswings and downturns of prices and inflation is illustrated by the arrows linking the peak and trough to the rise and fall of the yields on Moody's AAA Corporate Bonds from their trough after World War II to their peak in 1980–1981 and their subsequent collapse into the Great Recession, a period of approximately 56 years.

Fig. 1. Relationship between inflation waves and the long-wave clock

This 56-year trough-to-trough rhythm has characterized movements of prices and inflation in the USA since the nation achieved independence (Berry, Kim, and Baker 2001; Berry and Kim 1996). The dates of the troughs and peaks and the associated reflationary/inflationary upwaves and disinflationary/deflationary downwaves are shown in Fig. 2.

Fig. 2. Timing of Kondratieff peaks, troughs and inflation waves in the last two centuries

Embedded Cycles

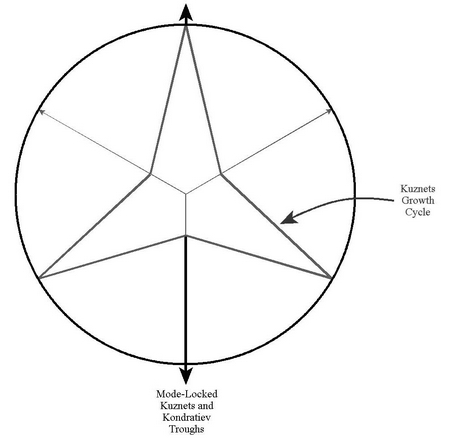

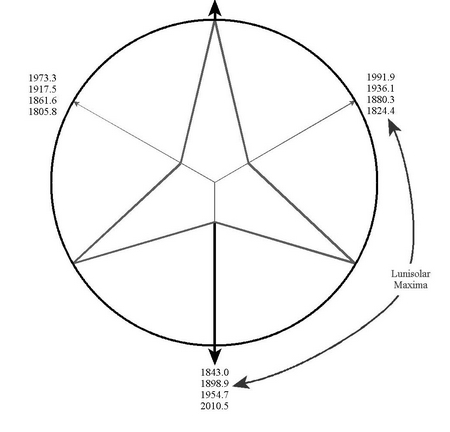

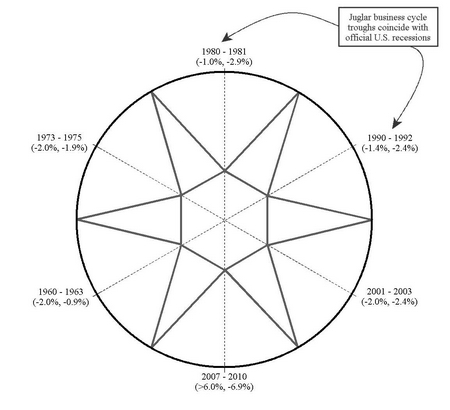

Embedded within each long wave are three 18.6-year Kuznets cycles of economic growth (Berry, Kim, and Baker 2001; Berry, Harpham, and Elliott 1995). They interlock in deflationary depressions, the Kondratieff-Kuznets troughs shown in Fig. 3. Timing may be maintained by an exogenous pacemaker: successive Kuznets troughs reappear in lockstep with 18.6-year lunisolar maxima, as set down in Fig. 4 (Berry 2000). Major stock market collapses have signaled the downturn from each Kuznets peak over the past 200 years. In turn, nestled between each Kuznets peak and trough is a Juglar business cycle of 9.3 years. There are six of the Juglar cycles to a Kondratieff wave, as shown in Fig. 5, two to each Kuznets cycle, one on the upwave and one on the downwave. The figure also shows the change in employment and in spending on discretionary services in the last six official U.S. recessions, each of which coincides with a Juglar trough. In 2007, for example, employment declined by over 6 % and discretionary spending by 6.9 %.

Fig. 3. Three Kuznets economic growth cycles are mode-locked within each Kondratieff wave

Fig. 4. Kuznets cycle troughs coincide with lunisolar maxima. Is this evidence of an exogenous pacemaker (Zeitgeber)?

Fig. 5. Six Juglar business cycles are mode-locked within each Kondratieff wave, two per Kuznets cycle. Recessions occur in Juglar troughs

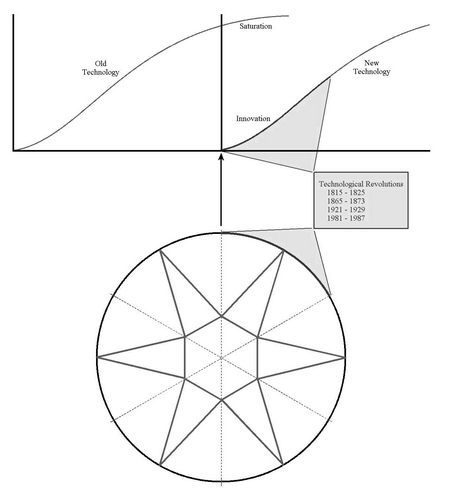

The Driving Force: Technological Revolutions

Long waves are driven by clusters of innovations that introduce new techno-economic systems and give rise to waves of economic growth and social change. These clusters occur in the aftermath of stagflation crises (Kondratieff peaks), as shown in Fig. 6 (Berry, Kim, and Kim 1993; Berry, Kim, and Kim 1994). During these crises the technologies responsible for growth and change in the previous long wave reach market saturation and then collapse. Investors search for alternatives among a menu of new ventures offered by investors and entrepreneurs. Venture capitalists typically invest in a broad basket of alternatives and let the market select the winners. As certain innovations take off they shape the economic system and patterns of growth and change for the half-century that follows. Since independence the USA has experienced four such technological revolutions.

1815–1825: ‘The Era of Good Feelings’ unfolded as growth accelerated, prices decelerated, and the stock market boomed. Southern cotton production led the expansion, accompanied by growth of the New England textile industry and by canal-building. The deflation was compounded by the retirement of government debt incurred in the Louisiana Purchase.

1865–1873: ‘The Gilded Age’. The cash accumulated during the period of war and stagflation made possible loans that financed rapid output growth during the period of reconstruction. Key inventions centered on steel, railroads, coal and steam. Prosperity increased rapidly in an atmosphere of accelerating deflation. There was another wave of immigration, and a prolonged bull market.

Fig. 6. Technological revolutions, introducing economy-transforming innovations, occur after Kondratieff peaks

1921–1929: ‘The Roaring Twenties’ began with rapid growth of the automobile industry, petroleum, chemicals, and electricity and consumer electronics. The new Federal Reserve System, after the panic of the 1920 crisis, pursued an easy-money policy. New techniques of mass production and scientific management increased output, reduced prices, and led to another great wave of prosperity. There was a massive building boom, and a strong bull market unfolded.

1981–1987: ‘The Reagan Era’ was market by the rapid growth of new information technologies: Key innovations included the IBM PC and MS DOS in 1981, the Internet in 1983 and Apple's Macintosh in 1984. As in previous episodes, an era of disinflationary growth began in 1982. A strong bull market pushed stock prices upward, culminating in another historic high, but ending in the crash of 1987.

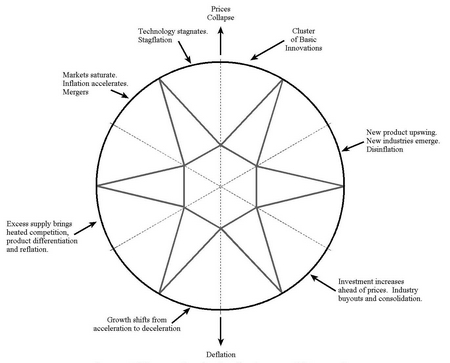

The Metamorphosis Model

Mensch (1979) offers a ‘Metamorphosis Model’ to explain how a technological revolution that emerges from a ‘technology stalemate’ (i.e. a stagflation crises at a Kondratieff peak) sets in motion the sequence of events that leads, 50–60 years later, to the next technology stalemate and technological revolution. As described in Berry (1991) these events are:

1. A cluster of basic innovations (introducing new branches of industry) and radical-improvement innovations (which rejuvenate existing branches) occurs in response to a technology stalemate. Venture capital is attracted to the new lines of business. New demands are awakened.

2. Parallel S-shaped innovation-growth cycles, some of which substitute for older goods or services, characterize the new branches of industry. Initial entry is followed by rapid upswing and by accelerated growth.

3. During the new-product upswing, investment, employment, and incomes increase rapidly, well ahead of prices and inflation. This is the period of disinflation or deflation.

4. Basic and radical-improvement innovations are followed by routine-improvement innovations that rationalize production and increase capital intensity. But these innovations are subject to diminishing returns on the demand side. The growth curve grades over from acceleration to deceleration. This is a natural phase of the product life-cycle of manufactured goods.

5. Corporate growth overestimates domestic markets and produces excess supply and heated competition. Markets become saturated. Almost inevitably, an industrial economy tends to overinvest in any new technology – capital goods in particular.

6. There are two responses to excess supply: attempts to reduce competition by product differentiation and industrial mergers, and attempts to segment domestic and foreign markets, ‘dumping’ excess output. Overinvestment breeds ‘pseudo-innovation’, which benefits neither buyer nor seller. Rather, existing industries attempt to protect their market shares by means of product differentiation in which the ‘image’ or packaging of the product is changed, but no longer are any of its basic qualities altered. The economy then enters a period in which output stagnates. Limits to growth are encountered, markets are flooded, key resources may be scarce and their prices rise, and there is slow-down in income and employment growth. Rates of return decline, and capital is therefore not reinvested in existing lines of business. Instead, money moves into speculation.

7. The end result is a technology stalemate in which growth is replaced by stagnation, and in which large scale organizations seek to maintain the appearance of growth by controlling output and raising prices, thereby inducing stagflation. During this period there is increasing protectionism, yet overconcentration in leading industries sets the price spiral into gear. Large-scale industry and large-scale labor push up wages and prices. Large-scale organizations that grow in the period of pseudo-innovation require and promote conservative patterns of investment: risk-taking in new ventures is minimized.

8. The price spiral ends in a sharp collapse. But because returns in older, established industries were eliminated during the period of stagflation, and the prospect of speculative profit vanishes in the ensuing collapse, new venture capital becomes available, seeking high-growth investment opportunities. The appearance of venture capital at this time results in a rush of attempts to convert many of the inventions that appeared since the preceding period of basic innovation into useful techniques or products – that is, into a cluster of basic innovations that precipitates another long-term growth upswing. New industries attract capital and labor from stagnant sectors, circumvent older resource scarcities, stimulate demand for new kinds of goods and services, and generally introduce the reinvigorating effects of a structural transformation of the economy. Another cycle begins. Fig. 7 offers an overview of these stages, which dominate and pattern successive Juglar cycles.

Fig. 7. Mensch’s metamorphosis model arranged around the long-wave clock. Phases coincide with successive Juglar cycles

Interlocked Social Rhythms

Sociologists William Strauss and Neil Howe argue that there is a recurrent generational cycle in America social history (Strauss and Howe 1991; Berry and Kim 1994). A succession of 18–20-year cohort generations, they say, has dominated American life since settlers first came to North America. A cohort generation consists of everyone born in a particular time-span or ‘cohort period’, sharing a common age bracket as they move through their life cycles, experiencing the same economic and social conditions and sharing a distinct world view. Cohort periods are separated by times of stress when people perceive that historical events are radically altering their social environments. Members of a cohort generation, they argue, share a peer relationship that derives from a combination of a common age location with respect to the background chronology of historic trends and events, perceived membership in a group that shares both belief and behavior, and a sense of social community that is reinforced by the expectations of others. Each generation moves through a common sequence of life phases, each of which occupies a cohort period: youth, young adulthood, mature adulthood and elderhood, and what develops is adherence to certain fundamental notions, a generational weltanschauung or web of beliefs and attitudes about fundamental questions. Transitions between these phases occur during these times of stress, and it is in such times that each existing cohort defines the central role of the phase of life that it is entering, a direction that reverses the perceived excesses of the cohort occupying the same life phase since the last crisis, producing a dialectic which alternates between adjacent generations and leading to a peer-personality relationship among two-apart generations.

Each of these cohort generations is born in one Kuznets cycle, reaches young adulthood in the second, mature adulthood in the third and elderhood in the fourth. There have been eleven such generations since the USA achieved independence. Their birth periods are set down in Fig. 8. The periods of stress that separate these cohort generations coincide with Kuznets troughs. The exceptional stresses of Kondratieff-Kuznets troughs have made some groups try to separate from the mainstream and create utopian communities (Berry 1992).

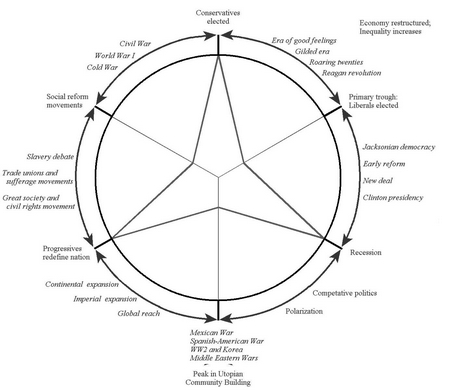

Cycles in American Politics

Similarly interlocked with the Kondratieff-Kuznets rhythms are cycles in American politics, as summarized in Fig. 9 and Table 1 (Berry et al. 1998). Conservatives have been elected to the presidency amidst Kondratieff peaks and have presided over the epochs of technological change driving the next wave. During this period the economy is restructured, there is growing inequality between winners and losers, leading to election of liberals in the next Kuznets trough. During the next Kuznets upswing there is restructuring of the polity, until the next recession brings that change to an end. An era of competitive politics ensues, culminating in political polarization leading into the Kondratieff trough. Emerging from the trough, progressives take over and attempt to redefine the role and purpose of the nation. There is an intensive period of social reform that precedes a drift into conflict as growth slackens, the dominant technology reaches market saturation, and inflation spirals towards the next Kondratieff peak and conservative victory.

Fig. 8. Three cohort generations are born to a long wave and one per Kuznets cycle

Fig. 9. The phase structure of American political history

|

Inflation (long-wavepeak): Con-servatives elected |

Deflationary growth: Economy is restructured by way of new technology |

Primary trough: Liberals elected |

Secondary recovery: Policy is restructured |

Deflation long-wave trough: Political polarization |

Reflationary growth: progressives redefine nation |

Stagflation: Technological and political stalemate |

|

1815–16 |

The Era of Good Feelings • Canal era • Wind and water power • Monroe presidency • Urban/rural inequality grows |

1825–28 |

Jacksonian democracy • Rise of mass political parties and the two party system • Distributive state evolves; spoils system |

1836–1848 • Mexican War |

Continental expansion • Manifest Destiny • Slavery debate |

1857–65 • Civil War • End of slave states |

|

1865–66 |

The Gilded Years • Railroad era • Coal and steam power • Grant presidency • Regional inequality grows |

1873–78 |

Early reform • Third party system • Regulatory initiatives at state and national levels |

1884–1896 • Spanish-American War |

Imperial extension • ‘White Man's Burden’ • Regulatory state evolves • Trade unions and suffrage movements |

1907–18 • World War I • End of imperialism |

|

1919–20 |

The Roaring Twenties • Highway and Airway Era • Oil Power • Harding/Coolidge presidencies • Metropolitan/non-metro-politan inequality grows |

1929–32 |

The New Deal • Fourth party system • Redistributive state • Keynesian macroeconomic policies • Bureaucratic management and control |

1942–1960 • World War II • Korean War |

Global Reach • Free world leadership • Great society programs • Civil rights movement |

1973–69 • Cold War • End of communism |

|

1980–81 |

The Reagan Years • Telecommunications era • Knowledge power • Reagan presidency • Skilled/unskilled inequality grows |

1978–91 |

Clinton presidency • Resurgence of congressional power • Reform of welfare state • Debate on equal opportunity and affirmative action |

2001–2012 • Iraq and Afghan Wars |

|

|

The Next Set of Cycles?

What, then, does the future hold? We now are in a Kondratieff-Kuznets trough, the ‘Great Recession’ – that is the deflationary depression that began with a stock market crash in 2007. If the rhythms of the past repeat themselves with the same 9.3, 18.6 and 55.8 year timing, peaks and troughs will repeat on the calendar suggested by Fig. 10 (Berry 2006).

Fig. 10. Key dates in the next trough-to-trough long wave

Reflation, then inflation will take over on the passage to the next inflationary spiral, around 2036, a path already guaranteed by massive unfunded pension liabilities and other components of indebtedness that can only be honored via the printing press. In keeping with earlier reflationary phases, there already are considerable progressive political pressures to redefine the global role of the United States and to introduce new social reforms. And even though the U.S. role in Iraq and Afghanistan is now coming to an end there is the ever-present risk of more general global conflict further down the road with radical Islam and/or with an expansionist China. Meanwhile, the technologies of the information technology revolution are being pushed towards market saturation, laying the groundwork for the next technological revolution after the peak of 2036. Since the nature of such revolutions is determined by the market we can only speculate about the nature of the one to come, but it will certainly have elements that redefine energy resources, reshape transportation and communications, refashion production, and radically change lifestyles, as have all previous revolutions.

References

Berry B. J. L. 1991. Long Wave Rhythms in Economic Development and Political Behavior. Baltimore, MD: John Hopkins University Press.

Berry B. J. L. 1992. America's Utopian Experiments. Communal Havens from Long-Wave Crises. Hanover, NH: University Press of New England.

Berry B. J. L., Kim H., and Kim H.-M. 1993. Are Long Waves Driven by Techno-Economic Transformations? Evidence for the U.S. and the U.K. Technological Forecasting and Social Change 44: 111–135.

Berry B. J. L., and Kim H. 1994. Leadership Generations, a Long-Wave Macro History. Technological Forecasting and Social Change 46: 1–10.

Berry B. J. L., Kim H., and Kim H-M. 1994. Innovation Diffusion and Long Waves. Technological Forecasting and Social Change 46: 289–293.

Berry B. J. L., Harpham E. J., and Elliott E. 1995. Long Swings in American Inequality: The Kuznets Conjecture Revisited. Papers in Regional Science 74: 153–174.

Berry B. J. L., and Kim H. 1996. Long Waves 1790–1990. Intermittency, Chaos and Control. Chaos Theory in the Social Sciences / Ed. by L. D. Kiel, and E. Elliott pp. 215–236. Ann Arbor, MI: University of Michigan Press.

Berry B. J. L., Elliott E. W., Harpham E. J., and Kim H. 1998. The Rhythms of American Politics. Lanham, MD: University Press of America.

Berry B. J. L. 2000. A Pacemaker for the Long Wave. Technological Forecasting and Social Change 63: 1–23.

Berry B. J. L., Kim H., and Baker E. S. 2001. Low-Frequency Waves of Inflation and Economic Growth: Digital Spectral Analysis. Technological Forecasting and Change 68: 63–73.

Berry B. J. L. 2006. Recurrent Instabilities in K-Wave Macrohistory. Kondratieff Waves, Warfare and World Security / Ed. by T. C. Devezas, pp. 22–29. Amsterdam: IOS Press.

Mensch G. 1979. Stalemate in Technology. Cambridge, MA: Ballinger Publishing Company.

Strauss W., and Howe N. 1991. Generations. A History of America's Future, 1584 to 2069. New York: William Morrow and Co.